advertisement

|

News for the Hospitality Executive |

advertisement

|

by Elaine Sahlins

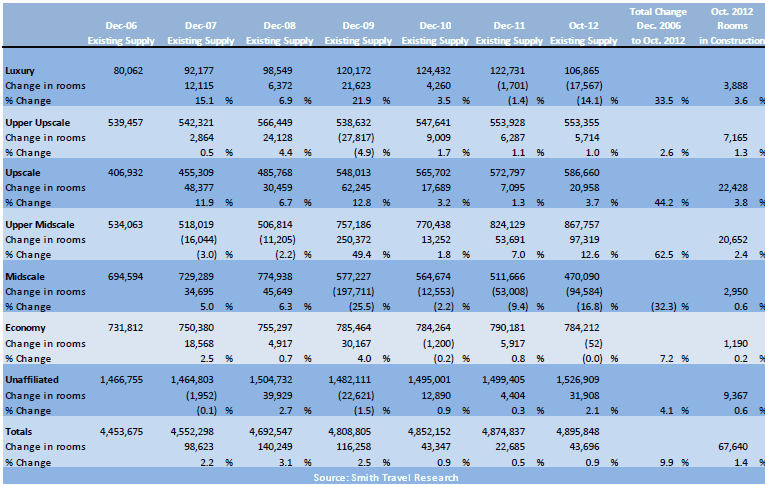

February 8, 2013 Since 1976 HVS has tracked hotel construction costs throughout the United States. The survey considers data for six lodging types: Economy/Budget Hotels, Midscale Hotels w/o F&B (without Food and Beverage), Extended-Stay Hotels, Midscale Hotels w/ F&B (with Food and Beverage), Full-Service Hotels, and Luxury Hotels and Independent Resorts. The 2012/13 Hotel Development Survey reports updated per-room development costs through the end of 2012. Each year HVS Consulting and Valuation researches development costs from our database of hotel construction budgets, industry reports, and franchise offering circulars. These sources provide the basis for the range of component cost per room. New project construction cost data collected each year may change the upper and lower data points in the range and/or impact the mean and median of the construction cost components. The upper and lower ends of the ranges are also influenced by changes in construction cost components derived from published sources, industry indexes, and information from architects, contractors, developers, lenders, and other professionals involved with hotel development projects. The 2012/13 development cost survey reflects ranges of development costs in each category. The survey is not meant to be a comparative tool to calculate changes from year to year—rather, it represents the true costs of building hotels across the United States. The data represent a wide array of geographical locations, from tertiary markets in the Southwest to mid-Manhattan. The development costs of the same hotel product, for example a select-service Fairfield Inn or Holiday Inn Express, can be more than three times higher from one locale to another. Although hotel performance has rebounded in many major U.S. markets, financing continues to be the key component to unlocking new hotel construction. Since 2010, many hotel markets in the U.S. experienced considerable rebound in their operating performance. The majority of major markets have recovered or are expected to recover by year end 2013. According to Smith Travel Research (STR), occupied room night demand growth nationally for the 12 months ending September 2012 averaged 3.3% and average rates increased 4.2%. Despite these positive trends, hotel construction remains relatively constrained. While there were more rooms under construction at the end of October 2012 as compared to the year-end 2011, there were fewer active projects in the pipeline. Hotel room inventory data from STR show the recent national trends in new hotel supply, as reflected in the following chart. CHART

1 - NATIONAL HOTEL ROOM SUPPLY GROWTH – DECEMBER 2009 THROUGH OCTOBER

2012

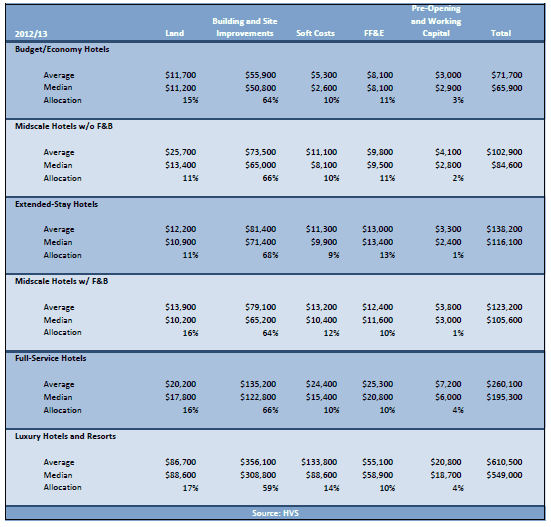

The improvement in operating performance has spurred some projects to be brought off the shelf and other new developments to proceed. As would be expected, new hotel construction is concentrated in the midscale through upscale segments. These STR Chain Scales represent selectservice and extended-stay brands, including such property types as Courtyard by Marriott, Staybridge Suites, Hampton Inns, and Hyatt Place. These properties are characterized by lower construction costs, lower labor costs and higher profit margins than those of full-service hotels. Their brand affiliations are important to lenders; enabling developers to secure construction funding, primarily through existing relationships with regional or national banks. Non-traditional financing sources are being sought for some new projects. Most prominently, the EB-5 Visa program has become a sort of global crowd funding1 mechanism for hotel developers. Administered by the US Citizenship and Immigration Service (USCIS), the program requires that a project create or preserve at least 10 full-time jobs for qualifying US workers within two years (or under certain circumstances, within a reasonable time after the two-year period) of each immigrant investor’s admission to the United States as a Conditional Permanent Resident. The minimum required capital per investor is $1,000,000 in urban areas or $500,000 in rural areas. When approved, the EB-5 investor (and spouse and children) is granted conditional permanent residency for a two-year period. The program is especially suitable for larger hotel projects with their substantial employment practices. Hospitality sector projects being funded using EB-5 programs include casinos, select-service and urban full-service hotels. HVS has provided hotel market analyses and appraisals for several EB-5 program applications. Development Cost Changes The cost of developing hotels generally continues to escalate, although cost changes for the different categories tracked in the HVS Hotel Development Cost Survey were not uniform. Land transactions for new hotel construction are more prevalent than in recent years. In urban and suburban markets, attractive hotel sites are being sourced for other real-estate projects such as apartment and mixed-use projects, which can sometimes be more feasibly developed, driving up the cost of securing good hotel sites. Developers of large-scale mixed-use projects are still considering hotel use in the plans, but many are proceeding with other parts of the development first. Some hotel brands, such as Embassy Suites, are developing prototypes that can be built on smaller sites. Other developers are going forward with projects that were shelved during the recession, are contributing the already-owned land as part of the project equity. Our recent work on these types of projects, using the residual value to the land in a feasibility analysis, often shows that good hotel sites have appreciated significantly since 2009. Competing forces are affecting materials and labor costs, but the view from the construction industry is that these costs are starting to increase and will continue to do so. Labor remains the highest component of construction cost. Specialized construction labor saw modest gains in wages throughout 2012. Many firms that had frozen wages beginning in 2009 are now increasing wages. Increased construction expenditures also manifest in some material pricing: In 2011 and 2012, the price of gypsum, copper pipe, and plywood exceeded inflation. But, changes in the business practice of construction are helping to contain some of the expense. Many construction firms are opting for lower-priced negotiated contracts rather than design-bid-build. Conversely, the cost for some materials, particular lumber, remains low. While the housing market is starting to revive, production is well below peak 2005 to 2007 levels; suppressed overall demand for lumber continued to depress pricing through the first half of 2012. However, with the increase in activity in the housing market toward the end of the year, suppliers started raise prices. Overall, the annual inflation for construction materials tracked close to 2.5% by the end of 2012. As in 2011, industry surveys and development budgets indicated generally inflationary growth for construction materials. The cost of materials associated with infrastructure projects was stable while materials used in high-end finishing work increased in price. Building costs are also tied to oil costs; oil prices remained weak during the third quarter of 2012. Changes in the prices of materials varied. Plywood costs increased significantly over the course of 2012 while copper pipe declined 17% during the same period. Hurricane Sandy’s impact on material pricing is not yet known. Construction costs remain the highest in high-labor cost markets such as San Francisco, Boston, Chicago, Philadelphia, and New York. According to RS Means, the lowest-cost market in which to build a hotel is Winston-Salem; the reported difference between New York and Winston-Salem is 74%. Many construction industry experts believe innovation and technology will be the keys to controlling costs in the future. As labor costs continue to rise, especially in urban areas, reducing the construction that is done manually will save money. In recent years, technology and collaborative design work methods have been effective in reducing costs, particularly in health-care facility development. Total Project Management (TPM) and Building Information Modeling (BIM) software allows architects, engineers, interior designers, space planners, general contractors, and sub-contractors to work together during the planning and design stages, developing building solutions early in the process to avoid costly change orders later. The use of portable devices at construction sites has also proliferated. Using tablets on-site, construction supervisors have been able to notate building plans based on actual conditions encountered and send those concerns directly to the project engineers and architects, avoiding time delays and expensive printed plan revisions. Designing pre-fabrication of building components, including electrical and mechanical components off-site, and then installing these components as needed can be more efficient. Hotel renovation and refurbishment programs remained a strong driver of FF&E purchasing in 2012. Hotels that are being upgraded to brand standards are being asked to do more quickly with less inconvenience to guests. While a collaborative renovation project team can expedite the process, the faster timing can also increase the manufacturing and shipping costs of the products. The higher cost of shipping is being noted as one of the major influences on cost increases. Choices such as stock fabric and carpet patterns rather than custom selections are used to keep overall timing and project costs down. Soft costs include entitlement and permitting costs, along with financing costs. While some entitlement costs increased as jurisdictions searched for additional revenue, the financing that was available was priced at lower interest rates than in prior years. Many hotel construction projects require a significant amount of equity. We have found that developers are more flexible with their investment expectations as their equity contributions increase and the cost of financing falls. Since 2007, the cost of building sustainably has become less expensive with a greater availability of sustainable materials. Hotel developers report the incremental cost of building a green hotel has decreased up to 60% over the past five years. The volume of hotel construction was much higher in 2012 than in the recent past, with limitedand select-service hotels being the dominant product being built. STR reports that 67,640 hotel rooms are currently under construction. While the amount of rooms under construction is significantly lower than 185,119 rooms that were under construction in December 2007, the current amount is 25% higher than the number of rooms being built at the end of 2011. Hotel developers and lenders are showing greater interest in proposing new projects as many markets are absorbing the supply that came on in recent years. With many market operating at historically high occupancy levels, we anticipate an increase in the number of proposed hotel projects, particularly in urban and suburban markets. Pre-Room Hotel Development Costs The nadir of hotel development costs in the most recent cycle was 2010. Because of the economic trends in the past five years, very few luxury and full-service hotels were proposed or developed. During the prior development cycle, a number of urban and resort properties were developed with per-room costs that set new highs. In the 1990’s, some hotel and resort project costs exceeded $1 million per room. At this point in the cycle, we are not seeing these types of developments proposed. The ranges in this survey reflect the current trends in both costs and product development. CHART

2 – 2012/13 HOTEL DEVELOPMENT COST SURVEY PER-ROOM AVERAGES (BASED ON

2011/12 AMOUNTS)

CHART 3 - 2010 HOTEL DEVELOPMENT COST

SURVEY PER-ROOM RANGE OF COSTS FOR 2012/13

It is important in this analysis to note that there is no uniform system of allocation for hotel development budgets. Hotel development costs are accounted for in numerous line items and categories. Individual accounting for specific projects can be affected by tax implications, underwriting requirements, and investment structures. For example, in a development project, FF&E installation and construction finish work can overlap. Accounting for these items is not always the same from one project to another. In addition, we recommend that users of the HVS Hotel Development Cost Survey consider the perroom amount in the individual cost categories only as a general guide for that category. The totals for low and high ranges in each cost category do not add up to the high and low range of the sum of the categories. None of the data used in the survey showed a project that was either all at the low range of costs or all at the high range of costs. A property that has a high land cost may have lower construction costs and higher soft costs. The total costs shown in the preceding table are from perroom budgets for hotel developments and are not a sum of the individual components. All individual property information used by HVS Consulting and Valuation for the development cost survey is provided on a confidential basis and is believed to be reliable. Data from individual sources are not disclosed. 1 Crowd funding or crowdfunding (alternately crowd financing, equity crowdfunding, or hyper funding) describes the collective effort of individuals who network and pool their money, usually via the Internet, to support efforts initiated by other people or organizations. ____________________________________________  About Elaine Sahlins About Elaine SahlinsElaine Sahlins holds an undergraduate degree from Barnard College, Columbia University in New York City and an MPS degree in Hotel Administration from Cornell University. After graduating from Cornell she worked for VMS Realty in Chicago analyzing hotel investments, and then went on to become a review appraiser in San Francisco at Security Pacific, which was subsequently acquired by Bank of America. She joined HVS in 1997 in the San Francisco office. Elaine assumed responsibility for the Hotel Development Cost Survey in 1998. About HVS HVS

is the world’s leading consulting and services organization focused on

the

hotel, restaurant, shared ownership, gaming, and leisure industries.

Established in 1980, the company performs more than 2,000 assignments

per year

for virtually every major industry participant. HVS principals are

regarded as

the leading professionals in their respective regions of the globe.

Through a

worldwide network of 30 offices staffed by 400 seasoned industry

professionals,

HVS provides an unparalleled range of complementary services for the

hospitality industry. For further information regarding our expertise

and

specifics about our services, please visit www.hvs.com.

|

| Contact:

HVS

— San Francisco 100 Bush Street Suite 750 San Francisco, CA 94104 +1 (415) 268-0347 direct +1 (415) 869-0516 fax [email protected] |

To Learn More About Your News Being Published on Hotel-Online Inquire Here