advertisement

Hotel Capitalization Rates Stabilize as Market Forces

Create State of Equilibrium

|

News for the Hospitality Executive |

advertisement

|

By Suzanne R Mellen, CRE, MAI, ISHC, FRICS

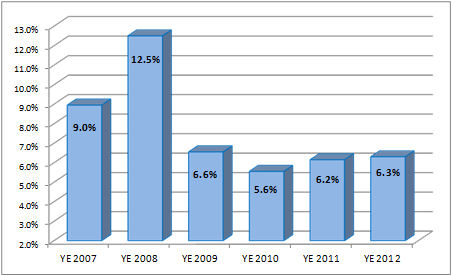

February, 2013 Hotel capitalization rates are stabilizing due to the counter balancing forces of a healthy transaction market, a shortage of product for sale, the low cost of capital and the slowing of net income gains. This article discusses these forces and presents data illustrating these trends. Counter balancing forces at work in the hotel investment market have created a state of equilibrium that has stabilized capitalization rates for the near term. The availability of low cost capital, healthy but not frenzied transaction activity, generally strong and slowly improving hotel operating performance, offset by limited inventory and political and economic uncertainty have resulted in the most stable market environment in recent times. This article, which is published biennially[1], discusses trends in hotel capitalization rates and provides an outlook for 2013. During times of robust investor activity, downwards pressure is exerted on capitalization rates due to strong competition for quality assets. While this past year was a relatively strong year in terms of sales activity, the number of major sales, defined as assets that sell for $10 million and over, declined by 12% from the level witnessed in 2011, based on preliminary data for the year, illustrated in the chart below. Note that this sales data excludes portfolio sales. The dollar volume of sales transactions declined even more, as the number of large, high price per key transactions sold during 2012 was below that of 2011. The average price per key declined from $209,000 to $181,000 as a result of the change in mix of assets being transacted. Private equity was significantly more active in 2012 than in 2011, when REITS dominated the market. However, sellers were less inclined to place their assets on the market, creating a dearth of inventory for sale. The expectation that improvement in earnings and renewed activity by REITS will lead to higher pricing in 2013 is credited with the seller pullback last year. Major

Hotel Sales Transactions (Non-Portfolio >$10 million)

While lodging REITs were the buyers in 29% of the transactions in 2012, as compared with 43% in 2011, activity by publicly traded REITS gained momentum as the year progressed, due to improvement in REIT stock prices. The major sales activity in 2012 reflects a healthy, active market, but not a buying frenzy, with investors pursuing strategic hotel acquisition opportunities despite the uncertain trajectory of the US economy. Participants interviewed for this article expressed optimism for transaction activity in 2013, as more sellers place their assets on the market and both REITS and private equity pick up their acquisition activity. The potential for retrenchment by lenders and market participants if the stock market reacts negatively to a prolonged debt ceiling and deficit reduction battle in the first quarter of 2013 does not appear to be suppressing investor sentiment for the moment. Hotel capitalization rates derived from actual sales transactions have risen since their nadir in 2010, when investors were buying assets based on net income that was severely depressed due to the impact of the Great Recession. With the recovery in hotel performance, much of the expected improvement in net operating income has been realized; thus, the potential for future upside has moderated, resulting in a rise in capitalization rates from 2010 to the present. Many hotels have or soon will be reaching prior peak occupancy levels. Future gains in revenue and net income are still anticipated as average rates rise faster than inflation. However, in many markets just how much and how fast revenue will continue to climb is uncertain. Some markets have already witnessed two years of strong, above inflationary average rate growth, and just how much more consumers are willing to pay before being priced out of the market is unclear. Those markets that are lagging in their recovery may have a difficult time raising average rates as aggressively as they did in the past due to uncertain economic conditions. At the same time, we are beginning to see increases in the supply pipeline, particularly for extended-stay and select service product, which may impact existing hotels. While most hotel investors remain very bullish about future net income gains, due to what is perceived as a supply/demand imbalance in favor of demand, investors are becoming less aggressive in their forecasts of future operating performance, wary of overpaying in a market laden with uncertainty. These factors have translated into a stabilization of capitalization rates, as evidenced by the data derived from hotel transactions that HVS appraised at the time of sale. The following chart sets forth the historical trend in full service hotel rates of return. Derived and

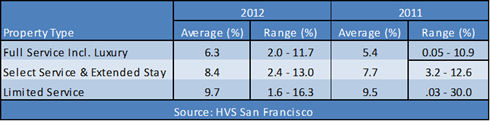

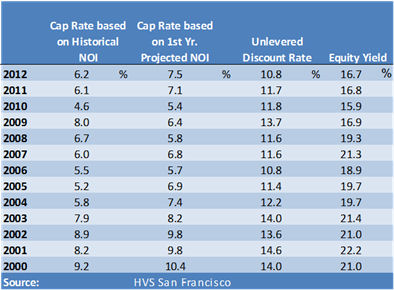

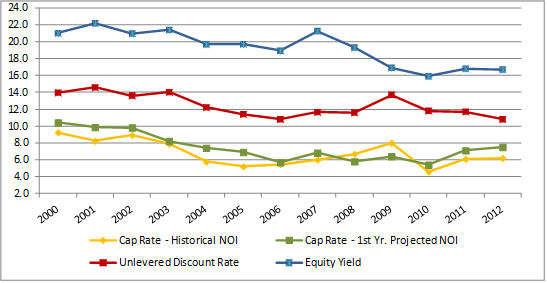

Projected Capitalization and Discount Rates – Select Set of Full

Service Hotels

While capitalization rates based on historical and projected first year net income trended up slightly from 2011 to 2012, unlevered discount rates[2] have declined by 90 basis points, reflecting 1) a moderation of projected future gains in NOI, and 2) extremely low interest rates and the increasing availability of debt financing. At the same time equity return requirements remained fairly stable from 2011 to 2012, and well below their rates prior to 2009. This same data is reflected in the following chart. Capitalization rates based on historic net income remain healthily above going-in capitalization rates based on projected first year net income, reflecting that the market anticipates continued, albeit more moderate, improvement in hotel net income. Derived and

Projected Capitalization and Discount Rates – Select Set of Full

Service Hotels

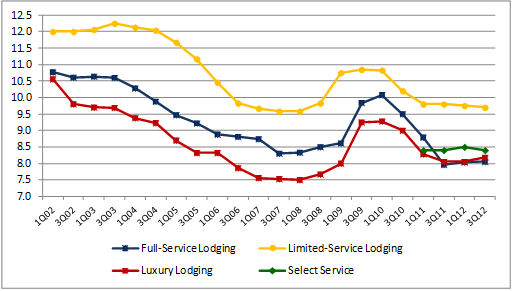

Source: HVS San Francisco Capitalization rates derived from all of the sales data in the HVS Sales Database, based on historical net income at the time of sale divided by the sales price, support these trends, as evidenced in the following chart. Capitalization rates for full service, select service and extended-stay and limited service products have trended up over the past year, and are currently at a point of stabilization. Capitalization Rates Derived From Sales

Transactions - Historical NOI Hotel

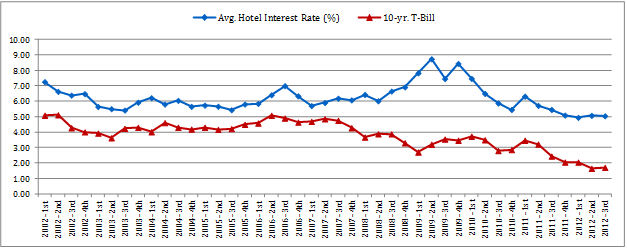

Capitalization Rate Comparison – PWC Real Estate Investor Survey Data The cost of capital is the primary driver of cap rate trends. The Federal Reserve has maintained the federal funds rate below .25% since December of 2008, the lowest rates over the past 60 years, providing an unprecedented interest rate environment. With the slowing of economic growth over the past year and the Federal Reserve’s commitment to maintain low interest rates through 2014, hotel mortgage interest rates are at their lowest level since we began tracking them in 1973. With the return of lenders to the market and a revitalized CMBS market, hotel owners fortunate enough to have a well performing hotel with a good physical, market and borrower profile, have been flocking to refinance their properties with fixed interest rates mortgages with interest rates at or even below 5% during the fourth quarter of 2012. Hotel mortgages maintain a healthy 300 basis point spread over the yield on the 10-year t-bill, as evidenced in the following chart. Low interest rates have helped to keep hotel capitalization rates low, offsetting the rise that might be expected as net income gains lessen over time. Hotel

Mortgage Interest Rate Trends  Source: HVS Capitalization rates derived from lodging REIT Enterprise Value and EBITDA further illustrate the current relatively stabilized environment for hotel investments. The stock market is generally a leading indicator, as is reflected in the spike in cap rates in 2008, before a rapid moderation as the market anticipated normalization in 2009 subsequent to the financial crisis in late 2008. Capitalizaton

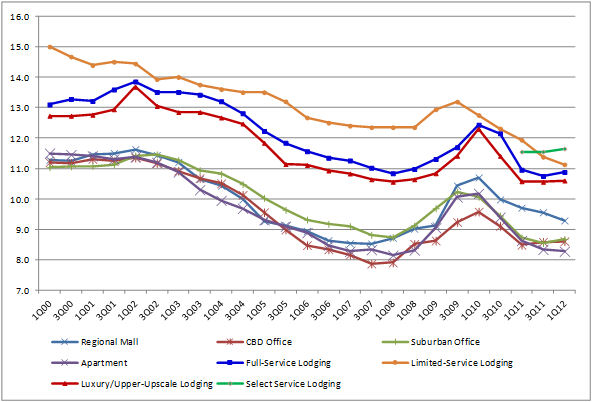

Rates Derived From Select Lodging REIT Data The following chart sets forth discount rates, or unlevered internal rate of return expectations, derived from the PWC Real Estate Investor Survey for the four lodging product sectors (with select service beginning in 2011), as well as discount rates for other commercial and multi-family residential real estate categories for comparison. Discount rates for other commercial and residential real estate continue to generally follow the same trend as hotel discount rates, rising significantly during the financial crisis in 2008 and 2009, then falling in 2010 and reaching a point of stabilization in the first quarter of 2011 through the present. Hotels continue to retained their significant yield premium over other real estate assets. PWC

Real Estate Investor Survey – Discount Rates

Given the factors at play in the hotel investment market at this time, we anticipate that hotel capitalization rates will remain generally stable throughout the year, barring any unforeseen outcome of the debt ceiling and deficit reduction battle over the next few months. The Fed has committed to maintain a low interest rate environment through 2014 and lenders still seem favorably inclined to continue to lend on hotels, as the hotel industry is viewed as being in the early innings of a long term recovery, due to continuing economic growth and limited new supply. Equity return requirements remain moderate, due to the lack of yield on alternative investments. As sellers increasingly identify this as an opportune time to place their assets on the market, transaction activity will pick up, creating downwards pressure on cap rates which will continue to offset the rise in cap rates due to moderation in NOI gains. These counter balancing forces have placed us at the current point of capitalization rate stabilization, a welcome relief after the volatility of the past five years. _____________________________ [1] www.hvs.com/publications/mellen [2] Free and clear internal rate of return based on a ten year forecast of income and expense at the time of sale, based on HVS appraisals at the time of the transaction  About Suzanne R Mellen Suzanne R. Mellen is the Senior Managing Director of the San Francisco, Los Angeles and Las Vegas offices of HVS, heading the Consulting & Valuation and Gaming Services divisions. She has been evaluating hotels and associated real estate for 35 years, has authored numerous articles, and is a frequent lecturer and expert witness on the valuation of hotels and related issues. Ms. Mellen has a BS degree in Hotel Administration from Cornell University and holds the following designations: MAI (Appraisal Institute), CRE (Counselor of Real Estate), ISHC (International Society of Hospitality Consultants) and FRICS (Fellow of the Royal Institution of Chartered Surveyors). About HVS HVS is the world’s leading consulting and services organization focused on the hotel, restaurant, shared ownership, gaming, and leisure industries. Established in 1980, the company performs more than 2,000 assignments per year for virtually every major industry participant. HVS principals are regarded as the leading professionals in their respective regions of the globe. Through a worldwide network of 30 offices staffed by 400 seasoned industry professionals, HVS provides an unparalleled range of complementary services for the hospitality industry. For further information regarding our expertise and specifics about our services, please visit www.hvs.com. |

| Contact:

Suzanne Mellen HVS San Francisco 100 Bush Street Suite 750 San Francisco, CA 94104 +1 (415) 268-0351 direct +1 (415) 896-0516 fax [email protected] www.hvs.com |