![]()

advertisement

United States Hotel Construction Pipeline

Executive Summary - Q1 2010

|

News for the Hospitality Executive |

![]()

advertisement

United States Hotel Construction Pipeline

Executive Summary - Q1 2010

|

April 30, 2010 -

In Q1, hotel operations showed continued improvement, with more positive

gains in demand and occupancy than initially expected. The economy has

improved, as GDP has bounced back significantly in the last two quarters.

Job losses are declining, causing unemployment to marginally subside. An

economy continuing to strengthen should be able to withstand the anticipated

declines in stimulus programs scheduled for the second half of 2010.

With increasing demand, room rates should begin to improve in Q2, causing

RevPAR to register positive gains and putting the industry more firmly

on the road to recovery.

The banking crisis continues to weigh heavily on the industry, affecting both transaction activity and the ability of construction projects to acquire financing. There is ample evidence that distressed real estate loans will soon begin to be resolved at a faster pace. Having curtailed lending, with a strong economic and stock market recovery as a tailwind, and with low central bank borrowing costs, lenders have substantially rebuilt their balance sheets. Many are now reporting operating profits. Toward the end of 2010 and into early 2011, there should be increased activity in loan sales, foreclosures, individual transactions and an uptick in M&A activity. With many assets coming to market at discounted prices, there should soon be a wealth of opportunity for investors who can access debt and/or equity. The industry will enter a period where it will be cheaper to purchase existing hotel assets than to build new ones. For now, there are few hotel transactions. According to LE�s recent Sales & Pricing Trends Report, only 411 fee simple sales took place in 2009 that were reported in the public domain. That is a 75% decline from the peak volume year in 2007. At $58,296, 2009�s average selling price per room was also at a cyclical low. Transaction activity in Q1 2010 continues to show YoY volume declines.

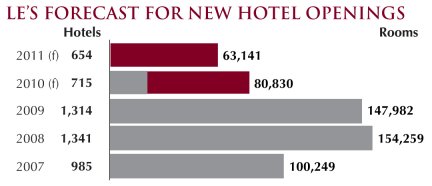

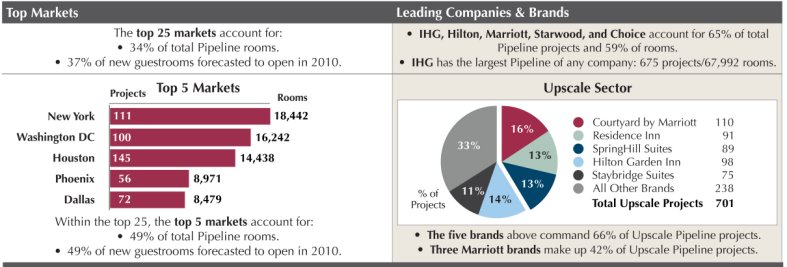

LE�s Forecast for New Hotel Openings

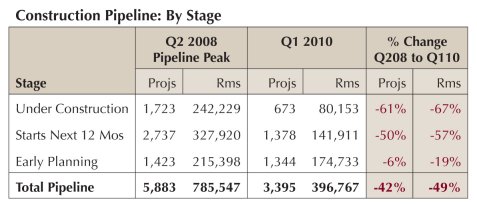

Construction Pipeline

Pipeline Highlights

|

| Contact:

LODGING ECONOMETRICS

|

.