advertisement

|

News for the Hospitality Executive |

advertisement

|

by Andy Reed

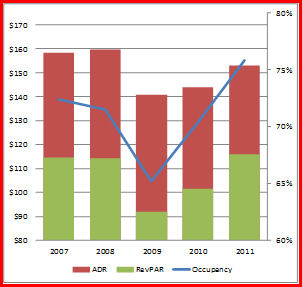

March 2012 2011 Year in Review – Miami The Third Quarter 2011 Florida Newsletter (“Miami’s Hotel Performance and Values are Set to Heat Up”) highlighted the fact that Miami’s hotel sector was displaying very strong market indicators. The investor and market participant sentiment was positive and both debt and equity investors were bullish on Miami – and for good reason. Year-end 2011 RevPAR (revenue per available room) for hotels throughout Miami-Dade County surpassed the 2007 benchmark, or what is generally regarded as the peak of the market. The Miami Beach, Downtown/Brickell, and the Airport markets, specifically, performed strongly and are poised to have another great year. Miami has established itself as a gateway hospitality market and is favorably viewed by conservative debt investors who are ready and willing to make loans on existing and proposed hotel assets in the market area. The Third Quarter 2011 article leaned on indicators such as hotel transaction volume, trends in domestic and international visitation, growing international source markets (notably Brazil, Argentina, and Colombia), strong occupancy and average rate trends, and hotel investment and new developments as we concluded significant upside existed on a wide variety of local assets. Hotel performance and values not only improved, but the market value for a significant portion of residential and commercial real estate increased dramatically and far ahead of the pace that was projected by the bulk of industry experts in 2010 and early 2011. For example, it was anticipated that the overbuilding of residential condominiums in the Brickell submarket would take years to be fully absorbed – an influx of unforseen foreign investment resulted in this excess condominium supply being absorbed well ahead of projections. Trends in office and retail vacancy and rental rates also confirm the city’s strong economic recovery and are reflective of the city’s status as a gateway market. Revenue per Available Room in Miami Hotels has Exceeded the 2007 Peak  As illustrated, revenue per

available room (“RevPAR”) in 2011 ($115.85) has exceeded the 2007

RevPAR peak

($114.71) as a result of very strong occupancy performance.

As a result of the economic downturn, a very

limited amount of hotel development commenced in 2009, 2010, and 2011

which has

allowed existing hotels to benefit from growing demand levels by

achieving

historic occupancy levels. With

tighening corporate and personal budgets in 2009 and 2010, consumers’

price-sensitivity increased dramatically and hotels were forced to rely

more on

discount, wholesale, and third-party entities to sell room nights, all

of which

contributed to the decline in average rate.

The challenge many operators now face is yield management: hoteliers

must strategically phase out the lower-rated discounted demand that

properties

relied on during the downturn. With occupancy

at peak levels, owners and operators in Miami are now in position to

employ

yield management strategies; potentially at the expense of occupancy,

but to the

benefit of overall RevPAR levels. We

anticipate strong rate growth in 2012 throughout much of the

county. This newsletter also identifies a variety of

hotel development projects within Miami-Dade county that will have an

effect on

the hotel landscape. As illustrated, revenue per

available room (“RevPAR”) in 2011 ($115.85) has exceeded the 2007

RevPAR peak

($114.71) as a result of very strong occupancy performance.

As a result of the economic downturn, a very

limited amount of hotel development commenced in 2009, 2010, and 2011

which has

allowed existing hotels to benefit from growing demand levels by

achieving

historic occupancy levels. With

tighening corporate and personal budgets in 2009 and 2010, consumers’

price-sensitivity increased dramatically and hotels were forced to rely

more on

discount, wholesale, and third-party entities to sell room nights, all

of which

contributed to the decline in average rate.

The challenge many operators now face is yield management: hoteliers

must strategically phase out the lower-rated discounted demand that

properties

relied on during the downturn. With occupancy

at peak levels, owners and operators in Miami are now in position to

employ

yield management strategies; potentially at the expense of occupancy,

but to the

benefit of overall RevPAR levels. We

anticipate strong rate growth in 2012 throughout much of the

county. This newsletter also identifies a variety of

hotel development projects within Miami-Dade county that will have an

effect on

the hotel landscape.

Current Status of the Hotel Transaction Market in South Florida Hotel transaction volume is a critical guage which is regularly used to measure the health of the hospitality market. Keeping in regular contact with hotel brokers who actively work in the transaction market is an important part of the work HVS performs. In addition to the volume of transactions, the disparity between the asking price, the bid price, and the final sale price, the investment parameters used to complete a deal (such as capitalization rates, required debt and equity yield rates, loan-to-value or debt-to-equity rates, and projected debt coverage ratios) are excellent indicators. Recent notable transactions in the southeast region of Florida have been presented in the following table. The “upcycle” in Miami should continue, noting that Smith Travel Research (STR) projects RevPAR in Miami to grow between 5.0-10.0% in 2012. In fact, Miami is one of only eight cities for which STR has projected RevPAR growth between 5.0% and 10.0% for the 2012 year.

The Downtown Miami/Brickell and Miami Beach submarkets are regarded by many as two of the more attractive and high-profile submarkets for hotel investment within the county; not surprisingly, these two submarkets also pose some of the greatest barriers to entry with regards to new development. While debt capital is generally more favorable in these high-performing submarkets, the costs associated with acquiring the land and the limited land availability often makes it difficult for a new hotel development to “pencil out.” These high development costs have not deterred all developers, however, as evidenced by the status of the current development pipeline. The future direction of hotel development in Downtown Miami/Brickell could very well hinge on the approval or denial of casino gambling permits, a hot topic that is currently being discussed in the Florida Legislature. While the discussion was recently tabled, the potential development looms over the hotel landscape of South Florida. An organization called the Genting Group, based in Malaysia, in a combined effort with Las Vegas Sands and other hopeful casino developers, is leading an attempt to convince the state’s legislators to approve the casino gambling license with a $3 billion master plan for a development called Resorts World Miami. The company has acquired roughly 30 acres of land in downtown Miami (including the Miami Herald building in May 2011 and the Omni Center in September of 2011) and is poised to begin development upon the Legislature’s approval. With the Omni being the first stage of Resorts World Miami, Genting could quickly offer casino jobs and revenues by fitting out the vacant 650,000-square-foot Omni Mall with a casino. At completion, the property will be roughly ten million square feet and feature four hotels (spanning 5,200 hotel rooms, or an increase of roughly 10% of the current inventory in Miami-Dade County), two residential condominium towers featuring approximately 1,000 units, more than fifty restaurants and bars, and luxury retail shopping mall, and 750,000 square feet of meeting and function space. Genting estimates that Resorts World Miami would create 15,000 direct and indirect temporary construction jobs and 30,000 permanent jobs in addition to between $1.4 to $2 billion in casino revenues, which would make the property the highest-grossing casino in the United States. The group is hoping for a completion date in the Fall of 2014. As the bill currently stands, though tabled for now, it would allow three casino licenses in South Florida. Miami Beach is one of the most sought after hotel real estate markets in the country, as evidenced by its year-end 2011 RevPAR of over $159. If one would isolate the Miami Beach submarket and compare it to the top 25 hotel markets in the country, as per data from Smith Travel Research, this submarket would rank second only behind New York City. Given the consistently strong RevPAR performance by hotels in Miami Beach and the future outlook of the submarket, which is poised for significant demand growth from both domestic and international visitors, it is no wonder why hotel investors are presently clamoring for opportunities to own a hotel on Miami Beach, either by acquiring an existing property or developing one from the ground up. The Miami International Airport is a key driver for room night demand throughout Miami and in the Airport/Civic Center and Doral submarkets, specifically. Hotel developers have taken notice that these two submarkets regularly post some of the highest occupancy levels in Miami-Dade county. In 2011, the Airport/Civic Center and the Doral submarkets achieved annual occupancy levels of 82.1% and 81.0%, respectively. Based on the multitude of research, interviews, and market studies that we have performed for clients in the area, we believe there are significant levels of unaccommodated room night demand in the submarkets. This conclusion is confirmed by the industry-wide rule-of-thumb that suggests unaccommated room night demand exists in a competitive market that posts annual occupancy levels above 70%. Miami-Dade County From the start of 2007 to the start of 2012, Miami-Dade County’s hotel room inventory increased by a compounded annual average rate of 2.2% per year, but from 2011 to 2012, as a result of the difficulty in sourcing financing and weak economic conditions in 2009 and 2010, room supply increased by only 0.6% while room night demand increased significantly. Increasing demand with little-to-no increase in room supply has resulted in strong marketwide hotel performance. According to data requested from Smith Travel Research, 54.9% of the hotel supply in Miami-Dade County is branded and 45.1% is independent. Luxury Of all of the branded hotel properties in Miami-Dade County, those considered to be “luxury” by Smith Travel Research have grown at the fastest rate from 2007 to January 2012, increasing by a compounded annual average rate of 3.7%. Presently there is one branded property classified as “luxury” in the development pipeline, being the 261-room Edition, which is scheduled to open in the Fall of 2013 on the 29th Street block of Collins Avenue on Miami Beach. Upper Upscale Representing the largest segment of branded hotel supply in the county (25.9%), having an accurate pulse on the development pipeline of “upper upscale” properties is critical to existing hotel operators and prospective developers alike. From 2007 to January 2012, upper upscale room supply increased by an annual average of 2.9%. Currently there are two properties spanning 647 guestrooms in the planning stage of development, one of which is a 247-room Embassy Suites which will open in Downtown Miami while the other is a 400-room hotel slated for Miami International Airport. These properties are anticipate to open in late 2013 or later and will increases the branded upper upscale hotel rooms in the county by roughly 9.8%. Upscale Hotel properties considered to be “upscale” account for 22.7% of the branded room supply in Miami-Dade County, according to data requested from Smith Travel Research. From 2007 to the start of 2012, the room supply within this tier has grown by a compounded annual average rate of 3.3%. The following figure presents the active projects and the respective stages of development for the nine hotel developments within this upscale tier that HVS is aware of. The HVS Miami office contributed to the development process for a hotel property in the Brickell area that just acquired financing, in part through the EB-5 program, and is set to break ground in the coming months.

Consumers nationwide are quickly gaining awareness for Starwood’s “aLoft” brand. As such, many developers are actively considering building hotels and flagging them with this up-and-coming, modern brand. In fact, of the nine hotel development projects within the county, three hotels (totalling 525 guestrooms) are anticipated to operate as aLoft hotels. Based on our research as well as data provided by Smith Travel Research, of the branded quality tiers, the upscale quality tier is anticipated to see the greatest increase in room supply, at 22.0%. Upper Midscale, Midscale, and Economy Properties that fit within these three quality classifications account for 34.1% of Miami-Dade County’s total branded room supply. The total inventory within these segments has essentially remained flat from 2007 to the start of 2012. Specifically, the Hampton Inn brand is gaining market share within downtown Miami/Brickell, noting the 221-room Hampton Inn that opened in Brickell in September 2011 and the fact another Hampton Inn is slated to open in “Midtown,” Miami in the late Summer of 2014. Independent It may come as a surprise to many, but hotels not affiliated with a nationally-recognized brand account for roughly 45% of all hotel rooms within Miami-Dade County. Independent hotel guestrooms within the county have increased by an average of 2.8% per year from the start of 2007 to the start of 2012. At the moment, within Miami-Dade County there are sixteen hotel development projects in various planning or construction stages; a significant portion of these hotels are to be developed in the downtown area. Miami-Dade Hotel Marketplace Outlook Macroeconomic indicators and local trends point towards a strong 2012 for Miami-Dade County hotels. County-wide occupancy and RevPAR levels are above the peak levels that were recorded in 2007 and 2008. Going forward, as confirmed by local research and market interviews, we anticipate significant growth in marketwide ADR in 2012 that will contribute to record-breaking RevPAR levels, however occupancy will likely suffer as price-sensitive room night demand is phased out of the market. The greater Miami region will see a resurgence in meeting and group business from both a volume and a revenue perspective. Due to the significant advanced booking window and the decline in groups’ propensity to travel in 2009 and 2010, the city is now poised to capture groups that had previously elected not to travel or negotiated during the downturn for very low hotel room rates. Potentially an immediate impact on the region (and one of the most prolific hotel developments in the history of South Florida), if casino licenses and Resorts World Miami are approved, Genting estimates that Miami International Airport would achieve an additional 5.4 million airline passengers (which would reportedly yield a 30% increase in airline revenues) and that the Miami-Dade County hotel industry would see a 50% gain in revenue (or about $1 billion). Its acquisition of the debt on the Omni in late 2011 would allow for the immediate fit out of a 650,000-square-foot space with a casino following the approval of the gambling bill and the granting of a license. In an interview of Scott Wadler and Max Comess of Holliday Fenoglio and Fowler, one of the most active intermediary hotel groups in Miami, commented that the greater Miami transactions market in 2012 is anticipated to be active and very competitive, with a large supply of buyers seeking properties and hotel values having recovered, and in some cases surpassed, historical peak levels. Many properties that changed hands in 2011 were due to the seller being under financial duress; without pressure to sell, prices are anticipated to continue to increase. Many submarkets are relatively protected from significant additions to supply in the immediate future given the difficulty that developers came across when sourcing financing in 2008, 2009, and 2010. In the near and mid term, we anticipate that many equity investors in the Miami-Dade market area will utilize the EB-5 program in order to (1) finance hotel development and (2) acquire green cards for South American investors. HVS Miami has worked with developers who have successfully raised money through this program and began construction on hotels that have been conditionally approved for the program. ____________________________________________  About Andy

Reed About Andy

ReedAndy Reed is an Associate in the Miami office of HVS, the premier global hospitality consulting firm since 1980. Since joining HVS, Andy has provided consulting services for a number of hotels, resorts, and mixed-use hospitality assets throughout the United States and the Caribbean. Geographically, his particular markets of interest include Miami, Orlando, the Florida Keys, and remote areas in the Caribbean. Prior to joining HVS, Andy provided a range of consulting services to the public and private tourism and economic development sectors throughout Australia, New Zealand, and portions of Asia. As a graduate of the University of Colorado, Boulder, Andy holds a Bachelors degree in Economics. About HVS HVS is the world’s leading consulting and valuation services organization focused on hotel, restaurant, shared ownership, gaming, and mixed-use real estate. Established in 1980, the company performs more than 2,000 assignments per year for virtually every major industry participant. HVS principals are regarded as the leading professionals in their respective regions of the globe. Through a worldwide network of 30 offices staffed by 400 seasoned industry professionals, HVS provides an unparalleled range of complementary services for the hospitality industry, including financing, marketing and sales solutions for shared ownership real estate. For further information on all of our services, please visit www.hvs.com. |

| Contact:

HVS Consulting

& Valuation

Services |

To Learn More About Your News Being Published on Hotel-Online Inquire Here