| By Jim Butler, Hotel Lawyer | Author of www.HotelLawBlog.com

20 May 2007 - At the recent Meet the Money® conference on hotel

financing, Bobby Bowers, Senior Vice President at Smith Travel Research

(STR) provided an overview of the U.S. lodging industry for the 12 months

ending March 2007. The results were very interesting and bode well.

Here are his slides and what we think they mean.

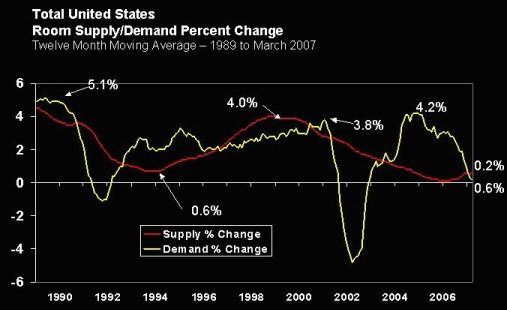

This supply-demand chart is a classic. It shows results since the late

1980s and dramatically illustrates how room demand growth accelerated from

late 2002 and has then gradually settled back down over the past few years,

while the growth in supply has been trending downward since the late 1990s

until it bottomed out 2006. Remember, these numbers are not the percentage

changes in the absolute amount of demand (measured by room nights) or supply

(measured by number of rooms), but reflect the percentage of change. The

crossover of supply and demand growth rates in 2007 is a significant event,

but does not, by itself, herald any impending doom, particularly given

the long period during which demand has been growing faster than supply.

This chart shows two of the most important components for measuring performance

in the hospitality industry: changes in occupancy and ADR. In evaluating

what the statistics mean, it may be useful to recall that the period from

1989 to 1993 marks one of the darkest periods in the hospitality industry

with thousands of hotel bankruptcies, and that the period from 1993 to

2000 marked some of the best years in the industry, the likes of which

still have not been equaled on an inflation-adjusted basis. Does the divergence

between occupancy and ADR that started in late 2004 have similarities to

the divergence that started in late 1993 or early 1994? How important is

it that occupancies are projected to actually decrease in 2007 as opposed

to merely moderating in 1994 through 1996? This is particularly interesting

when compared to RevPAR shown on the chart above.

This chart shows two of the most important components for measuring performance

in the hospitality industry: changes in occupancy and ADR. In evaluating

what the statistics mean, it may be useful to recall that the period from

1989 to 1993 marks one of the darkest periods in the hospitality industry

with thousands of hotel bankruptcies, and that the period from 1993 to

2000 marked some of the best years in the industry, the likes of which

still have not been equaled on an inflation-adjusted basis. Does the divergence

between occupancy and ADR that started in late 2004 have similarities to

the divergence that started in late 1993 or early 1994? How important is

it that occupancies are projected to actually decrease in 2007 as opposed

to merely moderating in 1994 through 1996? This is particularly interesting

when compared to RevPAR shown on the chart above.

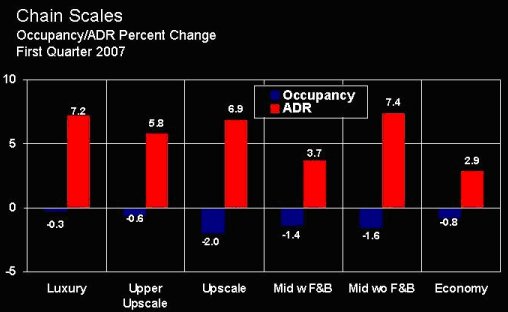

ADR showed growth in all segments -- some more than others -- and this

chart gives a fuller picture as to where the downtick in occupancy has

occurred.

ADR showed growth in all segments -- some more than others -- and this

chart gives a fuller picture as to where the downtick in occupancy has

occurred.

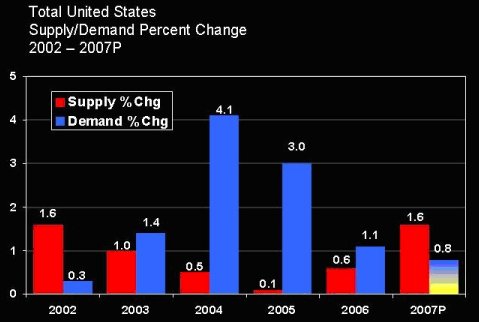

This bar chart shows supply-demand information for the past four years,

as well as projections for 2007. It illustrates the pent-up demand that

has been accumulating since 2003, and why the small crossover in supply

growth -- now exceeding demand growth -- may be of less concern than it

would under other circumstances.

This bar chart shows supply-demand information for the past four years,

as well as projections for 2007. It illustrates the pent-up demand that

has been accumulating since 2003, and why the small crossover in supply

growth -- now exceeding demand growth -- may be of less concern than it

would under other circumstances.

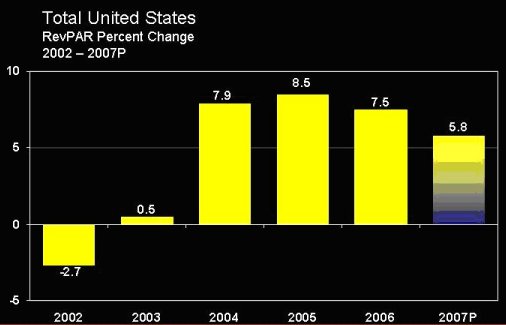

This chart dramatically shows all-time record levels of RevPAR increased

for 2004, 2005 and 2006. By any historic standards, a 5% RevPAR increase

is great! The question will be how long and how far RevPAR growth decreases

continue. There is still no cause for panic. There may be a wake-up call

around the corner, but the fundamentals are still so strong that this does

not signal an immediate problem.

This chart dramatically shows all-time record levels of RevPAR increased

for 2004, 2005 and 2006. By any historic standards, a 5% RevPAR increase

is great! The question will be how long and how far RevPAR growth decreases

continue. There is still no cause for panic. There may be a wake-up call

around the corner, but the fundamentals are still so strong that this does

not signal an immediate problem.

Predicting what the future holds . . .

The STR predictions were as follows:

-

Supply growth is accelerating

-

Demand growth is weak, but will accelerate

-

Construction costs remain a wild card Higher labor costs continue to be

a concern

-

Aggressive pricing will continue

-

Higher profits are expected

-

Continued RevPAR growth in 2007

While these trends did not seem to surprise any of the delegates at Meet

the Money®, having the tea leaves and a tea leaf reader provided valuable

insights. Thanks again, Bobby!

Please send me your thoughts at [email protected].

About the Author:

Jim Butler is one of the top hotel lawyers in the world.

GOOGLE �hotel lawyer� or �hotel mixed-use� or �condo hotel lawyer� and

you will see why. He devotes 100% of his practice to hospitality,

representing hotel owners, developers and lenders. Jim leads JMBM�s

Global Hospitality Group®�a team of 50 seasoned professionals with

more than $40 billion of hotel transactional experience, involving more

than 1,000 properties located around the globe. In the last 5 years

alone, they have brought their practical advice to more than 80 �hotel-enhanced

mixed-use� projects, a term Jim coined to fill a void in industry lexicon.

This term describes one of the hottest developments in real estate-where

hotels work together with shopping center, residential, office, retail,

spa and sports facility components to mutually enhance the entire project�s

excitement and success. Jim and his team are more than �just� great hotel

lawyers. They are also hospitality consultants and business advisors.

They are deal makers. They can help find the right operator or capital

provider. They know who to call and how to reach them. They are a major

gateway of hotel finance, facilitating the flow of capital with their legal

skill, hospitality industry knowledge and ability to find the right �fit�

for all parts of the capital stack. Because they are part of the

very fabric of the hotel industry, they are able to help clients identify

key business goals, assemble the right team, strategize the approach to

optimize value and then get the deal done. Jim is the author of the

Hotel Law Blog, www.HotelLawBlog.com. He can be reached at +1 310.201.3526

or [email protected]. |