advertisement

Lodging Econometrics Q2 2012 U.S. Lodging Report Reveals Development Trends

Are On The Rise with 1,180 New Project Announcements in the Pipeline

|

News for the Hospitality Executive |

advertisement

|

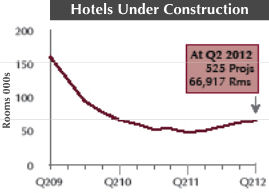

September 2012 - Like the slow but

steady expansion in the overall economy

and the improvement in Lodging Industry operating statistics, a period

of

moderate growth in Pipeline metrics has been underway for a while.

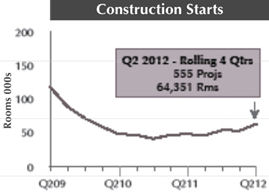

The annualized four-quarter trend line for Construction Starts at 555 projects/ 64,351 rooms is up from the bottom for the sixth consecutive quarter and is at its highest level in 10 quarters. The uptick in Construction Starts is due largely to the commencement of previously stalled projects in the pipeline while developers were awaiting evidence of a sustained operating recovery.

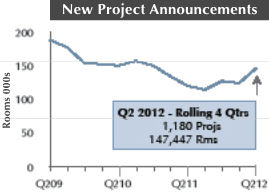

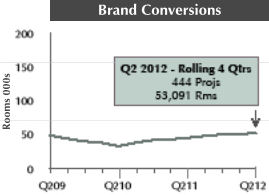

The most significant indicator of future Pipeline growth is New Project Announcements (NPAs). At 1,180 projects/ 147,447 rooms, the annualized four-quarter trend line is up from the previous cyclical bottom for the third consecutive quarter and is at the highest level in six quarters. Brand Conversions are slowly increasing, as well. The annualized four-quarter trend line at 444 projects/ 53,091 rooms is up from the bottom for the eighth consecutive quarter and is at a 13 quarter high. Based on current construction trends, these pipeline metrics support LE’s initial Forecast for New Hotel Openings in 2014 of 446 projects/ 48,335 rooms. This is a 31% room count increase and the first substantial upturn from the bottom of 346 projects/ 37,200 rooms set in 2011. Looking Ahead Following the bottom of a previous real estate cycle, a fundamental improvement in developer sentiment is necessary to begin a new cycle. Confidence is rekindled when developers conclude that an improving economy is not likely to fall back into recession and that lodging demand has turned around sufficiently to minimize any risk of a major reversal. These thresholds have been reached in the last two years, and the nascent beginnings of a new real estate cycle have begun to take shape. When discussing industry growth patterns, modest and measured growth can often create impatience and frustration. For sure, recovery in the Lodging Industry has been slower than hoped for, but none-the-less, improvements are solid. LE expects that both ADR and RevPAR will exceed previous cycle highs in 2013, perhaps Occupancy too, but if not, then in 2014. It’s LE’s expectation that once the election season is over the administration will be able to build a bi-partisan political consensus to ensure that job growth policies are at the top of the nation’s agenda. Job growth is the key to improving consumer spending, which is necessary to trigger investment by the business community. That will then spur further lodging demand and propel hotel development forward at a faster pace, well into the middle of the decade. About Lodging Econometrics Launched in 1995 with the encouragement of Wall Street analysts and many Lodging Industry leaders, Lodging Econometrics (LE) is the recognized authority on all hotel real estate including the Development Pipeline and the Sale and Transfer of Lodging Real Estate nationwide. LE also compiles and maintains the Industry's Census of Open and Operating Hotels including the Names of Owners & Management for more than 60,000 hotels in the U.S. and Canada. |

| Contact: Lodging Econometrics |