|

News for the Hospitality Executive |

![]() .

.

|

Introduction Clearview Hotel Trust intends to sell stock in an initial public offering (IPO) to fund the acquisition of 14 hotels from Columbia Sussex, who would stay on as the hotels’ operator. Investors, it’s time to meet your business partner. Columbia Sussex, a Fort Mitchell, KY based company headed by owner William Yung, III, grew during the boom years to become 4th largest owner of full service hotels in the country with 67 hotels. Credit was easy, and Columbia Sussex borrowed lots. Now, the cost to rapid expansion is becoming clearer, as Columbia Sussex does something it has rarely done before – seek a partner. Columbia Sussex needs Clearview to buy its 14 hotels so it can repay a $215 million loan that matures in July and is guaranteed by Columbia Sussex. While Clearview’s IPO and concurrent acquisition will solve one imminent debt maturity, it does not address the rest of Columbia Sussex’s pending debt problems, not all of which were disclosed by Clearview in its initial SEC filing. But does Clearview need Columbia Sussex? The core questions potential investors must examine before buying this IPO are:

Can

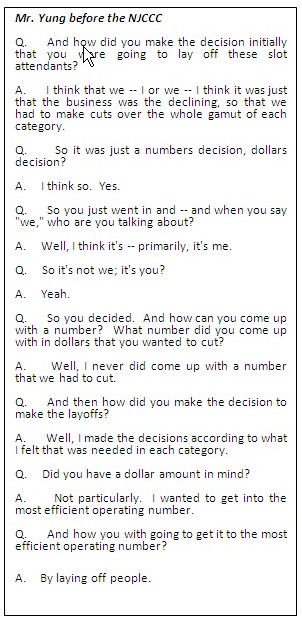

Mr. Yung Work for Clearview? Mr. Yung’s record in the gaming industry provides the best evidence to question Mr. Yung’s ability to work for Clearview and its investors. Uncooperative in Atlantic City In 2006, Mr. Yung acquired the Tropicana Casino and Resort in Atlantic City as part of a $2.8 billion purchase of Aztar Corp., and by the end of 2007, he lost the Atlantic City Tropicana as state regulators denied his license renewal and imposed a $750,000 fine. The New Jersey Casino Control Commission (NJCCC) gave a number of reasons for denying Tropicana’s license. Soon after taking over control of the property, Yung laid-off nearly 1,000 employees – approximately one-quarter of the workforce. This was one of the factors in the Commission denying the Tropicana’s license. The NJCCC’s

Chairwoman Linda

Kassekert said in her motion to deny the license: "Staffing

was slashed in pursuit of profit. Cleanliness was disregarded in order

to meet

a predetermined bottom line. Customer service was dismissed.”

… "Simply

put, I do not believe this applicant has the business ability to

operate a

facility of this size and magnitude given the decisions that were

made." [1]

Mr. Yung’s approach to reducing costs was noted by the Commission: “Calculus is a marvelous discipline: you start with the answer, and work backwards. In certain respects, that was Yung's approach in dealing with the Tropicana. He needed to get a certain answer, and it mattered little whether there was a cogent analysis to justify the outcome." [2] Chairwoman Kassekert remarked on Mr. Yung’s failure to notify the Commission on Tropicana’s layoffs: “Simply put, Yung exhibited a lack of cooperation on a grand scale that did nothing to earn regulatory trust in his ability to operate in this marketplace. Moreover, his decision-making process was seriously flawed.”

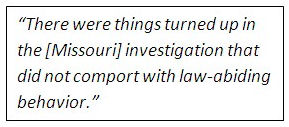

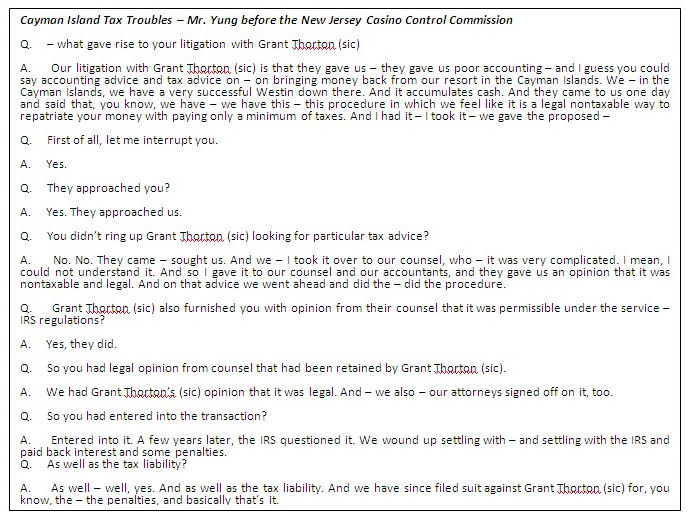

In addition, Kassekert remarked on the inconsistencies of the testimonies of Mr. Yung and other Tropicana employees during the licensing hearing: “Most unfortunately, there is evidence of outright perjury in the record and evidence of a more subtle kind in its elusiveness. This can only lead me to the conclusion that this applicant has failed to meet the requirements of the [Casino Control] Act for honesty, integrity and good character.” Tropicana Bankruptcy “Following the license denial, two subsidiaries of Wimar Tahoe Corporation, Tropicana Entertainment, LLC and Tropicana Las Vegas Holdings, LLC, and certain of their respective subsidiaries, which we collectively refer to as the Tropicana Entities, defaulted on their $1.3 billion credit agreement. Thereafter, on May 5, 2008, the Tropicana Entities filed voluntary petitions for reorganization relief under Chapter 11 of the Bankruptcy Code in the United States Bankruptcy Court for the District of Delaware.” “On May 5, 2009, the United States Bankruptcy Court for the District of Delaware approved the First Amended Joint Plan of Reorganization, which, among other matters, authorized the creation of a litigation trust, which we refer to as the Tropicana Litigation Trust, for purposes of pursuing any claims against Mr. Yung, Columbia Sussex Corporation and Wimar Tahoe Corporation and certain of their affiliates. On February 17, 2010, Lightsway Litigation Services, LLC, as trustee of the Tropicana Litigation Trust, filed a complaint against Mr. Yung, Wimar Tahoe Corporation, Columbia Sussex Corporation and certain of their affiliates in the United States Bankruptcy Court for the District of Delaware." [3]The allegations in the complaint can be found in the Clearview S-11. Misfortune in Missouri In 2005, Yung attempted to buy a St. Louis casino out of bankruptcy. After Missouri’s background check, he withdrew. “‘There were things turned up in the [Missouri] investigation that did not comport with law-abiding behavior,’ gaming commission director Gene McNary told the Kansas City Star in December. ‘We gave them a chance to withdraw, and they did.’" [4] “On January 12,

2006, PCI [President

Casinos, Inc.] filed an adversary action in the Bankruptcy Court for

the

Eastern District of Missouri, alleging three causes of action: (1)

breach of contract

based on Columbia Sussex’s failure to purchase the President Casino;

(2) prima

facie tort claim based on Columbia Sussex's raising of the validated

parking rates

for the Cherrick Lot; and (3) injunctive relief pursuant to 11 U.S.C.

§ 105, enjoining

Columbia Sussex from blocking access to the Cherrick Lot by casino

patrons and

from raising the validation parking fee over $1.50. On January 25,

2006, the

Bankruptcy Court entered a temporary restraining order granting the

requested

injunctive relief to PCI." [5] “On January 12,

2006, PCI [President

Casinos, Inc.] filed an adversary action in the Bankruptcy Court for

the

Eastern District of Missouri, alleging three causes of action: (1)

breach of contract

based on Columbia Sussex’s failure to purchase the President Casino;

(2) prima

facie tort claim based on Columbia Sussex's raising of the validated

parking rates

for the Cherrick Lot; and (3) injunctive relief pursuant to 11 U.S.C.

§ 105, enjoining

Columbia Sussex from blocking access to the Cherrick Lot by casino

patrons and

from raising the validation parking fee over $1.50. On January 25,

2006, the

Bankruptcy Court entered a temporary restraining order granting the

requested

injunctive relief to PCI." [5]US District Court Judge Henry Edward Autrey (Eastern District of Missouri) wrote in his September 25, 2009 order: “…William Yung told John Aylsworth that if President Casino did not drop the breach of contract suit ‘he would just take that parking lot away and chain it up.’ When asked about these remarks, Yung explained that he wanted to retaliate against PCI for what he perceived were threats to bring a breach of contract suit. Then, on the heels of these remarks, Columbia Sussex, with just eight hours notice to the President Casino, without any research into appropriate market rates for validated parking, raised rates 300 percent, from $1.50 to $6.00." [6] Judge Autrey affirmed a bankruptcy court’s judgment on the parking dispute which ordered Columbia Sussex to pay $382,884 to the casino, however he “reversed the bankruptcy judge's decision on the breach of contract claim and awarded $42.3 million to President Casinos, which includes damages and prejudgment interest." [7] In October 2009, Columbia Sussex made a motion for rehearing. Unwanted in Indiana “In March 2007, Evansville Mayor Jonathan Weinzapfel learned Columbia Sussex was laying off about 70 casino workers, a number higher than first discussed, and asked the gaming commission to see if the company was thus violating state standards. “The commission opened an investigation only to suspend it when New Jersey decided to revoke Columbia Sussex’s license to operate the Tropicana casino in Atlantic City. New Jersey officials said the Tropicana had failed to meet state standards on cleanliness and service. Columbia Sussex, facing a bankruptcy, decided to sell Casino Aztar, Tropicana and a casino in Vicksburg, Miss.: [9] “‘My ambition for Evansville was to build a boat in a moat there,’ Yung said. ‘Then I went and met the mayor, He was concerned no one [from Columbia Sussex] came to see him; no one bent to the altar,’ Yung said. “Yung said Columbia’s relationship with the city got off to a rocky start at the meeting because the mayor’s first question regarded the company’s record with the Equal Employment Opportunity Commission complaints. “‘I didn’t come asking for anything; I came because he wanted me there,’ Yung said. ‘Obviously, I wasn’t welcomed.’ “Weinzapfel said he did not recall starting the conversation with a question of EEOC claims, but the mayor said he did ask about the issue because the city’s research into Columbia Sussex turned up an ‘inordinate’ amount of EEOC complaints. “Yung said he came away from the meeting ‘disheartened,’ adding that several factors must be in place in order for communities to attract investment. “‘One of them is, you want to be wanted,’ Yung said. ‘Clearly I wasn’t wanted.’" [10] Park Cattle Lease Lawsuit Disclosures in Tropicana Entertainment’s SEC filings describe a dispute over maintenance of Tahoe Horizon Hotel and Casino, which was subject to land leases with a third party called Park Cattle Company. “In October

2005, Tropicana Casinos and Resorts, Tropicana Entertainment’s ultimate

parent, received a default notice from Park Cattle, the landlord for

the two ground leases for our Tahoe Horizon property, On April 2, 2008, the parties to the lawsuit reached settlement, described in Tropicana Entertainment’s SEC filing. “On April 2, 2008, Tropicana Entertainment, LLC (“Tropicana Entertainment”), Tahoe Horizon, LLC (“Tahoe Horizon”), Columbia Properties Tahoe, LLC (“CP Tahoe”) and certain of their affiliates (the “Unrestricted Affiliates;” and together with Tropicana Entertainment, Tahoe Horizon and CP Tahoe, the “Tropicana Parties”) entered into a Stipulation for Entry of Judgment (the “Settlement Stipulation”) with Park Cattle Co. (“Park Cattle”) pursuant to which the parties agreed to settle their ongoing litigation that had been pending in a Nevada state court with respect to the ground lease for Tropicana Entertainment’s Lake Tahoe Horizon Casino and Resort (the “Horizon Resort”) in South Lake Tahoe, Nevada. Under the terms of the Settlement Stipulation, the Unrestricted Affiliates agreed to make cash payments totaling $165 million (the “Settlement Payments”) to Park Cattle over the next three years, the first of which was made on April 2, 2008 in the amount of $40 million.”[12]Furthermore, as reported by Tropicana Entertainment, “[T]he proposed Horizon Resort lease amendment provides, among other things, that the ground lease will terminate on March 31, 2011.” That would be 29 years before its expiration. According to the Las Vegas Sun: “The Horizon also had been fined by the Environmental Protection Agency for mishandling of asbestos in the building and cited by OSHA for violations of the electrical code.”[13] RevPAR at Columbia Sussex Hotels Columbia Sussex is known for a particular operating style focused on cutting costs. Because there are costs associated with occupancy gains, Columbia Sussex’s emphasis on cost reductions may limit RevPAR growth from increased occupancy, even in the good years. Potential Clearview investors may want to examine what happened at a distinct portfolio of 14 hotels after their acquisition by Columbia Sussex in the last upcycle. Columbia Sussex bought 14 hotels for a total $1.4 billion from Wyndham on October 6, 2005, borrowing $1.1 billion in CMBS and mezzanine debt. The prospectus for the CMBS – called Bear Stearns Commercial Mortgage Securities 2006-BBA7 – details the performance of the hotels at that time. According to the Offering Circular, the 14 Columbia Sussex hotels had an average RevPAR of $99.60, with occupancy of 76% and an average daily room rate (ADR) of $131, for the twelve months ending March 31, 2006.[14] For the year end 2007, according to Fitch Ratings, the portfolio’s average RevPAR was $99.40, essentially flat when compared to the March 31, 2006 period. 2007 occupancy for the portfolio declined to 62.5% with an increased ADR of $158.90.[15] Additionally, "Fitch stressed YE2007 net cash flow (NCF) also declined 6% compared to issuance NCF.”[16] By September 2008, year-to-date occupancy was 65%, ADR $163, and RevPAR was $105.58, according to Fitch. These 14 Columbia Sussex hotels missed the solid RevPAR growth during the boom years of the last upcycle. By contrast, average annual RevPAR for U.S. hotels overall increased 7.5% in 2006 and another 5.7% in 2007, according to Smith Travel Research.

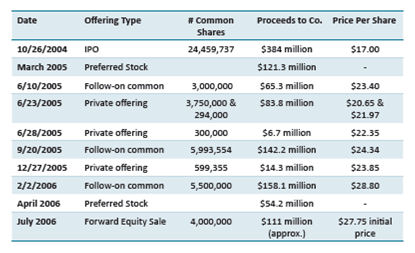

Performance of 14 Other Columbia

Sussex Hotels During Last Up Cycle

Clearview stated in its original S11: “Certain of the hotel properties in our initial portfolio have lower occupancy rates, which we believe provides opportunities for improvement through, among other measures, selectively enhancing group sales teams at certain of our properties.”[17] Prospective investors should consider whether Clearview will succeed in changing Columbia Sussex’s management style given the record laid out on previous pages. Likewise, investors should ask Clearview management what their analysis is of maintenance and capital expenditures that may have been deferred under Columbia Sussex’s ownership. Mr. Jon Kline’s Record Clearview Hotel Trust touts Mr. Kline’s record at Sunstone Hotel Investors as evidence of a “Proven Track Record”. [18]“Our Chairman and Chief

Executive Officer, Jon D. Kline, previously served as Chief Financial

Officer from 2004 to 2006 and President from 2006 to 2007 of Sunstone

Hotel Investors, or Sunstone, a publicly-listed hotel REIT. Mr. Kline

played a significant role in transitioning Sunstone from a private

hotel owner and operator financed by Westbrook Partners, a real estate

private equity fund, to a publicly-listed company. Sunstone completed

more than $2.0 billion in acquisitions during Mr. Kline’s tenure.”

Mr. Kline

resigned from his

position as President of Sunstone effective June 30, 2007, following

the

appointment of Steve Goldman as Chief Executive Officer in March 2007.

Sunstone has walked away from, put into receivership or intends to deed back to lenders 11 hotels, with 2,838 rooms. Sunstone still has $1.2 billion of debt, excluding the debt associated with those 11 hotels. Despite the number of equity offerings it undertook during the acquisition period, Sunstone shareholders have faced a 65% increase in the number of outstanding shares since mid-2007 (Mr. Kline’s departure), as the company completed two more follow-on share offerings in 2009 in the bottom of the cycle. Sunstone’s current share price remains well below its 2004 IPO price. Start-up REITS DraggingSince December 2009, three other REITS have undertaken IPOs to raise capital for hotel acquisitions: Pebblebrook Hotel Trust, Chesapeake Lodging Trust, and Chatham Lodging Trust. All three are trading below their IPO prices, and are underperforming in comparison to the leading hotel REIT, Host Hotels, for the period since their IPOs, through June 16, 2010.  Columbia Sussex’s Growing Labor Disputes Labor disputes at Columbia Sussex’s properties have grown over the last few years, with the number of boycotts growing from one in 2007 to 8 as of today. Facing a variety of cuts, including layoffs, benefit reductions, pay freezes, higher costs for health insurance, and/or work speed-ups in the wake of their hotel’s acquisition by Columbia Sussex, unionized employees have called for boycotts of the Baltimore Sheraton City Center in Maryland, Hilton Crystal City in Northern Virginia, Anchorage Hilton in Alaska and Hilton Sacramento West in California. Dave Thompson, who has worked at the Hilton Anchorage for 15 years says, “As I see more of our jobs being combined, less of us working, and the housekeepers having to clean two extra rooms a day, I have become more determined to win fair working conditions at our hotel.” And in March 2010, hotel workers’ union UNITE HERE called on customers to boycott 4 more Columbia Sussex hotels in support of a fair process for organizing a union. They are: Westin Washington DC City Center, Westin Emerald Plaza San Diego, Wyndham Chicago and Westin Chicago Northwest. Will Columbia Sussex bring labor disputes to Clearview’s hotels? Columbia

Sussex’s Debt Obligations The Bear Stearns 2006-BBA7 The Clearview SEC filing discloses that five of the hotels they plan to acquire are part of a 10-hotel loan that is guaranteed by Columbia Sussex and CSC Holdings, LLC and matures July 1, 2010. The filing also discloses that four hotels owned by Columbia Sussex subsidiaries have had receivers appointed by courts in 2009 and 2010. The filing, however, does not disclose $1.1 billion in debt that comes due later this year. One of the largest pieces of Columbia Sussex’s outstanding debt is in a CMBS – the Bear Stearns 2006-BBA7 – which was used to finance the acquisition of 14 hotels from Wyndham in October 2005. The $1.1 billion in loans for these 14-hotels made up 79% of the purchase price and matures October 12, 2010. The 2006-BBA7 is also uncommon as a CMBS in that it has no sector diversification and the Columbia Sussex portfolio makes up 93.1% of the outstanding balance. According to Fitch Ratings, on June 23, 2010, the 2006-BBA7 Columbia Sussex loans entered into special servicing, with Fitch identifying “imminent default” as the reason. The $1.1 billion, from Bear Stearns Commercial Mortgage Inc. and Bank of America, is composed of $570 million in Senior Notes and $532 million in Mezzanine Loans. The Senior Notes are cross-collateralized and cross-defaulted, as described in the Offering Circular. The Columbia Sussex Portfolio Loan backing 2006-BBA7 had an original maturity date of October 12, 2007. Three one-year extensions have been granted with the final maturity date of October 12, 2010 approaching. At the time of underwriting, occupancy for these 14 hotels was 76%. In 2009, occupancy had dropped to 60%.[20]The Bear Stearns 2006-BBA7 Mezzanine Debt Two collateralized debt obligations (CDOs) contain portions of the Columbia Sussex mezzanine debt associated with the2006-BBA7 – Guggenheim Structured Real Estate Funding 2005-1 (Guggenheim 2005-1) and Brascan Structured Notes 2005-2, Ltd./Corp. (Brascan 2005-2). Fitch Ratings downgraded all classes of Brascan 2005-2 in November 2009 and all but one class of Guggenheim 2005-1 in February 2010. For Brascan 2005-2, Fitch reported on November 13, 2009 a base case loss expectation of 45.7% and wrote: “The

largest component of Fitch's base case loss expectation is Columbia

Sussex, a

mezzanine loan (11%) secured by an interest in 14 full service hotels

with a

total of 5,821 rooms. The hotels are branded under the Sheraton,

Westin,

Hilton, and Marriot flags. The borrower recently exercised the final

extension

remaining on the loan. While performance of the portfolio has been

stable, the

portfolio is highly leveraged.” For Guggenheim 2005-1, Fitch reported on February 4, 2010 a base case loss expectation of 16.3% and wrote: “The

largest component of Fitch's base case loss expectation is a mezzanine

loan

(19.4%) backed by partnership interests in a portfolio of 14 full

service

hotels (5,822 keys) located across the U.S. The hotels are under the

Westin,

Sheraton, Marriott, and Hilton flags. In line with most hotel

properties, net

cash flow has declined precipitously since the loan was originated.

Fitch

modeled a maturity default in its base case scenario.” Maiden Lane On March 31, 2010 the Federal Reserve Bank of New York (FRBNY) announced that it was making public nearly all holdings of the Maiden Lane portfolios. Maiden Lane LLC was the vehicle the FRBNY formed in June 2008 to acquire $29 billion in troubled assets of Bear Stearns as part of the deal which allowed J.P. Morgan Chase to acquire the collapsing investment bank. The Fed’s recent disclosure reveals that as of January 29, 2010, Maiden Lane LLC had on its balance sheet approximately $900 million combined in current principal balance or notional amount in 6 different classes of Bear Stearns 2006-BBA7 securities. Columbia Sussex Westin Casuarina

Loan in Special Servicing In February 2010, Fitch Ratings released a U.S CMBS Focus Performance Report which looked at the Wachovia Bank Commercial Mortgage Trust Series 2005-C22, containing a loan for the Columbia Sussex Westin Casuarina Hotel and Spa in Las Vegas. The report highlights the Casuarina loan as one of concern, with a modeled loss of 43%. Fitch writes, "As of the TTM [trailing twelve months] ended June 30, 2009 ADR, occupancy, and RevPAR were $118.67, 61.5%, and $72.98, respectively. This represents a RevPAR decline of 26% since YE 2008. The borrower has requested a modification due to the decline in performance of the hotel and Fitch considers it likely that the loan will transfer to special servicing in the near future." On March 31, 2010, Fitch announced the loan entered special servicing. "Reason for Transfer: Imminent Default." UNITE HERE represents

approximately

110,000 members in the non-gaming hotel industry, including employees

at 5

hotels owned and operated by Columbia Sussex. UNITE HERE has labor

disputes

with Columbia Sussex in several cities throughout the United States. [1] Remarks of

New Jersey Casino Control Commission’s Chairwoman Linda

Kassekert,

December 12, 2007.

[2] http://www.state.nj.us/casinos/home/news/pdf/opinionandorder.pdf, p.43 [3] SEC Form S11, p. 121. [4] Kentucky Herald Leader, February 10, 2008. http://www.kentucky.com/news/state/story/314039.html [5] Opinion, Memorandum and Order, Judge Henry Edward Autrey, US District Court (Eastern District of Missouri), September 25, 2009. [6] Opinion, Memorandum and Order, Judge Henry Edward Autrey, US District Court (Eastern District of Missouri), September 25, 2009. [7] Missouri Lawyers Media, October 2, 2009, “Bankrupt Missouri casino wins $42M judgment.” http://www.allbusiness.com/legal/trial-procedure-judges/13136912-1.html [8] Indianapolis Business Journal, March 1, 2008. http://cms.ibj.com/ASPXPages/6iframes/FrontEndArticlesDetailPage.aspx?ArticleID=11919&NoFrame=1 or http://www.ibj.com/article?articleId=13910 [9] Evansville Courier & Press, April 1, 2008. http://www.courierpress.com/news/2008/apr/01/01web-AztarName/ [10] Evansville Courier & Press, May 11, 2007. http://www.courierpress.com/news/2007/may/11/aztar-boss-rips-mayor-yung-says-he-wasn’t/ [11] SEC, Tropicana Entertainment, 10Q, filed December 6, 2007. [12]

SEC 8K, Tropicana Entertainment, April 8, 2008. |

| Contact:

UNITE

HERE RESEARCH DEPARTMENT MARIS ZIVARTS 212-414-7247 COURTNEY ALEXANDER 631-834-4681 275 7TH AVENUE • NEW YORK, NY 10001-6708 |

Another key

factor in the denial

was Tropicana’s “total disregard” for the requirement to create an

independent

audit committee under New Jersey regulations.

Another key

factor in the denial

was Tropicana’s “total disregard” for the requirement to create an

independent

audit committee under New Jersey regulations. arising from

Tropicana Casinos and Resorts’ alleged failure to maintain the Tahoe

Horizon hotel and casino facilities as required by the leases.

Tropicana Casino and Resorts has operated the Tahoe Horizon on the

leased premises since 1990.”

arising from

Tropicana Casinos and Resorts’ alleged failure to maintain the Tahoe

Horizon hotel and casino facilities as required by the leases.

Tropicana Casino and Resorts has operated the Tahoe Horizon on the

leased premises since 1990.”