advertisement

Lodging Econometrics Reports 2012 Forecast for New Openings for EMEA

Pipeline Totals Continue to Fall, with Further Declines Expected as European Economies Soften

and Political Turmoil Intensifies in the Middle East

|

News for the Hospitality Executive |

advertisement

March 7, 2011 - The sovereign debt

crisis, budget cutbacks and rising inflation continue to weigh heavily

on much

of Europe and will keep economic growth subdued at least into 2012.

Uncertainty

is particularly high in Ireland, Spain, Portugal, and Italy. In the

United

Kingdom, an unexpected drop in GDP to -0.6% in Q4 2010 has triggered

apprehensions

about a double-dip recession. Fears of increased energy and commodity

prices in

the wake of the recent turmoil in the Middle East and Northern Africa

are

impacting as well. Overall economic insecurity, combined with

lackluster

lodging operations, will continue to dampen developer sentiment. March 7, 2011 - The sovereign debt

crisis, budget cutbacks and rising inflation continue to weigh heavily

on much

of Europe and will keep economic growth subdued at least into 2012.

Uncertainty

is particularly high in Ireland, Spain, Portugal, and Italy. In the

United

Kingdom, an unexpected drop in GDP to -0.6% in Q4 2010 has triggered

apprehensions

about a double-dip recession. Fears of increased energy and commodity

prices in

the wake of the recent turmoil in the Middle East and Northern Africa

are

impacting as well. Overall economic insecurity, combined with

lackluster

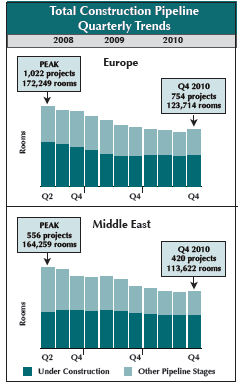

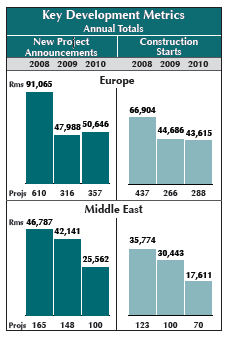

lodging operations, will continue to dampen developer sentiment.Europe’s Total Construction Pipeline, at 754 projects/123,714 rooms at the end of Q4, has been in a bottoming formation for seven consecutive quarters. New Project Announcements (NPAs) into the Pipeline remain in a low channel at 117 projects/14,058 rooms, and Construction Starts for projects already in the Pipeline, at 75 projects/9,492 rooms, are at their second lowest level reported in three years. As more budgetary reductions are enacted, construction financing still difficult to obtain and just modest improvements in lodging operations anticipated, these development metrics should decline further into 2012. Along with its own sovereign debt, investment and banking issues, the Middle East and Northern Africa are now contending with explosive political unrest in many countries. This does not bode well for future development in the region, where Pipeline counts have already been in decline for 10 straight quarters. At the end of Q4, the Total Middle East Pipeline stood at 420 projects/113,622 rooms, the lowest LE has recorded in three years. The flow of NPAs into the Pipeline is still sluggish, with just 28 projects/8,897 rooms announced in Q4. Constructions Starts are at a three-year low, with only 18 projects/4,333 rooms getting underway in the quarter. With the recent upheavals, travel to the region is expected to decrease sharply, negatively impacting lodging demand and profitability. Absorbing new supply that previously came online will become even more difficult, especially as New Hotel Openings rise through 2012. LE expects a serious slowdown in new hotel development, with NPAs and Construction Starts for projects already in the Pipeline falling to new lows. Cancellations and Postponements are likely to increase.  EUROPE DEVELOPMENT Europe’s Total Pipeline, at 754 projects in Q4, remains in a low plateau, holding flat for a fifth consecutive quarter. With over half of all projects and rooms currently Under Construction, LE expects the Pipeline to empty substantially through 2012. LE’s Forecast for New Hotel Openings projects 191 new hotels/28,946 rooms to open in 2011, and then an additional 185 hotels/30,731 rooms in 2012. Developer sentiment remains muted for the second year in a row. Total New Projects Announcements (NPAs) into the Pipeline in 2010 are down 41% by projects and 44% by rooms from the high in 2008, only showing a slight increase over 2009. NPAs are likely to decline further and will not be adequate to refresh Pipeline totals any time soon. Construction Starts for projects already in the Pipeline are also down from 2008, -34% by projects and -35% by rooms, and will remain in a low channel until the economy and lodging operations recover more substantially. MIDDLE EAST DEVELOPMENT Total Pipeline counts in the Middle East trended down further from the Q2 2008 peak to reach a new three-year low of 420 projects in Q4 2010. With rampant civil unrest in many countries, inbound travel is poised to drop precipitously, further dampening lodging demand and hindering the absorption of the wave of new hotels that opened in 2009. After declining in 2010, New Hotel Openings will bounce back again in 2011, when LE’s Forecast projects 85 hotels/20,975 rooms to come online, and then reach a new high for the cycle with 101 hotels/27,523 rooms in 2012. Key development metrics show a more substantial decline in 2010 compared to 2009. NPAs into the Pipeline are down 32% by projects and 39% by rooms year-over-year (YOY). Construction Starts also declined considerably, down 30% by projects and 42% by rooms. The larger YOY drop in room count for Construction Starts is notable, as the average size for projects starting construction is falling from 304 rooms in 2009 to 252 rooms in 2010. The age of the large, luxurious, “starchitect” designed project appears to be winding down slowly. |

| Contact: Lodging Econometrics |