|

News for the Hospitality Executive |

U.S. Hotel Construction Pipeline Decelerating Rapidly

LE First Quarter 2009 Results

.

| PIPELINE OVERVIEW

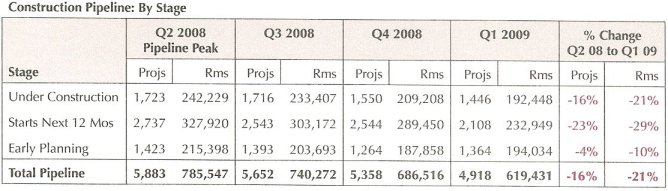

In Q1 2009, the US Construction Pipeline decelerated rapidly and now stands at 4,918 projects / 619,431 rooms. Compared to the Pipeline peak in Q2 2008, this is a drop of 16% by projects and 21% by rooms, a substantial fall-off for a three-quarter period. Current pipeline trends are beginning to reflect the deep recession in the economy, the banking crisis, the evaporation of mortgage lending, and serious shortfalls in lodging operating performance.

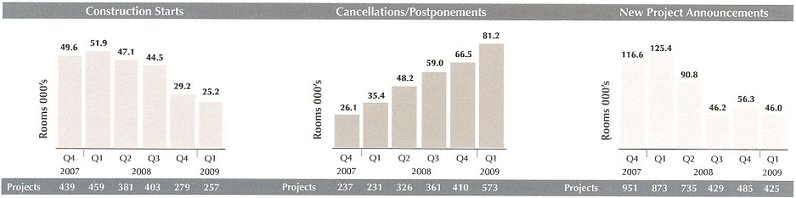

While selected smaller projects are still able to locate financing under stringent terms, larger-scale construction cannot. As a result, numerous projects are stalled in the pipeline as developers struggle with credit difficulties and the changing operating environment. Accelerating project cancellations are now reaching the highest level LE has ever recorded. New Project Announcements into the Pipeline are trending further downward. Those projects seeded in the pipeline at mid-decade and already financed are now opening at an increased speed. New supply additions will reach a cyclical peak in 2009 and then taper off beginning in 2010. At Q1, there were 1,446 projects / 192,448 rooms Under Construction, a drop of 22% and 21% respectively from the Q2 2008 peak. The impact of the financing crisis is evident in the slowed forward migration of projects. Presently, just 29% of total pipeline projects are presently Under Construction, with totals expected to continue to trend downward until 2011. The swift drops have prompted LE to revise its Forecast for New Hotel Openings lower for 2009 by 4,238 rooms or 2.6% and by a much larger 15,169 rooms or 9.4% in 2010. Projects Scheduled to Start Construction in the Next 12 Months have declined precipitously from the Q2 2008 peak, down 23% by projects and 29% by rooms. The slump is a result of the rise in Cancellations and Postponements, which is expected to continue. At 2,108 projects/232,949 rooms or 43% and 39% of the Total Pipeline, respectively, Scheduled Starts show a large backup of projects that lack the financing to start construction. 12-month starts will also be a source of additional Cancellations and Postponements, as the economy and the lodging operating environment add to growing developer concerns. Projects and rooms in Early Planning are declining, but more modestly. This stage is generally where New Project Announcements enter the pipeline, and also serves as a repository for larger projects that are confirmed as being actively pursued by developers, but currently have little chance of locating financing. Marginal projects will continue to drop out, as the declining economy affects feasibility and a developer�s willingness to continue to invest in idle projects. LE expects overall pipeline totals to continue to decline at least into 2011. KEY PIPELINE METRICS At 257 projects / 25,179 rooms in Q1, Construction Starts have continued to trend downward and are expected to bottom in 2010. Lending is practically non-existent for hotels greater than 200 rooms, while smaller projects, requiring mortgages of less than $15 million, can sometimes acquire financing. A number of community banks are active, but they are very selective and the terms are strict. A reversal in starts cannot occur until the larger banking issues are resolved and new mortgage lending concepts are created, which will likely be a prolonged process. With development constrained by the lending and lodging operating conditions, Cancellations and Postponements have propelled upward since mid-2007, when lending issues first arose. In Q1, 573 projects / 81,221 rooms were cancelled or postponed. This trend is expected to continue throughout 2009 and later top out, as projects having marginal feasibility and those that cannot secure financing exit the pipeline. After a brief tick upward in Q4 2008, when both developer and franchise

sales teams rushed to finalize agreements by year-end, New Project Announce¬ments

(NPA�s) into the Pipeline have resumed their downward trail. At 425 projects

/ 46,006 rooms, the room count is down 63% from the cyclical peak established

in Q4 2007. In a short span, NPA�s have dropped to their lowest level in

over five years, with expectations of extending even lower before

LEADING FRANCHISE COMPANIES Of the 425 new projects announced in Q1, 83% or 353 projects have already

chosen a brand. 293 of these projects selected brands from the top five

franchise companies, the most popular being brands with proto¬typical

models less than 150 rooms, which are right-sized for the credit markets.

For Hilton, it�s Hampton Inn and Suites and Hilton Garden Inns. InterContinental

has a large portfolio consisting of Holiday Inn Express, Candlewood, Staybridge

Suites and the newly designed Holiday Inn. Marriott has Fairfield and Town

Place Suites, as well as smaller models of Spring Hill Suites, Courtyards

and Residence Inns. Choice has Comfort Inn and Suites and Sleep Inns. Wingate

and Baymont are Wyndham�s mid-market new construction brands, while Microtel

dominates the economy segment.

TRANSACTIONS - SALES VOLUME & PRICING TRENDS Since peaking in 2007 with 1,606 sales, transaction activity has slowed dramatically with the near disappearance of financing. In 2008, individual transactions plummeted 47% to 846 transactions. For Q1, only 94 transactions took place, indicating a continued and even steeper fall-off in deal- making ahead. The 2008 average selling price (ASPR) was $85,899 per room. Of the total 846 transactions, 69, or 8% of the total, were larger than 200 rooms, with an ASPR of $123,823. The remaining 777 sales were properties smaller than 200 rooms and had an ASPR of $71,904. LE expects sales volume to remain low and for selling prices to be wildly skewed in the near term, as there will be only a small group of sellers and buyers active in the marketplace. For most sellers, it is not a preferred time to sell. Only sellers that need to move assets to raise cash to cover other capital concerns or those that have distressed assets and are forced to sell will be active. Further, lenders and mortgage servicers will press an increasing number of foreclosure auctions. Because of the lack of available financing and a scarcity of ready investors, overall selling prices are expected to continue to trend downward over the next two years. However, developers of newly constructed, branded hotels in top markets can ensure themselves an immediate profit over their construction cost. There are certain investor groups eager to purchase these promising investments. Two such transactions occurred in New York City in Q1, one a 298-room, newly constructed Hilton Garden Inn, which sold for $121,200,000 or $406,711 per room, and the other a 244-room Fairfield Inn selling for $99,500,000 or $407,787 per room. Because of today�s depressed credit markets, qualified buyers are few and will likely continue to be so for the near future, resulting in little to no competition for assets. However, with owners unable to resolve looming refinancing issues ahead and the operating environment reaching new lows, an increasing flow of higher quality assets should soon begin to surface. That should prove to be the catalyst for renewed capital formation that will increase the pool of qualified and ready-to-act investors. ABOUT LODGING ECONOMETRICS With over 30 years of experience, Lodging Econometrics (LE) is the foremost source of global business development intelligence for hotel franchise companies. LE serves as your strategic planning partner. We identify every opportunity available to your company worldwide, based on your particular market share goals, sales objectives and brand specifications. |

| Contact:

Lodging Econometrics

|

.

.

|

|

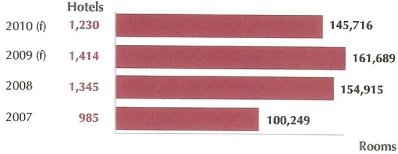

At

1,414 hotels/161,689 rooms, New Hotel Openings will reach a cyclical peak

in 2009, but miss setting a new all-time high by about 8,500 rooms. Reductions

have already been made for 2009 and 2010 as a result of declines in the

pipeline, but more recently because of a growing number of underway projects

that have stopped mid-construction. In 2008, 53 projects / 13,116 rooms

halted construction. Thus far, Q1 has 28 projects / 5,276 rooms suspending

construction, more than half the project count for all of 2008. Generally,

these are projects where the developer started building without having

all financing in place. While a failure to complete financing may be the

dominant reason, changes in the operating environment and/or competing

needs for the developer�s investment capital may also be factors. Additional

downward revisions in the Forecast may need to be made if credit availability

doesn�t improve soon.

At

1,414 hotels/161,689 rooms, New Hotel Openings will reach a cyclical peak

in 2009, but miss setting a new all-time high by about 8,500 rooms. Reductions

have already been made for 2009 and 2010 as a result of declines in the

pipeline, but more recently because of a growing number of underway projects

that have stopped mid-construction. In 2008, 53 projects / 13,116 rooms

halted construction. Thus far, Q1 has 28 projects / 5,276 rooms suspending

construction, more than half the project count for all of 2008. Generally,

these are projects where the developer started building without having

all financing in place. While a failure to complete financing may be the

dominant reason, changes in the operating environment and/or competing

needs for the developer�s investment capital may also be factors. Additional

downward revisions in the Forecast may need to be made if credit availability

doesn�t improve soon.