|

News for the Hospitality Executive |

Lodging Econometrics Quarterly Report Shows Middle East

Hotel

Construction Pipeline at 527 Projects/155,989 Guestrooms

.

New Hotel Openings to Accelerate

Through 2008 and 2009

.

|

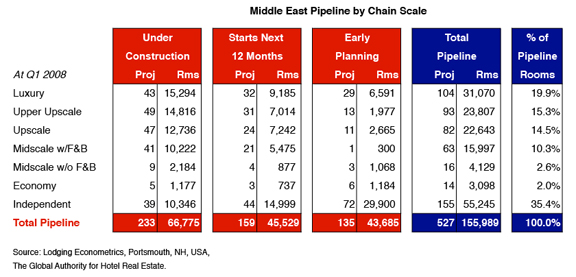

June 11, 2008 - According to its newly released Construction Pipeline Report for the Middle East, Lodging Econometrics (LE), the Global Authority for Hotel Real Estate, shows the Total Construction Pipeline at a record high 527 projects with 155,989 guestrooms at the end of Q1 2008. LE President Patrick Ford commented, �There has been a tremendous surge in the Development Pipeline, particularly in Dubai, Abu Dhabi, Saudi Arabia, Oman, and Qatar. World-class, master planned communities � luxurious beachfront resorts and residential developments, business and financial centers, modern new airports, and tax-free business and industrial zones - are providing once-in-a-lifetime opportunities for developers, investors, global lodging brands, architectural and design firms, and vendors/suppliers to the industry.� .  A cyclical high 233 projects/66,775 rooms, or 43% of the Total Pipeline, are already Under Construction. Total project and room counts Scheduled to Start Construction in the Next 12 Months peaked in Q4 2007, and declined slightly to 159 projects/45,529 rooms in Q1 2008. There are 135 projects/43,685 rooms in Early Planning, which is also a cyclical high. All projects included in the LE Pipeline have dedicated land parcels, are being actively pursued by developers and have been verified by the brands. LE�s Forecast for New Hotel Openings In Q1 2008, 13 projects having 3,802 rooms opened, a fraction of what is due to come online. New Openings are set to burst forward from now through 2010. LE�s Forecast calls for another 88 projects/23,756 rooms to open during the remainder of 2008, with a further 167 projects/43,428 rooms expected in 2009. LE�s Forecasts are based on current trend lines, and do not account for a steeper decline in worldwide economic conditions or for additional declines in the availability of construction materials and other shocks to construction costs which could cause further project delays and cancellations. A Development Pause May Be in the Offing Certain exigencies may cause developers to slow their pace for future planning and take a brief pause. The high volume of development here and around the world is creating intense competition and causing critical shortages in construction materials, like steel and concrete, and in skilled labor. Increased labor costs are also a factor. With inflation spiraling upward, construction costs are soaring, with some commenting that they have doubled in the past four years. The financial instability of some subcontractors is also compounding the problem. With a substantial wave of New Openings projected for 2008, 2009, 2010 and beyond, there is concern that such a sizeable influx of new supply will deflate occupancy rates and put downward pressure on room rates, which have been among the highest in the world. All of this is at a time when a global economic slowdown is beginning to unwind. This could moderate the flow of inbound tourism, making the absorption of these new guestrooms more difficult than originally contemplated.

These mounting developer concerns are reflected in the Pipeline. New Construction Starts, reported at 28 projects/8,760 rooms in Q1 2008, have been in a holding pattern for three quarters, while the Pipeline grew to a record high. This indicates project movement up the Pipeline is quite sluggish. Many projects appear to be �parked� in Early Planning and Starts in the Next 12 Months as developers sort through the new difficulties.

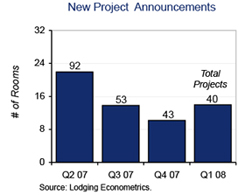

A solid indicator of developer sentiment, New Project Announcements have also been in a holding pattern, with Q1 2008 totaling just 40 projects/14,011 rooms. This is the third consecutive quarterly decline in project counts and a 57% drop from the 92 projects announced in Q2 2007. Both metrics are clear indications of a slowdown in New Hotel Openings

early in the next decade.

Dubai has long been the global media focus of the Middle East as it progressed with its strategic plan for transforming the Emirate through incredible, large-scale development: landmark structures designed by the world�s leading �starchitects;� exotic resorts and spas at renowned beaches, including Nakheel Properties� spectacular man-made Jumeriah Palm, the world�s largest land reclamation project; soaring office towers; luxurious residential communities; state-of-the art airports and convention centers. Reportedly, 40% of the world�s construction cranes are in Dubai. Lodging development has flourished in Dubai. The Total Pipeline has 162 projects/60,503 rooms, which will double its existing upscale guestroom supply when developed out completely. Half of Dubai�s Total Pipeline, 92 projects/30,107 rooms, is already Under Construction. There are 34 hotels/11,299 rooms expected to open in the last three quarters of 2008, while 54 hotels/ 15,360 rooms are forecast to come online in 2009. Dubai contains 31% of all projects and 39% of all rooms in the Total Middle East Pipeline. If viewed as a �city state,� Dubai would have the largest Construction Pipeline of any metropolitan area in the world, even larger than Las Vegas, New York, Washington, London, Shanghai, or Beijing. Other Master Plan Developments in the Works Abu Dhabi, the government center of the United Arab Emirates (UAE), has embarked on its own Emirate-wide development program. Strategically, it wants to establish its role as the Middle East�s cultural/educational hub, being home already to Abu Dhabi University and a satellite campus of Paris-Sorbonne University. With 73 projects/21,809 rooms, Abu Dhabi has the second largest Pipeline in the region. Nearly 25% of the rooms are Under Construction, while 47% are Scheduled to Start Construction in the Next 12 Months. Saadiyat Island is the designated cultural center, and will have a Frank Gehry-designed Guggenheim Museum, a branch of the famous Louvre Museum, a world-class performing arts center and concert hall. The shore-lined Corniche and the adjoining retail, financial and embassy district have 11 projects/3,773 rooms in the Pipeline. Yas Island, a $40 billion dollar development by Aldar Properties, will include a Formula One racetrack and the Ferrari World Theme Park, along with 11 hotel projects in various stages of development. Saudi Arabia�s plan is to become the religious and cultural center of Islam. It has 52 projects in the Pipeline, nearly 42% of which are already Under Construction. Much of the development is in the religious centers of Jeddah, with 16 projects, and Islam�s Holiest City, Makkah, with 10 projects. The capital city, Riyadh, has 10 projects in the Pipeline. Oman�s Pipeline has 51 projects, with over 63% of the guestroom activity in the capital, Muscat. Qatar�s Total Pipeline is 35 projects/11,350 rooms, most of which is in Doha. Egypt aims to expand its tourist appeal by further developing its beachfront resorts on the �Red Sea Riviera,� including the former port town of Sharm El-Sheikh, popular domestic destination Taba and the beach-lined town of Hurghada. The country has 31 projects/10,922 rooms in its Pipeline. An Extraordinary Opportunity for Global Brands Of the 527 projects in the Total Pipeline, 341 or 65% have already made a branding decision, while 155 projects have yet to decide. LE anticipates that 75% of those will make a branding decision prior to opening. Such explosive growth makes the Middle East one of the most important areas for Global Hotel Brands. With 77% of total development in the upscale segments, it serves as an important showcase area for companies to establish and advance their brands through large, iconic, luxurious hotels. Middle East-based Rotana Hotels, Inns & Suites has 33 projects/10,256 rooms, which is the largest guestroom count in the Pipeline. Of its total projects, 17 are Under Construction. The company has an aggressive strategic plan, with a stated goal of having 65 hotels open by 2012. The globally renowned Jumeirah International hotel company has 10 ultra-luxury properties in the works, including The Palm Trump International Hotel on Palm Jumeirah Island, which will have 300 hotel rooms and 360 private residences, and the 330-room Jumeirah Desert Pearl in Dubailand. Fairmont Hotel and Resorts, which is majority owned by Saudi Arabia�s Kingdom Hotel Investments, also has 10 luxury properties in the Pipeline, including one on Palm Jumeriah with 372 hotel rooms and 558 private residences and the 1,005 room Fairmont overlooking the Holy Mosque in Makkah. France�s Accor has the largest Pipeline project count in the Middle East with 34 hotels. There are 8 Sofitels and 11 Novotels. Accor is also one of the pioneer mid-market developers in the region, with 13 Hotel Ibis projects in the Pipeline. The InterContinental Hotel Group has 8 InterContinentals and 5 Crowne Plazas in the Pipeline. InterContinental is also accelerating a mid-market program in the region with 9 newly designed, prototypical Holiday Inns and 3 Holiday Inn Express�. Europe�s Rezidor Hotel Group has 9 Radisson SAS properties under development, and 5 of its mid-market brand, Park Inn. Switzerland�s Mövenpick also has an impressive Pipeline of 24 projects, 10 of which are located in Dubai. Germany�s Kempinski Hotels & Resorts, which operates the world famous Emirates Palace Hotel in Abu Dhabi and the Kempinski Hotel at the Emirates Mall in Dubai, has another 10 under development, including projects in Syria, Bahrain, Lebanon, and Jordan. North American-based companies see the Middle East as an important target for their brands. Marriott has 23 projects in the Pipeline, led by 7 Ritz Carltons, but also including JW Marriott, Renaissance and Courtyard properties. Starwood is focused on its high-end offerings, having a total of 21 Pipeline projects from its Luxury Collection, St. Regis, W, Le Meridien, Westin and Sheraton Brands. Hilton has a total of 11 projects under development between its Conrad and Hilton labels. Based in Singapore, Banyan Tree Hotels & Resorts has 6 each of its celebrated Banyan Tree and Angsana Resorts & Spas in the Pipeline. These are smaller, luxurious, one-of-a-kind, boutique designs where the resort and spa are the destination itself. Summary After rapid growth throughout the middle of the decade, the Middle East Construction Pipeline is about to unfold in earnest. Approximately 67,000 rooms are expected to open during the last 3 quarters of 2008 and in 2009, most of which are already Under Construction, making LE�s forecast a near certainty. New Openings will be heavy in 2010 as well. A build-out of the existing Pipeline will mean a doubling of current upper upscale and luxury supply. Indications are that project counts in the Total Pipeline are at or near peak for this decade. Rapidly spiraling construction costs, a shortage of construction materials and skilled labor, along with a softening in the global economy with its potential impact on inbound tourism, appear to be raising concerns in the development community. With the unfolding of 70-80% of the existing Pipeline as New Openings

in 2008-2010, developers may well be watching how this current development

wave will be absorbed before entering into another period of rapid growth.

It could prove advantageous to have such a period of assessment to see

how well tourist and business demand growth keeps pace with what will be

a significant supply increase across the region during the next three years.

Lodging Econometrics (LE) is the global authority for hotel real estate. LE conducts Supply Side research for all markets, countries, companies and brands � worldwide! © 2008 Lodging Econometrics |

| Contact:

Kathleen Hurley

|

|

|

A

Back-Up in the Pipeline

A

Back-Up in the Pipeline

A

Slowing of New Project Announcements

A

Slowing of New Project Announcements