advertisement

Lodging Econometrics Reports Asia Pacific Pipeline Stands at 2,317

Projects with 1,646 Under Construction Accounting for 44% of All Rooms

in the Global Pipeline

|

News for the Hospitality Executive |

advertisement

October 2012 - Asia

Pacific

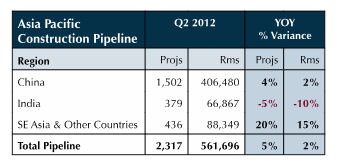

Pipeline totals, standing at 2,317 projects/ 561,696 rooms, hit an

all-time

high at the end of 2Q. There are 1,646

projects already Under Construction, representing a very high 71% of

total

Pipeline projects, as both Construction Starts and New Project

Announcements

into the Pipeline have remained strong.

Throughout the Asia Pacific region, there has been a rush to get development projects funded and into the ground in anticipation of the longer-term effects of the economic slowdown, underway since the second half of 2011. Nonetheless, the region still represents the greatest growth potential available for global franchise companies. The region accounts for a whopping 44% of all rooms and a third of all projects in the current global Pipeline.  China has the

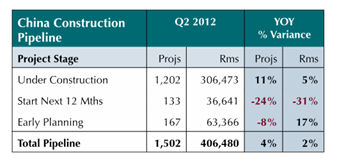

largest Pipeline in the world, by room count.

At 406,480 rooms, China accounts for a third of all global

rooms under

development. With 1,502 Pipeline

projects, China is second only to the United States.

Projects and rooms already Under Construction,

as well as Construction Starts, were at all time highs in Q1, as were

total

rooms in the Pipeline. The three metrics

tailed a bit in Q2, indicating the likely onset of a new downtrend from

the

development peak caused by the long anticipated global slowdown. New Hotel Openings peaked in 2010 at 966

hotels/ 136,812 rooms as a longer-term slowdown, albeit one with a

moderately

declining slope, has now set in. China has the

largest Pipeline in the world, by room count.

At 406,480 rooms, China accounts for a third of all global

rooms under

development. With 1,502 Pipeline

projects, China is second only to the United States.

Projects and rooms already Under Construction,

as well as Construction Starts, were at all time highs in Q1, as were

total

rooms in the Pipeline. The three metrics

tailed a bit in Q2, indicating the likely onset of a new downtrend from

the

development peak caused by the long anticipated global slowdown. New Hotel Openings peaked in 2010 at 966

hotels/ 136,812 rooms as a longer-term slowdown, albeit one with a

moderately

declining slope, has now set in.With the economy slowing abruptly in recent months, developer sentiment is far more restrained and risk adverse than before. The economic turmoil in Europe and a slower than expected recovery in North America are the immediate concerns. Neither situation seems to offer China any chance for near term relief. In response, China has initiated a flurry of new government sponsored infrastructure projects and has instructed their lending institutions to liberalize lending practices. These stimulus remedies have worked in the past, although they can cause longer-term problems like spiraling inflation and an acceleration in debt defaults. For sure, new government leadership coming into office next year will have additional economic stimulus at the top of their agenda too.  India’s economy

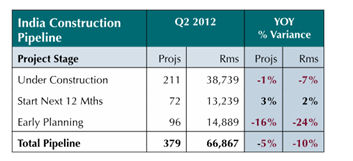

has been cooling for some time. Its

Pipeline, the third largest in the world, has 379 projects/ 66,867

rooms at the

end of 2Q 2012, down 5% and 10% respectively, year-over-year (YoY). More significantly, it is down 17% for both

projects and rooms since the peak set in Q4 2010. India’s economy

has been cooling for some time. Its

Pipeline, the third largest in the world, has 379 projects/ 66,867

rooms at the

end of 2Q 2012, down 5% and 10% respectively, year-over-year (YoY). More significantly, it is down 17% for both

projects and rooms since the peak set in Q4 2010.While the back-end of the Pipeline has declined, counts for hotels currently Under Construction have been rather consistent for the last 10 quarters, fluctuating narrowly in a broad topping out formation. As a result, LE’s forecast calls for an acceleration of new hotels coming online as the front end of the Pipeline begins to unfold. 83 hotels/ 14,457 rooms are scheduled to open in 2012, 72 hotels/ 13,067 rooms in 2013 and 106 hotels/ 17,982 rooms in 2014. Despite a stalling economy,

India is still looked on as a

country of great opportunity, particularly for economy and midscale

global

brands. Accor recently announced an

aggressive plan to add 75 hotels over the next three years, while

Carlson

Rezidor entered into a strategic partnership to add 49 Park Inns in

north and

central India. A softening economy,

rising interest rates, an inadequate infrastructure and a difficult

permitting

and approval process make for a challenging environment for developers.

Southeast Asia

and the remaining 24 other countries in the region combine for a

Pipeline of

436 projects/ 88,349 rooms, up smartly by 20% and 15% respectively YoY. Indonesia

is booming. It’s always a bit of a

surprise to see that it has the world’s 5th largest Pipeline, ahead

of such other countries as the United Kingdom, Canada, Russia, Mexico,

Saudi

Arabia, Dubai and Germany. Three of the

world’s five largest Pipelines are located in the Asia Pacific region. Southeast Asia

and the remaining 24 other countries in the region combine for a

Pipeline of

436 projects/ 88,349 rooms, up smartly by 20% and 15% respectively YoY. Indonesia

is booming. It’s always a bit of a

surprise to see that it has the world’s 5th largest Pipeline, ahead

of such other countries as the United Kingdom, Canada, Russia, Mexico,

Saudi

Arabia, Dubai and Germany. Three of the

world’s five largest Pipelines are located in the Asia Pacific region.About Lodging Econometrics Launched in 1995 with the

encouragement of Wall

Street analysts and many Lodging Industry leaders, Lodging Econometrics

(LE) is the recognized authority on all hotel real estate including the

Development Pipeline and the Sale and Transfer of Lodging Real Estate

nationwide. LE also compiles and maintains the Industry's Census of

Open and Operating Hotels including the Names of Owners &

Management for more than 60,000 hotels in the U.S. and Canada..

|

| Contact: Lodging Econometrics |