advertisement

Europe, Middle East and Africa Pipeline Growth Muted As Developers

Await Further Economic, Operational & Financing Improvements

|

News for the Hospitality Executive |

advertisement

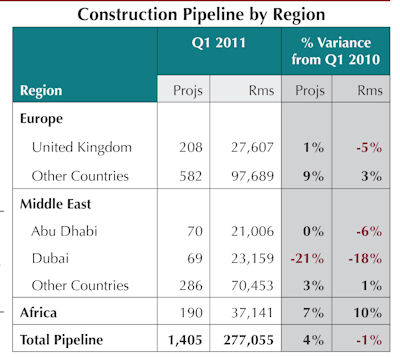

June 17, 2011 - Europe’s Construction Pipeline is at

790 projects/125,296

rooms at the end of Q1. The United Kingdom has the largest country

Pipeline in

Europe, with 26% of its total projects. At 208 projects/27,607, the UK

Pipeline

has grown 1% by projects, but decreased 5% by rooms year-over-year

(YoY). All

other European countries combined have seen a 9% increase in projects

and 3%

increase by rooms YoY. June 17, 2011 - Europe’s Construction Pipeline is at

790 projects/125,296

rooms at the end of Q1. The United Kingdom has the largest country

Pipeline in

Europe, with 26% of its total projects. At 208 projects/27,607, the UK

Pipeline

has grown 1% by projects, but decreased 5% by rooms year-over-year

(YoY). All

other European countries combined have seen a 9% increase in projects

and 3%

increase by rooms YoY.

The rapid recessionary declines in Europe’s Construction Pipeline have abated. The Pipeline is in a lower bottoming channel for a fifth consecutive quarter and will likely remain there until the sovereign debt crisis eases, national economies show a more vigorous recovery, improvement in hotel operations accelerates, and construction financing becomes more available. In the meantime, over half of Total Pipeline projects and rooms are now Under Construction, with many set to exit the Pipeline as New Supply during the next two years. This will continue to draw down Total Pipeline counts, as difficulties in securing construction financing will keep New Project Announcements at low levels. The Total Pipeline for the Middle East, at 425 projects/114,618 rooms in Q1, is down 2% by projects and 5% by rooms from Q1 2010. The region’s two largest Pipelines, Dubai and Abu Dhabi, have an extremely high 68% and 65% of projects Under Construction. Many of Dubai’s projects have had construction delays due to financing difficulties and downsized construction crews and, as such, are not moving aggressively toward completion. As a result, the openings for these projects are now spread out over the next 2-3 years. Combined with continued low New Project Announcements, this will rapidly deplete the Pipelines in these Emirates, which will enter a lengthy period of guest room absorption. Pipelines in other Middle East countries have also bottomed and might trend downward further due to growing political and civil unrest. Africa’s Total Pipeline of 190 projects/37,141 rooms has been trending upward incrementally for three consecutive quarters and is up 7% by projects and 10% by rooms from Q1 2010. Morocco (64 projects/11,955 rooms), Nigeria (19 projects/3,937 rooms) and South Africa (17 projects/2,492 rooms) account for 53% of the region’s total projects and 50% of rooms. The recent escalations in political and civil unrest in Libya, Tunisia, Egypt, and recently in Morocco could dampen development activity in Northern Africa in the future.  EUROPEAN DEVELOPMENT EUROPEAN DEVELOPMENT

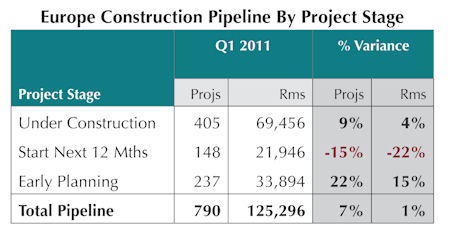

With 790 projects/125,296 rooms, Europe’s Total Pipeline is up 7% and 1%, respectively, from the same period last year. The disparity between year-over-year project and room count growth shows that the size of new projects entering the Pipeline is getting smaller. In Q1 2011, the average Pipeline project size was 158 rooms, a ten-room decrease from the average in Q1 2010. Developer preference is for smaller-sized properties with upscale and midmarket brands, for which financing can be more easily acquired. 71% of Europe’s Total Pipeline projects are in these chain scale segments, while 77% of all projects are less than 200 rooms. 405 projects/69,456 rooms are currently Under Construction, an increase of 9% by projects and 4% by rooms year-over-year. 85% of these projects are set to open during the remainder of 2011 and through 2012 and will empty the Pipeline substantially. Since peaking in 2008, New Hotel Openings have declined incrementally. LE’s Forecast for New Hotel Openings expects 204 new hotels/29,588 rooms to open in 2011, with a slight uptick in 2012, when 194 hotels/31,762 rooms are anticipated to exit the Pipeline as New Supply. New Hotel Openings are then expected to trend downward through mid-decade. Similar to the trends seen in other developed regions and countries of the world, Scheduled Starts in the Next 12 Months, at 148 projects/21,946 rooms, are at a four-year low and down 15% by projects and 22% by rooms from Q1 2010. Counts in Early Planning, at 237 projects/33,894 rooms, have risen 22% by projects and 15% by rooms YoY as this is where New Project Announcements (NPAs) have been entering the Pipeline, but are not quickly moving forward toward construction as developers wait for improved economic and financing conditions. NOTABLE PIPELINE DEVELOPMENTS

|

| Contact: Lodging Econometrics |