advertisement

U.S. Transaction

Prices Continue To Accelerate As Cap Rates

Are At Pre-Recession Lows During Q1 2011

Average Selling Price at Record High of

$125,946 Per Room,

a 30% YoY Increase

from Q1 2010’s $97,084 per room

|

News for the Hospitality Executive |

advertisement

U.S. Transaction

Prices Continue To Accelerate As Cap Rates

Are At Pre-Recession Lows During Q1 2011

Average Selling Price at Record High of

$125,946 Per Room,

a 30% YoY Increase

from Q1 2010’s $97,084 per room

|

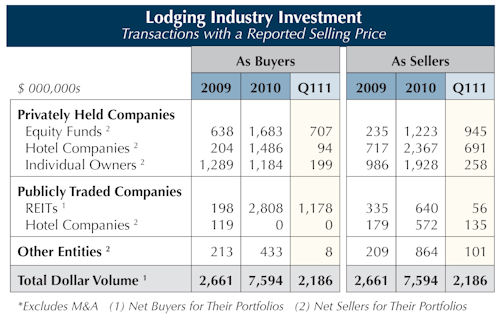

47% of the 110 transactions were in the top 25 markets, the highest percentage LE has ever recorded. 37% were in Upscale and higher chain scales. 21 hotels greater than 200 rooms, or 19% of the total, sold at a cyclical high average of $181,680 per room. For the 110 hotels that reported a selling price, a total of $2,186M was invested in the industry. REITs accounted for 54% of that total or $1,178M, while Privately Held Equity Funds were next at $707M. Together, they accounted for a whopping 86% of the total $2,186M invested. Equity Funds were the biggest sellers, followed by Privately Held Hotel Companies, with a combined $1,636M or 75% of the total.  Competition in the top markets for large luxury and upscale

hotels, both full and select service, is fierce. For institutional

investors,

the cost of debt is at a record low. REITs, in particular, have

comparatively

low yield requirements. Coupled with their ability to pay up front for

some

future performance, REITs have quickly pushed cap rates to

pre-recession lows. Competition in the top markets for large luxury and upscale

hotels, both full and select service, is fierce. For institutional

investors,

the cost of debt is at a record low. REITs, in particular, have

comparatively

low yield requirements. Coupled with their ability to pay up front for

some

future performance, REITs have quickly pushed cap rates to

pre-recession lows.However, overall selling prices continue to be unnaturally inflated due to an abnormally small number of sales in the lower chain scales where operations have not as yet recovered sufficiently to be a driver of valuations and where Main Street financing is still restrained. IT’S AN OPPORTUNE TIME TO BE A BUYER - To date, the current lift in valuations can largely be attributed to lower cap rates derived from record low interest rates on debt and lower equity yield requirements. Nonetheless, from a buyer’s perspective, we are at that singular time in every lodging cycle where attractively priced hotels with little downside risk are generally available, but where most of the lodging recovery and operating upside has yet to be realized. Making investments like this at the beginning of a new cycle is precisely the formula for the traditional 5-7 year institutional holding period. Paradoxically, for current ownership groups, it can also be a great time to be a seller of larger, well-located hotels in the top markets, if their financial and/or lending situation permits. Chances are their hotel is only in the beginning stages of recovery and requires reinvestment dollars for renovation and/or market repositioning, which often necessitates a refinancing event that can be difficult to consummate. A sale today in a rather fluid market replete with qualified buyers is often the best strategy to sidestep complex ownership issues. For some owners, it can amount to a once-in-a-cycle opportunity that cannot be missed. There is another reason why owners of larger, well-located properties might consider selling. If they continue to hold their assets, the hoped for future valuation lift, derived from improvements in operating performance, might be somewhat mitigated by higher cap rates caused by rising lending rates and equity yield requirements, as market conditions are expected to change further downstream. This could be particularly true for REITs, as shareholders will likely make demands to increase dividends in the future. Notable Transactions & Property Transfers

|

| Contact: Lodging Econometrics |