|

|

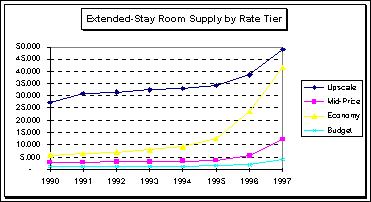

| Extended-stay hotel room supply in the United States increased more than 50 percent in 1997 over 1996. |

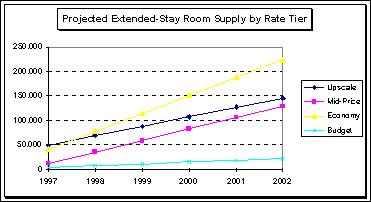

| There will be more economy-price than upscale extended-stay rooms before the end of 1998. This is a significant reversal from prior years and indicates a change in the way extended-stay lodging is used by American travelers. |

| Projected extended-stay hotel supply will be more than half a million rooms through 2002. At this level, extended-stay hotel rooms will represent some 12 percent of total lodging inventory. |

The database used in forming the estimations and projections in this

report 31 extended-stay brands as well as some independent hotels. There

are other independent extended-stay hotels that were not included, but

the sample represents most extended-stay rooms in the US. Brands are grouped

by the weekly room rate range in which their hotels conform. However, individual

hotels of a given brand may have weekly rates outside the ranges in certain

markets and we have adjusted for these variations.

Extended-stay room supply increased 54 percent during the first 10 months

of 1997 compared to year-end 1996. Supply gains in 1997 followed a 32 percent

increase in 1996 over 1995. Extended-stay hotel rooms currently represent

about 3 percent of total US hotel room supply. The graph following shows

the increase in extended-stay hotels rooms by rate tier since 1990.

Projected room additions through 2002 in the economy segment are also

the strongest, and this segment is projected to have the greatest number

of rooms before the end of 1998, as follows.

Assuming supply growth projections are fully realized through 2002, this represents a significant change from the current price distribution of extended-stay hotels and marks a change in the way Americans use extended-stay lodging. Use of extended-stay lodging will have expanded from the corporate expense-account market to encompass most demographic segments. Corporations are taking advantage of the availability of these facilities for training, relocation and temporary assignments at all levels.

According to Smith Travel Research, total US hotel room supply increased

at an average annual rate of 1.5 percent from 1990 through October 1997.

Assuming total room supply increases at the same rate through 2000 and

extended-stay hotel growth projections are fully realized, extended-stay

hotel rooms will account for about 12 percent of total US hotel room supply

through 2002.

Average extended-stay hotel occupancy was 79.6 percent through October

1997, which was the same as year-end 1996 occupancy despite a 54 percent

increase in supply. This represents remarkable expansion of demand in response

to new product. The table following shows historic extended-stay hotel

demand growth.

| 1990 | 1991 | 1992 | 1993 | 1994 | 1995 | 1996 |

|

|

| Rooms | 37,330 | 41,610 | 42.950 | 44,907 | 47,077 | 52,404 | 69,349 | 106,929 |

| Occupancy | 73.3% | 73.4% | 76.2% | 79.1% | 80.9% | 80.5% | 79.6% | 79.6% |

| Rooms Sold (thousands) | 9,987 | 11,148 | 11,946 | 12,965 | 13,901 | 15,401 | 20,154 | 31,067 |

| Demand Growth | 12% | 7% | 9% | 7% | 11% | 31% | 54% |

Extended-stay room demand grew at an annualized rate of 54 percent in 1997 compared to 1996. This equates to an annualized gain of almost 11 million room nights in 1997 following an increase of nearly 5 million room nights in 1996 compared to 1995. New extended-stay rooms are being absorbed rapidly on a national level.

Occupancy is highest in the budget segment, which is consistent with the inverse relationship between average length of stay and price. (Average length of stay increases as price decreases and a long average stay tends to promote higher occupancy.) Ultimately, we project that occupancy in economy and mid-price segment will be higher than in the upscale category. Lower occupancy in these segments compared to the upscale tier reflects a relatively high number of new rooms currently under absorption in mid-price and economy segments.

The overall average rate for extended-stay hotels declined to $67 in 1997 from $71 in 1996. Average rates rose in the upscale segment, but the overall average rate declined because of the large increase in lower-priced extended-stay hotels.

We project that the strongest average rate increases will occur in the mid-price segment because of the projected increases in the proportion of hotels price in the upper end of this category.

Extended-stay is a dynamic and rapidly evolving segment of the lodging industry. Its presence will be felt at all lodging price points within two years. Hotel owners and operators need to be aware of extended-stay and knowledgeable about these products so they can adapt their strategies to the marketplace of the year 2000.

|

|