advertisement

MKG Hospitality States it's Urgent to Sound the Alarm When the Situation

is Going From Worse to Worst at an Accelerated Pace

|

News for the Hospitality Executive |

February 29, 2012

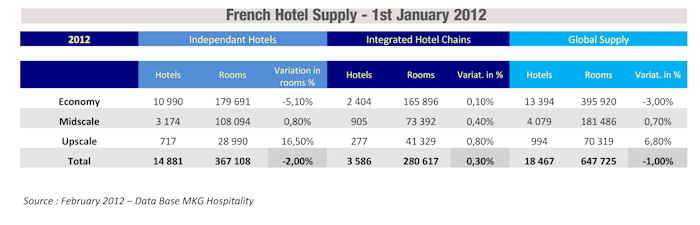

This situation is explained by to the sharp decrease of the independent hotel supply that shrank by 2% (or 7,300 fewer rooms). This happened at a time when the usual dynamism of the chain-hotel supply is slowed by difficulty of bringing a new supply out of the ground and pursuing the cleaning of certain franchise brand chains. In the end, the chain supply grew by fewer than 1,000 rooms in all. The economic crisis, the cost of marketing, and consumer expectations have undermined the profitability of a growing number of economy hotels that are paying the high price with a net drain of 634 hotels and 12,300 rooms – a record loss. However, the slump in the independent hotel sector does not condemn all operations. The same inventory also shows that growth in the independent supply is very significant in the three, four, and, five-star categories, which together experienced net growth of more than 5,000 rooms. This movement is the continuation of the decade-long trend that marks the return of independent hoteliers to there are of expertise: full service hotels in city centers. Moreover, hotel groups have decided to place franchising amongst their developmental priorities. Due to internal movements between chains, the growing power of franchisees in the supplies of corporate chains is not visible in the figures representing global growth. Growth, even marginal, for chain hotels on a shrinking global market allows them to cross another threshold of market share. Today, more than 43% of the global supply operates under a hotel brand, and certainly more than 50% if we add the main consortia, which require the flying of their banner. The analysis of the global lodging supply in France is pertinent only to classified hotels. However is they are not the only ones to address a commercial clientele. Parallel types of accommodations are increasingly poaching on these markets. Tax incentives remain strong for stimulating investments in new tourism residences and especially urban residences which have the advantage of being less seasonal. Despite the succession of high profile failures of operators such as Mona Lisa, Maison de Biarritz and Residhotel, real estate promotion is doing well: Adagio by Pierre&Vacances/Accor, Citadines, Appart’City, Park&Suites, Odalys City, Cerise by Exhore and Hipark are all multiplying their openings. While the tension with hoteliers may have subsided, it is clear that the residence-hotel model is absorbing a significant share of developers’ resources as they focus less on the hotel industry. “It is urgent to sound the alarm when the situation is going from worse to worst at an accelerated pace”, comments Georges Panayotis, President & CEO of MKG Group. “One should not be sorry about the restructuring of the French hotel supply that is taking place. However, one should be sorry about the measures taken in the past to protect independent hotels against the so-called ‘invasion’ of hotel chains have only slowed down the conversion of hotels that cannot bear the new economic situation, without preparing for the future. It is urgent to create a newly-built hotel supply, financed by independent or institutional investors. One might be used to thinking that it is impossible to relocate jobs in tourism, but in the end, the result is the same if the clientele opts for other destinations, due to lack of available rooms, as it is already the case in Paris during large MICE events.” Established in 1985 by Georges Panayotis, MKG Group has built a solid reputation for business expertise and substantial European-based know-how in the fields of tourism, lodging and food service. MKG Group meets the needs of each of its clients by providing valuable analytical and decision-making skills necessary for success. www.mkg-group.com |

| For further information , please contact : MKG Group - International Development Department Vanguelis Panayotis T. : +33 (0)1 56 56 87 87 [email protected] MKG Hospitality - Media Contact Michael Komodromou Tel: +44 (0)20 7624 4030 [email protected] Web: www.mkg-hospitality.com

|