advertisement

Room Rates Continue To Lag

|

News for the Hospitality Executive |

advertisement

|

July 6, 2011, Atlanta, GA – The

recovery of the U.S. lodging industry continues in a

pattern established in the first quarter of 2010, with occupancy gains

still

outpacing gains in room rate. According to the June 2011 edition

of Hotel

Horizons®,

PKF Hospitality Research (PKF-HR) forecasts that the demand for U.S.

hotel

rooms in 2011 will increase a solid 4.9 percent, while the average

daily room

rate (ADR)

paid by guests will rise a modest 2.4 percent.

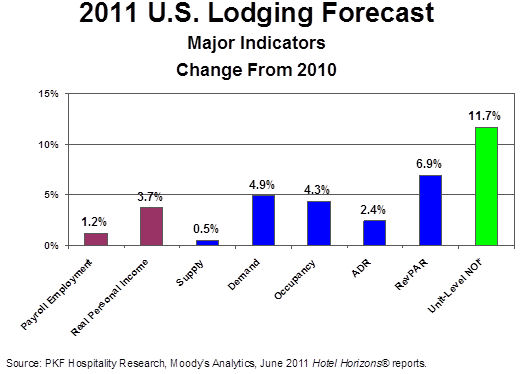

“We continue to be impressed by the pace at which travelers have returned to the road after the depths of the Great Recession,” said R. Mark Woodworth, president of PKF-HR. “Given the headwinds created by stagnant employment and continued weakness in the housing sector of the economy, it is somewhat surprising that hotel demand continues to bounce back as quickly as it has.” The 4.9 percent rise in occupied rooms forecast for 2011 compares to the 7.6 percent increase in lodging demand for 2010 reported by Smith Travel Research (STR). Both growth rates are well above the STR long-term average annual demand growth rate of 1.5 percent. “Offsetting the surge in demand, however, has been relatively sluggish increases in room rates. And, as hotel owners and operators know, it is ADR growth that powers profits,” Woodworth noted. “Given the sustained robust increases in demand, combined with limited new competition, one would expect that hoteliers should be able to start raising room rates more aggressively. However, market conditions are still very competitive and, with few exceptions, scarcity has yet to be a concern for most lodging consumers. We are forecasting that only 12 of the largest lodging markets in the U.S. will achieve an occupancy in 2011 that is greater than their long-run average. It won’t be until 2013 that we see the majority of the 50 markets in our Hotel Horizons® universe exceed their long-run occupancy rate.” Accordingly, PKF-HR is forecasting that U.S. room rates beyond 2011 will grow at a greater pace: 5.5 percent in 2012 and another 5.8 percent in 2013.  Unemployment Hurts The PKF-HR Hotel Horizons® econometric forecasts are driven by the economic projections produced by Moody’s Analytics (Moody’s). Therefore, it is important to understand the underlying economic variables that are steering the direction and magnitude of the PKF-HR lodging forecasts. “Since January of 2011 Moody’s outlook for the U.S. economy has continued to sour,” said John B. (Jack) Corgel Ph.D., the Robert C. Baker Professor of Real Estate at the Cornell University School of Hotel Administration and senior advisor to PKF-HR. “Moody’s has steadily lowered their 2011 forecasts for employment, income, and GDP growth since the beginning of the year. The only economic variable on the rise is inflation due mostly to the increases in the price of gasoline.” “To reflect Moody’s fading optimism about the economy in 2011, we have in kind adjusted our lodging forecasts. Compared to our thinking back in March of this year, our expectations for lodging demand growth have improved, but our projections of rate growth have diminished,” Corgel said. “Overall, the magnitude of our revenue forecasts have not changed materially, but the composition of the RevPAR growth drivers has. Occupancy gains will dominate the lift in RevPAR more than originally anticipated. After all, many local markets still have not reached long-run average occupancies – the point when rate growth accelerates.” For 2011, PKF-HR is forecasting a 4.3 percent increase in occupancy to accompany the 2.4 percent rise in ADR. The net result is a 6.9 percent projection of RevPAR growth in 2011, slightly less than the 7.1 percent rate forecast by PKF-HR back in March of 2011. PKF-HR’s forecast for RevPAR improvement in 2012 has been altered downward as well, from 8.9 percent in March to its current thinking of 8.7 percent. Unemployment Helps News of persistent high levels of unemployment is certainly discouraging, but this negative economic condition has had a positive impact on hotel profitability. The continued high rate of unemployment, and the resulting lack of pressure on salaries and wages, has helped to stem the rise in labor costs at U.S. hotels. Typically during the early stages of the recovery cycle, hotels incur a significant increase in the variable costs associated with the rise in the number of occupied rooms. First and foremost among the rising expenses are labor costs, which account for 46.6 percent of every dollar spent to operate a hotel in the U.S. “Unlike previous industry recoveries, this time around we have observed labor related expenses declining on a dollar-per-occupied room basis. This implies labor cost containment, combined with an increase in employee productivity,” Woodworth observed. “By controlling labor costs, hotel managers can offset the inefficient hotel revenue growth and achieve gains on the bottom-line.” PKF-HR is projecting unit-level net operating income to increase 11.7 percent in 2011. Profit growth will be even greater in 2012 (17.9 percent) as room rates begin to drive RevPAR. Improvement Spreads The early stages of this lodging recovery were dominated by the upper-tier properties. According to STR, RevPAR growth was by far greatest among luxury hotels in 2010. Looking towards 2011 and beyond, the recovery is projected to spread across the entire spectrum of the lodging industry. The June 2011 editions of Hotel Horizons® incorporate the new STR chain-scales. For 2011, PKF-HR is forecasting luxury hotels to continue to enjoy the strongest growth in RevPAR (10.0 percent), followed closely by properties in the upscale (9.4 percent) segment. RevPAR growth for all remaining chain-scale categories is forecast to fall in the range of 4.3 percent to 5.7 percent. “Our forecast of a 2.4 percent increase in the supply of upscale hotel rooms in 2011 reflects the popularity of select-service, boutique, and extended-stay hotels among developers,” Woodworth noted. “Concurrently, our 7.8 percent increase in demand forecast for this same segment is indicative of the popularity of these property types among consumers.” For 2012, the top three chain-scales (luxury, upper-upscale, upscale) are all forecast to achieve RevPAR gains in excess of 10 percent. Upper-midscale RevPAR is projected to increase by 8.7 percent, while midscale and economy properties should both enjoy a 6.6 percent boost in revenue. “Our June forecasts show the length of the recovery for the U.S. lodging industry has been extended a bit, but we are definitely on an upward trajectory. Travelers are returning to the road despite the slowing economy, new supply is not an obstacle, and hotel managers are effectively controlling their costs. These are important ingredients for a solid recovery,” Corgel concluded. To purchase a June 2011 Hotel Horizon® report, please visit www.hotelhorizons.com. Reports are available for each of 50 major metropolitan areas in the U.S., and contain five year projections of supply, demand, occupancy, ADR, and RevPAR. About PKF CONSULTING USA Headquartered in San Francisco, PKF Consulting USA (www.pkfc.com) is an advisory and real estate firm specializing in the hospitality industry. PKF Consulting USA is owned by FirstService Corporation and is a subsidiary of Colliers International. The firm operates two companies: PKF Consulting USA and PKF Hospitality Research. The firm has offices in New York, Boston, Portland, Indianapolis, Chicago, Philadelphia, Washington DC, Atlanta, Asheville, Jacksonville, Orlando, Tampa, Houston, Dallas, Los Angeles, Bozeman, and San Francisco. PKF Consulting USA offers hotel appraisal and hotel valuation services, hotel market studies, hospitality litigation support, and hotel advisory services. PKF Hospitality Research produces Hotel Horizons®, an econometrically based hotel forecast, BenchmarkerSM, a customized comparative hotel benchmark report, and Annual Trends® in the Hotel Industry, a historical hotel financial publication featuring rich hotel statistics, as well as hotel research services. |

| Contact: Mark Woodworth President PKF Hospitality Research 3475 Lenox Road, Suite 720 Atlanta, GA 30326 20170 (404) 842-1150, ext 222 Email: [email protected] or Chris Daly Daly Gray Public Relations Tel: 703 435 6293 Email: [email protected] www.dalygray.com

|