|

|

|

|

| June 1999 - Is the Pacific Asia travel and tourism industry,

and indeed the global travel and tourism industry, mired in an era of profitless

volume? In other words, has the swinging pendulum of unbalanced supply-and-demand

and excess competition led to a situation in which companies and countries

are just going for volume without making any profit of out of it?

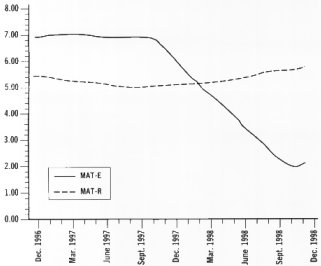

This issue has surfaced sporadically in many a travel trade show over the last few months and begs detailed analysis because it strikes at one of the foundation pillars of travel and tourism - that the industry is one of the biggest in the world, a major contributor to gross domestic product and a major creator of jobs. While that may all be true to some extent, is it one of the most profitable? Indeed, should profitability be a criterion at all? If so, how should it be measured? And what criteria should be set in place in order to enhance profitability? The phrase "profitless volume" surfaced in the travel and tourism industry about 10 years ago when the intense competition among Japanese tour operators seeking to obtain a piece of the action of the Japanese outbound 10-million programme led to massive discounting to the extent where the relentless pursuit of market share eroded bottom lines into what is euphemistically called "negative growth." This lesson of unbridled and imbalanced competition was apparently not learned. When Korea (ROK) followed Japan in opening up the floodgates of its outbound tourism, a huge number of travel agencies emerged, all pursuing their piece of the action. As the scales of competition tipped, prices plunged, taking with them quality of tours and industry profitability at large. Similar situations exist in Chinese Taipei and China (PRC). Indeed, throughout the Pacific Asia travel and tourism industry, the problem has been aggravated by the economic crisis which appears to be fading, but which is leaving behind a long wake that will take several years to fade. The latest scenario is emerging in the airline industry. At the recent PATA Annual Conference in Nagoya, Japan, both the mainline Japanese carriers, All Nippon Airways and Japan Airlines, described in great detail the problems they are facing with restructuring their companies and restoring them to profitability. Indeed, they are having to muscle in on each other's territory to win market share. The decline in both Japanese outbound and inbound travel has meant that the airlines are competing for a smaller cake, even as deregulation and liberalisation of the Japanese aviation industry has created more players competing for a share of that cake. At once, they have to cut costs, grow the market, invest in product and service improvements and eventually restore profitability. No one can venture a forecast as to when that will be achieved. At the March 1999 ITB in Berlin, Indonesian tourism officials pointed out that the devaluation of the Indonesia rupiah has hurt the country's foreign exchange earnings from tourism. While the country is clearly making huge amounts of money in rupiah, its earnings in "real terms" i.e., in much-needed foreign exchange, have declined from US $6.2 billion in 1996 to US $4.4 billion in 1998. Similar situations exist in Thailand. Perhaps the only exception is Korea (ROK), which has managed to grow its earnings in foreign exchange, but even here that is largely as a consequence of decreasing expenditures relative to receipts (see chart). The same situation exists in the hotel industry. According to hotel

and leisure industry consultants

The biggest problem that the industry is facing across the board, especially in the economically crisis hit countries, is that the debts incurred by both the travel and tourism industry companies, as well as the countries themselves, are in foreign exchange. Hence, the worse both the companies and countries are affected by the decline in foreign exchange earnings, the longer it will take to repay those debts, and the longer it will perpetuate the profitless volume factor. Clearly, the situation has benefited tour operators in many source markets, especially Europe. The advent of the single European market has led to major mergers and consolidations among European wholesalers who are also locked in a bitter fight for market share. To ensure profitability, they have to seek "the best possible rates" from their suppliers. While some wholesalers can in fact allow suppliers to increase rates in their devalued currencies, it still does not translate into an increase in foreign exchange earnings at the national level. While market forces rage, and the shakeouts continue in the face of imbalanced competition, the profitless volume pandemic could well spread. Indeed, to maintain their market shares in the face of the increased "value-for-money" factor of Pacific Asia destinations, other destinations in Africa and Latin America, where foreign exchange is also at a premium, are also having to drop prices. At the same time, the cost of attracting and servicing each tourist is rising for the national economies. This cost includes providing transport infrastructure (including aircraft purchases, airport terminals, cruise ports), upgrading technology, training and re-education, marketing, setting environmental controls and standards, and indeed paying out huge amounts of money in licensing, franchise, management and copyright fees. All of which begs the question: What is the real bottom-line benefit of the travel and tourism industry for the national economies, in valuable foreign exchange? One small step towards the long-term process of answering this question will be taken in June 1999 at the World Conference on the Measurement of the Economic Impact of Tourism. Organised by the World Tourism Organization (WTO), this conference aims to prove the true economic importance of tourism in hard facts and figures, by setting global standards for Tourism Satellite Accounts (TSA). Having done that, and trained their national statisticians to look closely at the figures, it will be only a matter of time before industry practitioners begin taking a closer look at the figures and questioning the net benefit to their countries. Like any corporate balance sheet, it is the bottom-line that will count. Counter-Trends:

This inaugural piece on counter-trends is intended to trigger some questioning of many "conventional wisdoms" that have gained global acceptability as gospel truth but which are in fact, worthy of closer scrutiny and some pinch-of-salt flavouring. Over the last few years, the travel and tourism industry has been told incessantly about certain trends with which it "must" fall in line to ensure future survival and profitability. However, there is increasing evidence that not everything is turning out the way pundits forecast, nor indeed will turn out as such. Perhaps the most hyped is the impact of technology, which is seen as

the ultimate panacea. Below, we look at 10 factors that testify to its

flaws, fallacies and failures. While technology will solve some problems,

it will also create some new ones. While it can do much good, it can also

do some harm. The recent failure of three consecutive space launches provides

testimony to that.

Rather than just go with the flow, the travel and tourism industry, as one of the biggest purchasers of information technology, needs to pause, think, weigh the facts as well as the pros and cons, and ask the right questions: Can it swim against the tide? Or is it likely to be one of the rats following the Pied Piper of Hamelin? Indeed, what can the industry do to veer away from "high tech" and focus on "high touch"? Or, alternately, adopt a balanced approach that uses high tech to enhance high touch? Consider the following: 1. Paperless Society: Foremost among the many promises made about

the benefits of technology was that a paperless society would dawn almost

overnight after technology took hold. Has it? Quite the opposite appears

to have happened.

2. Information Overload: Perhaps why a "paperless society" has not evolved. With the amount of information in the past 30 years being equal to all the information in the past 300, and doubling every few years, the question that arises is: What are we going to do with information that "dies" every few weeks? 3. Where's the Free Time?: Yet another myth - a promise of plenty of free time for all, once technology becomes commonplace. No sign of it yet. The only ones with plenty of free time are those made redundant by technology. Those working it are working harder than ever. 4. Viruses and Y2K: Viruses wreak havoc on computer systems around the world, the latest being the Chernobyl, which wrecked many a computer. The hysteria over the Y2K is just beginning; the actual impact will be felt only on or around the turn of the millennium. Fixing the subsequent damage will take time, and money. 5. Overdependence on Outside Factors: With the sole exception of a few countries like Singapore, India and Malaysia, which are trying to cultivate strong domestic information technology industries, most of the other Pacific Asia countries are almost totally dependent on imports of both IT hardware and software. That, plus the huge amounts that have to be expended on maintenance, support and training, amounts to a constant drain of financial resources. 6. Growing Rich-Poor Income Gap: Thanks to technology, currency speculators and hedge fund operators can bankrupt countries by moving money from one country to another by pressing a few computer keys. The rich can become poor overnight, and in the case of the Asian economic crisis, many did. Those who have the knowledge to manipulate such information to their advantage invariably get rich. The poor invariably remain far behind. 7. Unending Costs in Re-Tooling, Re-Training, Re-Equipping: With technology becoming obsolete every few years, sometimes even months, the flow of "new, improved" products is unending. Aside from confusing company managers, they become a huge drain on costs as companies have to run faster just to mark time. Once in it, there is no going back. 8. End of Privacy: In May, The Economist ran a feature story and editorial on this subject, focusing on how information about what we buy, eat, watch and surf is available within companies and governments. It claimed nothing can be done about it and that because the upside outweighs the downside, the public just has to learn to live with it. Really? 9. Impact of TV and Internet on Children: Soon after The Economist article, both Time and Newsweek ran cover stories on the influence of unrestricted Internet access by children, and the many unseen predators who can prey on unsuspecting youngsters. Some flimsy rules and software programmes for blocking out harmful Web sites have been created. But anything blocked from one computer can be accessed from another. There is always a way to beat the system, and kids know it. 10. Impact of Biotechnology, Cloning and Genetic Engineering:

The wonders of nature were provided for the use of mankind, not for misuse

or abuse. As people destroy nature, are they trying to come up with replacement

products that can be created or manipulated? Whenever people take on Mother

Nature, the human race loses.

|

|

|