![]()

advertisement

“Internet Travel Tax Fairness Act” / Issues Brief and Talking Points

|

News for the Hospitality Executive |

![]()

advertisement

|

March 2010

- AH&LA is strongly opposed to draft Federal legislation that would

prevent state and local governments from collecting room taxes from

online third party intermediaries (TPIs) when hotel rooms are booked

through such TPIs. If enacted, such legislation would place hotel

companies at a competitive disadvantage with respect to marketing their

own rooms and potentially subject hotel companies to massive tax

increases as State and local government seek to replace the revenue

lost as a result of the TPIs’ tax exemption preference that would be

codified by the legislation, further harming an already struggling U.S.

hospitality industry.

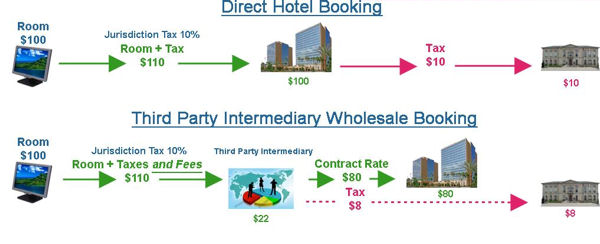

Non-industry members who wish to write to their federal lawmakers about this issue can find a sample letter template on this Webpage. AH&LA members can use the hotelLOBBY grassroots Website to send an email directly to their House or Senate members. BACKGROUND Online travel companies typically choose to calculate state and local hotel occupancy taxes based on the wholesale cost that they pay to a hotel for a room rather than the retail price they receive from the customer for the room. This practice results in lower taxes collected by state and local jurisdictions for rooms booked through an online travel company, rather than directly with a hotel, because the tax calculation is based on the lower wholesale amount. Many jurisdictions have become aware of this strategy and have filed lawsuits against some of the online travel companies for what they contend are unpaid tax revenues. In response, these companies are seeking legislation that would protect this practice by making it a legitimate tax exemption through a federal preemption of state and local authority. Many hotels contract with online travel companies in order to increase their occupancies. These companies include Expedia, Orbitz, Travelocity and others, and are referred to as “third party intermediaries” (TPIs) in the example below. In some cases, a hotel enters a contract with a TPI to provide rooms to the TPI at a discounted rate (the “wholesale cost”). The TPI then posts the rooms for sale at a higher rate to consumers. This is referred to as the “wholesale booking model.” In other cases, a contract between a hotel and a TPI may follow the “commission model” (described below), which is similar to the model used by traditional travel agencies. When using the wholesale booking model, a TPI advertises a room to consumers at a rate higher than its wholesale cost and includes unspecified taxes and fees in its final price. This is the center of the dispute.

This chart may help readers further understand the two

situations:

Local tax authorities become involved Many jurisdictions throughout the country have initiated lawsuits against the online travel companies because of this practice. The City of Columbus, Georgia recently won a suit against Expedia, in which the court found that Expedia should pay taxes to the city based on the advertised room rate, not the lower wholesale cost. Litigation initiated by the City of San Antonio, Texas had a similar outcome. Subsequent to the Columbus, Georgia decision, Expedia, Orbitz, Travelocity, hotels.com, (and possibly others) delisted hotels in Columbus. When an Internet search through these Websites is performed for Columbus, results instead are provided for Phenix City, Alabama, and other jurisdictions. This delisting also has occurred in other jurisdictions. In addition to litigation initiated by local and state tax authorities, many private consumer protection lawsuits have been filed against some online travel companies contending that consumers who booked rooms through these companies using the wholesale model were misled on charges (the amounts labeled as “taxes and fees”). PROPOSED LEGISLATION TO CREATE A NEW SCENARIO Some online travel companies are pressing for Federal preemption legislation that would prevent taxing authorities’ ability to collect taxes from these companies. The legislation would not only exempt online travel companies from remitting as tax the purported "service fee" (i.e., the $2 in the above example), but is written in such a way that it may also exempt the payment of any occupancy tax on rooms booked through online travel companies. Online travel companies contend that this legislation would prevent thousands of different jurisdictions from imposing different taxes on this type of wholesale hotel booking and limit that taxing authority to the 50 States. Yet, hotels would still be required to remit taxes to all taxing jurisdictions—over 7,000 in the United States. Hotels discriminated against The legislation specifically bans hotel Internet booking from equal tax treatment under the law. While the legislation creates a special tax category for TPIs, hotels and hotel companies would be prevented from the tax category. Cities and other jurisdictions that were restricted by the federal government in exercising their tax authority on TPIs would in all likelihood raise taxes on hotels to make up for the resulting budget shortfalls caused by that preemption. Hotels would in essence be punished for being diligent, following the law, and paying their taxes. Legislation that discriminates against hotels by exempting online travel companies from paying occupancy taxes will potentially subject hotels to massive tax increases as State and local governments seek to replace the lost revenue. Although hotels pay all the taxes they owe and have not had

their actions questioned, they will be the ultimate victims of this

legislation. LEGISLATIVE UPDATE On December 17, 2009, AH&LA sent a letter to the House and Senate to express the association's strong opposition to draft legislation (sometimes referred to as the “Internet Travel Tax Fairness Act”) that would prevent state and local governments from collecting room taxes from third party intermediaries (TPIs) when hotel rooms are booked through such TPIs. As the representative of an industry which employs tens of thousands of Americans, AH&LA strongly opposes legislation which would specifically target the lodging industry to place it at a competitive disadvantage and which potentially would subject lodging properties throughout the United States to massive tax increases. AH&LA continues to oppose the proposed Internet Travel Tax Fairness Act. At this time, no legislation has been formally introduced in

either house. Third party intermediaries are also sometimes referred to in literature on this topic as Online Travel Companies (OTC) or Online Travel Agencies (OTA). For more information, contact AH&LA Senior Vice President for Governmental Affairs Shawn McBurney at (202) 289-3123, [email protected]. |

| Contact:

AH&LA |