July 28, 2008 (USA) � Lodging Econometrics (LE), the Global Authority

for Hotel Real Estate, has released its US Construction Pipeline Report

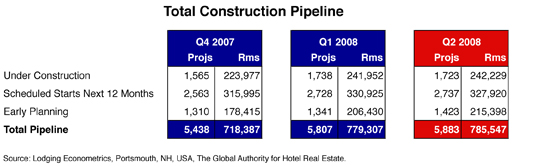

for Q2 2008, announcing 5,883 projects with 785,547 guestrooms in the Total

Pipeline. LE President Patrick Ford noted, �Showing only a moderate quarter-over-quarter

(QoQ) increase, project and guest room counts in the Total Pipeline are

at new peak levels, but appear to be cresting. New visibility on the economy,

the lending crisis and lodging operating trends emerged during the second

quarter, which served to dampen developer sentiment considerably. As a

result, key development metrics have softened, indicating that both project

migration within the existing Pipeline and the pace of New Project Announcements

into the Pipeline are beginning to ebb.�

.

Total rooms Under Construction are at a record high of 242,229. Further,

Early Planning totals of 1,423 projects/215,398 rooms are at historic highs,

while those Scheduled to Start Construction in the Next 12 Months, a total

of 2,737 projects, are at a record level as well.

All projects in the Pipeline have dedicated land parcels, are being

actively pursued by developers and have been verified by the brands.

Availability of Lending Drives Development

For the first time in this cycle, the migration of projects up the

Pipeline stalled significantly in Q2, clearly demonstrating that the lending

crisis is now creating a serious drag within the Pipeline. Projects from

the �Scheduled Starts Next 12 Months� stage did not flow forward proportionately

into �Under Construction,� and are likely to continue to be impeded.

Ford noted, �For some time, there has been no financing available at

either the Wall Street or National Bank level. During Q2, balance sheet

problems began to surface in regional banks and some community banks too.

It is becoming more increasingly difficult to source financing for 100-200

room projects, which account for 44% of the Total Pipeline, as well as

the majority of upscale and mid-market projects currently in the Pipeline.�

The withdrawal of lending from the economy is growing more serious

for developers. The highly credentialed investor group with an exceptional

hotel project, able to invest a large equity slice and absorb difficult

lending terms may gain access to financing. However, the overall availability

of financing is quite thin, forcing many developers to the sidelines. With

few signs that conditions will change before mid-year 2009 at the earliest,

Pipeline totals will likely decline over the next 4-6 quarters.

�In the months ahead, the �Starts� stage will remain disproportionately

large, as many developers are required by their franchise agreements to

start construction within 12 months,� commented Ford. �Numerous agreements

are likely to be extended, as everyone awaits a resolution to the lending

crisis.�

�Since most New Project Announcements enter the Pipeline in Early Planning,

that stage will back up as well, as developers continue project planning

despite not knowing exactly when financing will again become available.�

Project Migration Within the Pipeline is Slowing

As

would be expected, Q2 Construction Starts declined to 381 projects/47,107

rooms, down 78 projects/4,757 rooms from Q1. Despite the decrease, this

is still a healthy level that will contribute to New Hotel Openings late

in 2009 and in 2010. As

would be expected, Q2 Construction Starts declined to 381 projects/47,107

rooms, down 78 projects/4,757 rooms from Q1. Despite the decrease, this

is still a healthy level that will contribute to New Hotel Openings late

in 2009 and in 2010.

Another sign of shifting developer sentiment is the acceleration of

Project Cancellations. In Q2, 327 projects/48,452 rooms were officially

cancelled. This is the highest number seen since Q4 2001 in the immediate

wake of 9/11.

One Cycle Ends, Another Begins

Developers had initially hoped that the lending crisis would produce

just an abbreviated pause to this decade�s economic recovery. However,

in Q2 everything changed as most open questions about economic visibility

were answered. The problems are now seen as more widespread and more entrenched.

We can now conclude that the economic upswing was clipped short by the

crisis and officially ended in Q4 2007, drawing to a close one of the most

anemic recoveries in the post-World War II era, and that a new downward

cycle has begun, tempering developer bullishness.

The housing crisis, failed debt instruments, weakened Wall Street institutions,

and national and regional bank distress have all combined to effectively

limit access to credit. At the same time, prices for basic consumer needs,

including oil, food and transportation, are soaring. Oil prices at $130

per barrel and gas at $4.00 per barrel affect everything. Tipping points

have been reached.

Without access to credit, consumers have cut back substantially on

discretionary spending, including travel. In response, affected businesses

have been consolidating operations, conducting lay-offs and implementing

cost reduction programs, including cutbacks on both individual and meeting-related

travel. Travel will continue to soften, particularly in resort destinations,

as airline carriers have programmed significant capacity cuts for the fall

and winter months.

Many other developed countries are now mirroring our slowdown. They

are already experiencing or are set to see a fall-off in economic growth.

For emerging economies like China, Russia and India, it will be from a

much higher growth rate plateau. With this global economic slowing already

underway, inbound tourism from overseas, which has bolstered occupancies

on both the East and West coasts, could soften as other countries struggle

with rising inflation and less disposable income.

What is remarkable is that with so much economic change being absorbed,

the US downturn is still more moderate than what was feared last fall.

So far, not a very sharp fall-off or a deep recession, both the economy

and the lodging industry have been oscillating, plus or minus, around the

zero growth line. A sideways continuation, even prolonged, would not be

an unfavorable outcome.

Changing Trends in Lodging Operations

These changes have combined to significantly affect lodging operations.

Occupancies are falling, putting increasing pressure on room rates. RevPAR

growth, with a consensus forecast of a meager 4.4% at the beginning of

the year, finished at +1.5% for the first six months and will likely continue

downward as a slow-starting summer travel season unfolds.

Guest room demand is the major culprit at �0.3% year-over-year growth

at the end of Q2. Demand growth is likely to be negative for the year,

an unhappy consequence and a rare happening. It would be the first negative

growth year since 2001 and only the third in the last 25 years.

Most of the larger questions are now answered, but an important one

still remains: How long will the downturn last? With a hyperactive Treasury

Department and Federal Reserve Bank fashioning solutions and taking bold

action to set a floor to the financial fallout, LE�s expectation is that

it still could persist for another 12 to 18 months. The metric for operators

to monitor, as it is for lodging developers, is the return to a normal

lending environment. All growth is stymied, and a turnaround cannot begin

without greater access to lending.

New

Project Announcements Slowing Down New

Project Announcements Slowing Down

New Project Announcements into the Pipeline are the best metric for

measuring developer sentiment, which, in addition to the availability of

lending, is now beginning to be influenced by declining trends in existing

operations.

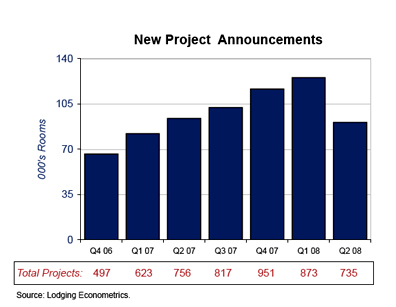

Exceeding 100,000 rooms for three consecutive quarters, New Project

Announcements reached a cyclical high of 125,442 rooms in Q1, then tailed

off sharply in Q2 to 90,793 rooms, a QoQ drop of nearly 28%.

LE expects quarterly New Project Announcements to continue to fade

until capital markets are restored. As the average 150-room project is

in the Pipeline for approximately 30 months, these declines will not impact

New Openings until mid-2010 and early 2011.

New Openings On the Rise as the Pipeline Unfolds

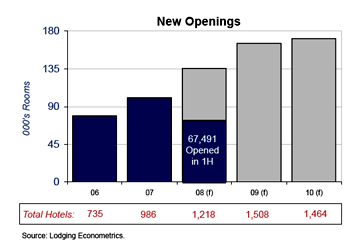

In 1H, 580 New Hotels opened, adding 67,491 guest rooms to Current

Supply. From a record peak, the Pipeline is now unfolding in earnest.

LE�s

Forecast for New Hotel Openings calls for a total of 1,218 hotels/135,373

rooms to open in 2008, a 2.9% gross growth rate, and 1,508 hotels/165,425

rooms to open in 2009, a 3.4% gross growth rate. The net change for New

Supply will likely be ± 0.3%-0.5% lower. With 1,723 projects/242,229

rooms currently Under Construction, LE�s Forecast for the next 18 months

is virtually certain. LE�s

Forecast for New Hotel Openings calls for a total of 1,218 hotels/135,373

rooms to open in 2008, a 2.9% gross growth rate, and 1,508 hotels/165,425

rooms to open in 2009, a 3.4% gross growth rate. The net change for New

Supply will likely be ± 0.3%-0.5% lower. With 1,723 projects/242,229

rooms currently Under Construction, LE�s Forecast for the next 18 months

is virtually certain.

For the first time and however tentatively, LE is forecasting 1,464

hotels/170,974 rooms to open in 2010, also a 3.4% gross growth rate. That�s

far less than a Pipeline of this size would normally produce. The 2010

Forecast anticipates delays, cancellations and further declines in New

Project Announcements. Understandably, the variables are very difficult

to tie down with any certainty. The forecast will almost certainly change

as more information about the economy, operating trends, the banking crisis

and loan availability is gleaned moving forward.

LE�s Outlook at Mid-Year

Questions have been answered and visibility is certain. It is not an

interruption in the previous growth cycle, but the start of a new, downward

cycle that hopefully will lead towards a soft landing.

With both the housing and lending bubbles bursting simultaneously,

the downturn is likely to be prolonged. As of yet, it is not steep or recessionary.

It is a unique and unusual challenge in that it requires lenders to raise

capital in order to re-enter the lending business. They need to rebuild

their balance sheets: take write-downs, consolidate and sell assets, cut

dividends, find new equity investors, and so on. The process will certainly

be long and tedious.

The hope is that the economy does not falter much further while that

scenario unfolds. Being tied heavily to the retreating consumer and retrenching

businesses, the lodging industry can do nothing but wait for the country�s

financial problems to resolve while struggling through a period of negative

demand growth, pressure on prices and rising operating costs. Margins will

suffer and profits will decline, albeit from record peaks established in

2007.

At this time, developers cannot access lending at reasonable terms.

If their projects are already in the Pipeline, they cannot progress towards

construction. As a result, the Pipeline will likely stall and �bunch up�

over the next 18 months. Cancellations will increase, as they did at the

end of the dot-com bubble and again after 9/11.

New Project Announcements into the Pipeline will continue, but at a

significantly reduced rate. With New Openings leaving the Pipeline at an

accelerating rate, Total Projects in the Pipeline will recede over the

next few years, clearing the way for the next development cycle in the

middle of the next decade.

On the plus side, the credit crisis will sharply curtail future supply

growth, but not until late 2010. In the near term, there will be the appearance

of overbuilding because of a widening supply/demand imbalance. In reality,

it is not overbuilding but the collapse of demand growth, a rare occurrence.

The rate of New Supply coming online over the next 30 months would have

been easily absorbed, had the economic recovery not been clipped short.

For now, the consensus is that the slowdown in lodging operating trends

will last at least into the second half of 2009, and will likely be followed

by a slow, moderate upswing. It�s hard to discern what the next economic

growth engine will be and when the necessary elements will coalesce to

propel it. Only time will tell.

Lodging Econometrics (LE) of Portsmouth, NH is the global authority

for hotel real estate. LE conducts Supply Side research for all markets,

countries, companies and brands � worldwide!

|