By Erich Baum, Brian F. Bisema, Raymond Parejo

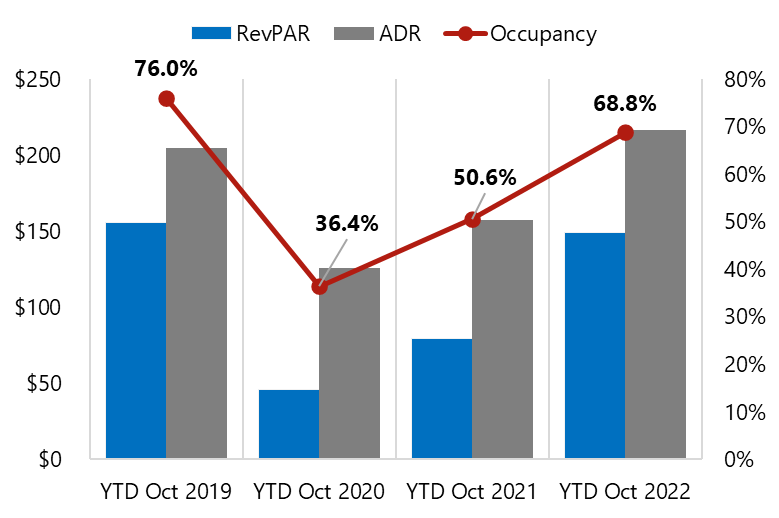

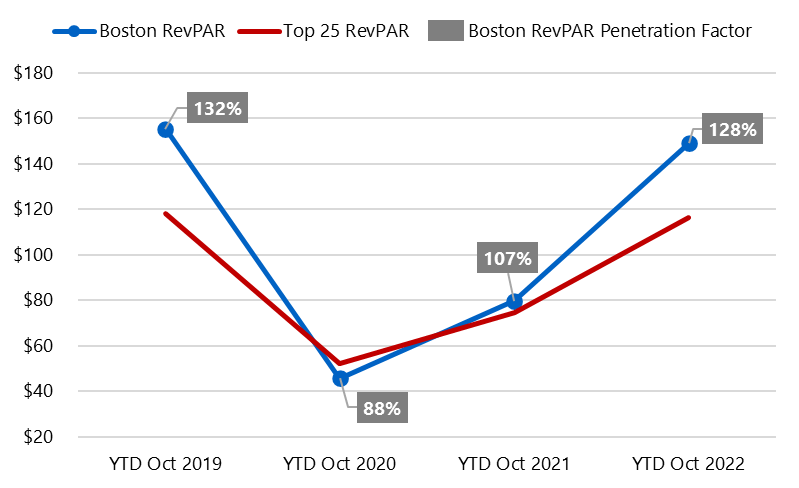

According to STR, Boston’s revenue per available room (RevPAR) finished 2021 at roughly half the pre-pandemic 2019 level, a discouraging performance. But the city took a leap forward in 2022 and is on pace to finish the year with a RevPAR level just a shade below the pre-pandemic performance. After adjusting for inflation, these results are less significant, of course, but the turnaround still represents a huge achievement, particularly considering that the recovery is still in progress for the international travel, corporate transient, and convention demand channels. As illustrated in the charts below, the market’s RevPAR returned to its historical position among the top 25 markets, with the year-to-date October 2022 RevPAR equating to 128% of the top 25 markets’ average. Among the top 25 markets in the country, Boston reported the fifth-highest RevPAR level through year-to-date October 2022, behind only New York City, Oahu, Miami, and San Diego, and ahead of San Francisco and Los Angeles.

Boston MSA Hotel Trends

Source: STR

Source: STR

The preceding data illustrate the extent to which Boston was disproportionately affected by the pandemic, a dynamic attributable to Boston’s status as an early hotspot for the virus, its high degree of reliance on international travelers, and its more restrictive public policies around travel and public gatherings. As recently as February 2022, city officials required convention delegates to be masked and have valid and current vaccination documentation. In addition, leisure transient demand led recovery throughout the country, and Boston’s leisure-travel season is limited by its climate, as compared to warm-weather destinations.

Demand Factors

- Citywide conventions are the Boston hotel market’s backbone. In March 2022, public health risks decreased enough for the city to relax restrictions on convention attendance. Pent-up group demand helped carry the market through the spring, summer, and fall of 2022. Based on pre-bookings, the convention outlook for 2023 is excellent. The number of hotel room nights generated by the Massachusetts Convention Center Authority is expected to reach a new peak, aided in part by the presence of the new 1,054-room Omni Seaport, a second convention-headquarters hotel that opened in September 2021.

- Commercial demand continues to lag pre-pandemic levels, in part because work-from-home policies implemented during the pandemic have proven popular and effective substitutes for in-person attendance. The extent to which this approach signals a new normal will be borne out over time, but hotel operators must budget accordingly in the near term.

- In Boston, the three key demand segments (commercial, group, and leisure) have all historically included a significant share of international travel. While Boston is not a convenient geographic locale for national conventions, it is central for international conventions whose delegates come primarily from the United States and Europe. International travelers are a particularly lucrative demand source that should continue to revive over time, as public health policies return to normal.

- As with other lodging markets across the nation, demand from domestic leisure travelers has paced the Boston hotel market’s recovery. However, this segment is likely to bear the brunt of any recessionary impacts, and most operators are factoring a modest national economic recession into their 2023 outlook.

Transaction Activity

Few arm’s-length, single-asset sales have closed in the Boston-Cambridge urban core since the onset of the pandemic. The following three transactions are probably the most useful indicators of current market values.

- The 205-room AC by Marriott sold in October 2021 for $434,000 per room.

- The 1,220-room Sheraton Boston sold in February 2022 for $192,000 per room.

- The 225-room Loews Boston Hotel (renamed Hotel AKA following the sale) sold in August 2022 for $529,000 per room.

New Supply

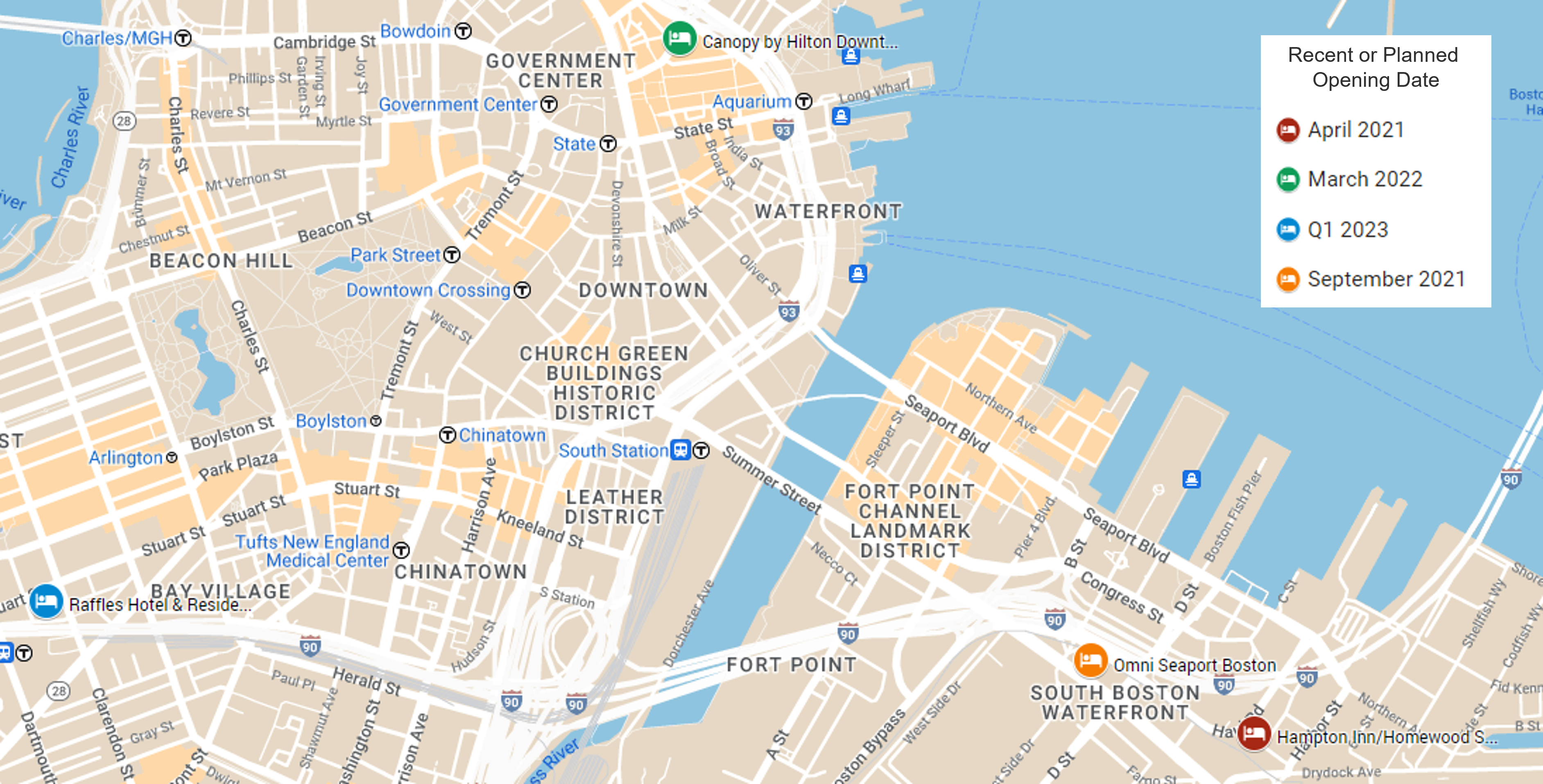

One of the great achievements of the Boston hotel market in 2022 has been weathering the impact of the new Omni Seaport with its 1,054 rooms, which opened in September 2021. The property has improved the marketability of the Boston Convention & Exhibition Center, to which it is attached, and is able to induce much of its own demand through its unique facilities and marketing efforts. Only one other hotel has opened recently, the 212-room Canopy by Hilton in March 2022, and only one new hotel is under construction, the 147-room Raffles Hotel. The map below illustrates the recent and planned new supply in Downtown Boston.

New Supply in Downtown Boston (as of December 2022)

Source: HVS

The Raffles Hotel will add to the congestion in the market’s luxury sector, which was previously expanded through the renovations of The Langham Boston and the former Taj Boston, now The Newbury, which were completed in June and May of 2021, respectively. Despite the new inventory, our research suggests the luxury sector has performed in line with the broader Boston market, with year-to-date RevPAR levels just below those recorded prior to the pandemic.

Looking Forward

In the early stages of the pandemic, there was a sense of a lack of horizon where market conditions might normalize. As 2022 comes to an end, it is now possible to realistically foresee a time when all demand channels are again vital and hotel markets in first-tier U.S. cities like Boston are once again thriving. Right now, that time seems most likely to be 2024, considering that federal monetary policy aimed at curbing inflation is expected to slow or even reduce economic activity through 2023. Prospects for a full inflation-adjusted return to normal in the Boston hotel market are further enhanced by a constrained new-supply outlook. Although the tone of this update is positive, Boston’s hotel market fundamentals are not yet sufficiently recovered to support financing for most new construction, particularly when interest rates are higher than usual. As such, there is virtually no chance that a full recovery will be delayed by supply growth. For hotel owners and operators who have suffered through an unprecedented external trauma that is well into its third year, this is very good news.

For more detailed forecasts or to inquire about a specific hotel project, contact Erich Baum, Brian Bisema, Raymond Parejo, or Kilian O’Brien with the HVS Boston office.