|

|

News for the Hospitality Executive |

|

| By:

Bryan E. Younge, MAI, ASA | Director, C&W Hospitality and Gaming

Group June 2009 Hospitality is perhaps in one way described as a sanctuary for service, comfort, and safety. Americans are, without argument, a breed that yearns for periods of pampering to disrupt a relatively hard-at-work life schedule. Additionally, uncertainty in the world caused by a quivering stock market, potential pandemics and the like makes the overall desire for hospitality and service ever so paramount to travelers, both leisure and business. Sadly, the hospitality industry is paradoxically the victim of the very events that justify and substantiate its cause. As we have seen with economic cycles over the past few decades, psychologically disturbing events place a toll on the U.S. and lodging market. World events in the first part of 2009 are precipitating sour moods for hotel owners and operators, but potentially sweet ones for wise hotel investors. Hotel buyers in the last hotel down cycle were able to find properties at highly discounted prices. The downturn following 9/11 caused hotel occupancy to bottom out in 2002 at a long-before seen level of about 59.0 percent on a national level, according to Smith Travel Research. At this point in the economic cycle, lenders and equity investors either set high return and debt coverage requirements, or they took their business to markets perceived as more stable. This put tremendous downward pressure on hotel values. Although the downturn was brief (relative to historical standards), a number of assets approaching distress were grabbed by patient hotel bottom feeders that managed to pull together plausible business plans and workable financing that allowed them to reap substantial returns on investment over a three to five year holding period. It was not unusual to see transaction prices as low as 40 percent of replacement cost. The following table illustrates hotel operating performance for reporting assets throughout the United States.

Source: Smith

Travel Research. Republication or other re-use of this data without the

express

written consent of STR is strictly prohibited.

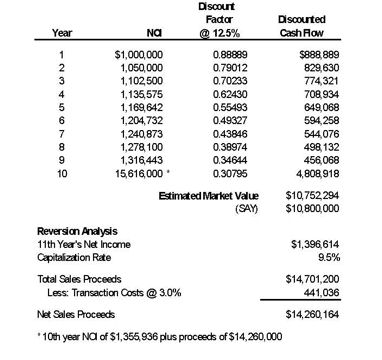

The current downcycle in the hospitality industry could be compared to the days of the energy crisis, in that many individuals believe that a full recovery might take the better part of a decade. Hotel owners and operators, however, are far more sophisticated today than at any time in the past. This, combined with improved infrastructure and travel efficiency would (from an academic standpoint) allow for the industry to mount an efficient comeback. One of the principal issues facing the market is the widespread over-leveraging of hospitality assets. Knowing that repairing the debt markets will take a good amount of time, property owners (at least those who have not been foreclosed on) who believe in this timeline are beginning to bite on low offers. The good news is that the majority of high-quality hotel properties are now well represented by an array of dedicated hospitality investment funds, management companies, franchisors, and surviving REITS that are less likely to bail out or completely vaporize in the harsh realities of current economic conditions. Current hotel company CEOs and presidents have learned from past downcycles, and there seems to be a heightened awareness and understanding of the tools and mechanics involved in making the proper adjustments to survive. Nevertheless, there are a number of high-quality hotel properties in high quality locations that may not have the ability to weather the current economic storm, and if identified on a timely basis, they can be acquired by well-informed investors at low bases resulting in potential strong returns to the investor. Value Driven by Financing Parameters On the note that more focused asset management efforts are poised to take place on distressed hotel assets, it is still important to consider the mechanics that will make this gainful experience realistic. Although in many appraisal scenarios where hotel valuation is based simply on a loaded direct capitalization calculation or an unleveraged discounted cash flow analysis, and where discount and reversion rates employed might erroneously resemble those which are either too conservative or aggressive, it is increasingly critical to consider all of the financing parameters involved in potential market transactions. An appropriate and more granular way to analyze a hotel valuation analysis under volatile and insecure market conditions—such as now—is to also closely consider, and segregate, the debt and equity components of the asset under a leveraged scenario. In order to do this, the analyst needs to dig deep into not only the market for transient accommodations, but also into the capital source markets. Thorough research will allow the analyst to identify specific equity investor return requirements relative to the market, as well as corresponding mortgage interest rates, loan-to-value ratios, selling costs, loan amortization periods, and balloon (payoff) terms. Unlike a standard direct capitalization or unleveraged discounted cash flow analysis, this approach frees up all the moving parts of a property’s expected future performance and sketches a more realistic picture for investors. This is largely important due to shorter-term uncertainty in the economy and lodging fundamentals. In the following exercise, the effects of market lending on the value of a hotel is revealed under two scenarios: first, disposition of the asset in the trough of an economic cycle—similar to that of the early 2000s and (perchance) today; second, the opposite extreme where economic conditions are near a crest. In both cases, the valuation analysis compares a leveraged transaction to an unleveraged one, with all input factors recognized by the market for (say) an average mid-rate full-service hotel in located in a highly impacted North American market with future rebounding potential. Cash flows grow at 3.0 percent annually, except in the first two years of Example 1 when 5.0 percent growth is incorporated. This is intended to suggest a recovery from an extreme downside position. Example 1: Unleveraged DCF vs. Segregated Mortgage and Equity Valuation. Low Market and Stringent Financing. Unleveraged

Discounted Cash Flow

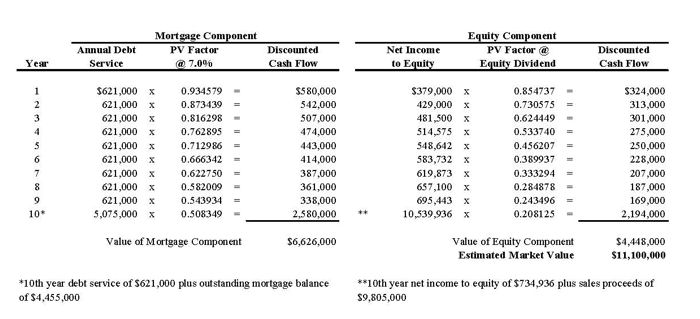

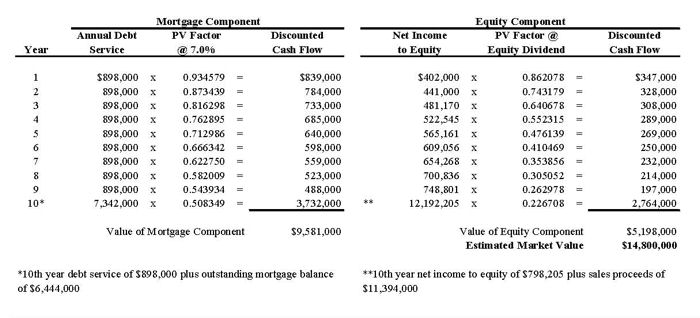

To compare, the following analysis recognizes the same projected net income to the property. This analysis suggests that the same market value conclusion is rendered under stringent lending and investing requirements, as derived from the market. Please note that this analysis fundamentally includes five degrees of factoring, versus the three degrees of factoring shown previously. Segregated

Mortgage and

Equity Valuation

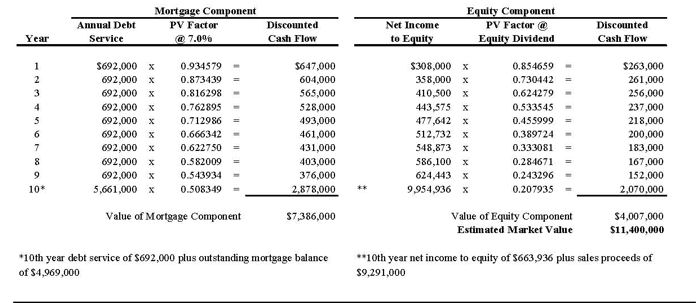

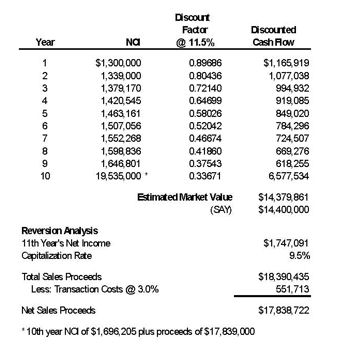

Unlike the unleveraged analysis, the segregated mortgage and equity model allows us to determine the effects of changing lending or investing requirements. The following analysis illustrates a ± $300,000 effect on property value, holding all else constant, when the lender requires a loan-to-value ratio of 65 percent, versus 60 percent presented earlier.  Example 2: Unleveraged DCF vs. Segregated Mortgage and Equity Valuation. Peak (or Stable) Market and Typical Financing. Reverting to the original argument of this narrative, current economic conditions in North America and other leading economies are yielding opportunities for hotel investors to locate profitable deals. As seen from a number of ventures, hotels were purchased near the trough of the lodging industry and sold in five to ten years thereafter for returns of 40 to 50 percent…in some cases, approximating 70 or 80 percent. Such profitability, albeit not necessarily a norm, was secured in part through effective management freshly experienced from critical cost control, but largely due to changing financing parameters. One example includes the investment of the 296-unit Rosemont Suites in Rosemont, Illinois, which was purchased in the beginning part of the 1990s for $18.4 million. The owners committed a modest $2.0 million in upgrades following the transaction, and sold the property to Lowe Enterprises, Inc. for $43.0 million eight years later…a ±66 percent nominal profit (inflation adjusted). Another example takes place in the more recent economic recovery period (post 9/11) in downtown Chicago, when the 751-unit Westin Michigan Avenue was purchased in early 2005 for $137 million. The owners committed only ±$3 million in capital improvements (less than $4,000 per key) following the acquisition, and sold the property to LaSalle Hotel Properties for about $215 million only one year later. This represents an impressive ±56 percent nominal profit, inflation adjusted. In addition, the Wyndham Glenview was acquired by a private investor in January 2005 for $9.7 million, who simply flipped the property five months later for $1.9 million more than the purchase price. Two years after that, the property resold again for $22.1 million after committing “only minor PIP items.” This signals a nominal profit of more than 80 percent. In all cases, the venturists attributed the investment success largely on improved cash flow vis-à-vis strong fundamentals and surprisingly less so on the slackening financing environment. In an effort to juxtapose the two valuation models represented by a soft economic climate with each other and again in a stronger economy, the same exercise was performed using the same hotel subject. In this analysis, net operating income increases at 3.0 percent annually, although it is stabilized with income that begins in year one that is 30 percent higher. In both the leveraged and unleveraged analysis, discount, capitalization, and investing parameters are reflective of a property with strong operating performance in a relatively stable North American market. As illustrated, there is a noticeable difference in potential value which might have been overlooked during the underwriting process without considering various market-oriented financing parameters. Unleveraged

Discounted Cash Flow

Segregated

Mortgage and

Equity Valuation

Looking Ahead The closer one becomes to current events as it relates to lodging trends, not to mention the fact that the stock values for several hotel companies recently reached long-term lows, it’s not surprising that pessimism would become the prevalent state of mind. However, optimists are less often pointing to this notion and more towards the fact that hotel REIT shares are, on average, up nearly 100 percent since their lows. Although the wider spectrum of investment in real estate properties and funds has started become less stigmatized somewhat in the wake of the recent financial meltdown (vis-à-vis the breakdown of corporate ethics and the resulting insecurity of general non-real estate shareholders), lodging ventures have often been perceived to be too risky. Doubling up on this whammy is dropping occupancy and room rates across most of the western hemisphere. All the same, travel is ultimately a necessity for the United States’ propensity to continue to be a global competitor, and prevailing industry sentiment is that lodging fundamentals will not get much worse despite some residual uncertainty in the world economy. Accordingly, smart hotel deal seekers are beginning to identify true opportunity. The valuation methods presented in this article are an example of how inherent profit could be overlooked. And, looking at past cycles as a preliminary basis to model future growth in a hotel’s cash flow might indicate that investments have more appeal than initially perceived. A few quarters from now, we will have a clearer vision of what the recovery for the lodging economy will look like, and how sweet the rewards could be for those venturists who were among the first to step off the sideline and onto the playing field. Mr. Younge is a Director and Midwest Area Leader of the Hospitality & Gaming Group, a full service hospitality organization within C&W specializing in appraisal and consulting. Mr. Younge has completed appraisal, consulting and litigation related assignments on a wide range of hospitality assets throughout North America, Central/Latin America, Europe and the Pacific Rim. He has been active in real estate valuation and consulting since 1998, and has a Bachelor of Science Degree from Cornell University, as well as a Masters in Business Administration from Northwestern University's Kellogg School of Management. |

| Contact:

Bryan E. Younge, MAI, ASA |

| Also See: | The

Role of Hotel Brands in the War of Survival / May 2009 |

| Local Internet Marketing Strategies for Franchised Hotels; Complement the Brand’s Efforts and Capture Local Internet Revenue Opportunities / Max Starkov and Mariana Mechoso / September 2008 |

.