Hotel occupancy growth is set to rebound to 0% to 2% in August following a 0.2% decline in July, according to preliminary data from Smith Travel Research that was released September 7. July's decline was fueled by a 1.9% decline in demand, which was the lowest level since July 2017. The occupancy decline in July was the first monthly decline in the past 12 months. Visitation was down from several international markets including China, which we believe is due at least in part to the trade war brewing between the US and China. According to flight data analyzer ForwardKeys, air bookings from China to the United States are down 8.4% since the end of March, when the US began imposing tariffs on China. China is one of the top five markets for visiting the US.

Exhibit 1 August occupancy set to turn positive

Source: Smith Travel Research

Source: Smith Travel Research

Macroeconomic factors will keep 2018 RevPAR at the high end of our forecast

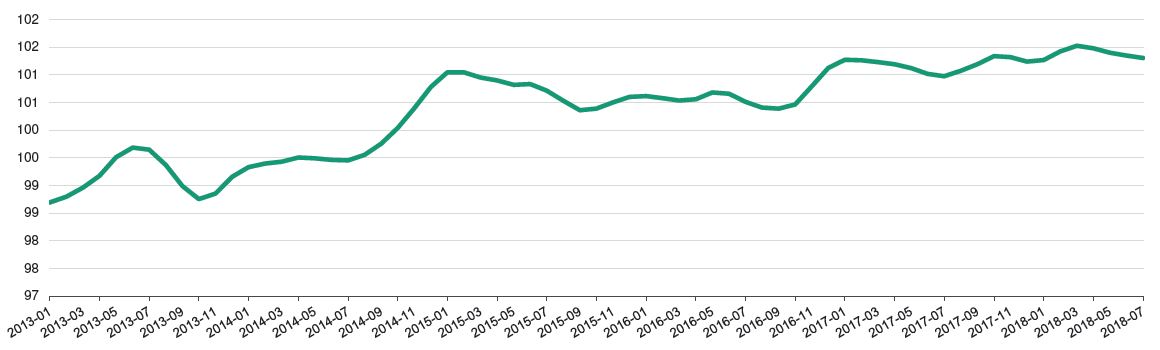

Consumer confidence, while down from its March 2018 peak, is still higher than at any point apart from the March-April 2018 period.

This has resulted in RevPAR growth of 3.5% for the year-to-date period ended July versus 2.7% for the same period in 2017.

Exhibit 2 Strong consumer confidence will continue to drive demand Monthly Consumer Confidence Index (US)

Source: The Organization for Economic Co-operation and Development (OECD)

Source: The Organization for Economic Co-operation and Development (OECD)

Strong demand, stable supply growth, and increased pricing through the end of July will drive full-year 2018 results at the high end of our forecast. We expect that demand in growth will outpace our forecast of 2.0% and grow between 2.5% and 3.0%. With supply growth around 2%, ADR will end the year growing at the high end of our 1% to 3% forecast. This will result in RevPAR of about 3% to 3.5%, above our 1% to 3% forecast.

Steady supply growth will likely not affect demand outside certain markets We expect total US hotel room supply to grow 2% in 2018, which is below historical levels but nonetheless a steady increase from about 1% in 2014.

Exhibit 3 Demand set to outpace supply growth the remainder of the year

Source: Smith Travel Resources, public information

Source: Smith Travel Resources, public information

This growth will mostly be focused in the upscale and upper midscale limited service segment and urban settings. Since early 2013, growth in the upscale segment (including such brands as Hyatt Hotels Corp.’s (Baa2 stable) Hyatt House, Hilton Worldwide Finance, LLC’s (Ba1 stable) Homewood Suites, and Marriott International Inc.’s (Baa2 stable) Residence Inn, has consistently outpaced growth of other segments including luxury and upper upscale, while upper midscale has outpaced those segments over the past year. Per data from Smith Travel Research, year to date though July 31, the upscale and upper midscale grew 5.7% and 4.1%, respectively, as compared to 2.1% for total US hotel rooms.

Exhibit 4 Upscale and upper midscale supply growth outpacing other segments

Source: Smith Travel Research

Source: Smith Travel Research