| The popularity of spa facilities in hotels and resorts

has exploded in recent years. For many full-service and resort properties,

spas are as much a requirement as restaurants and meeting space.

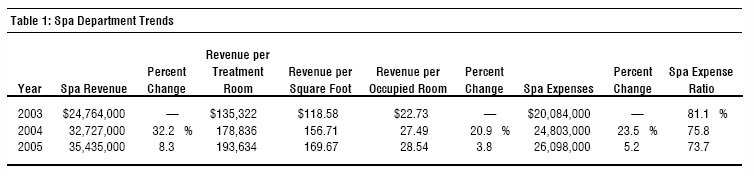

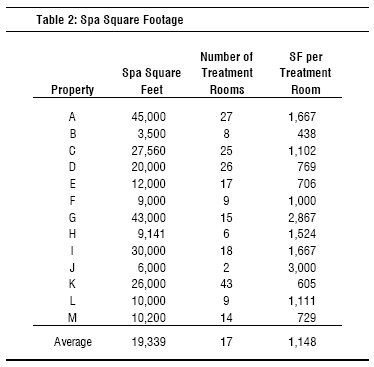

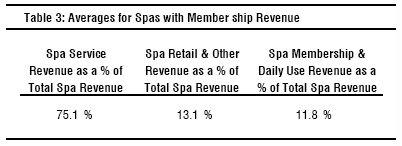

From an operational perspective, the success of a spa does affect a hotel�s financial performance, both as an operating department and as a marketing asset. Anecdotally, operators report the addition of an effectively planned spa can improve a property�s RevPAR (revenue per available room), allowing the property to sustain its competitive position. The following sets forth some financial statistics from spa operations and considers the economic impact of a spa on a hotel�s value. Spa Operating Performance Statistical data culled from spa operations in hotels and resorts indicates that spas are not only an expected guest amenity, but can add to the profitability of a hotel or resort. HVS International provides appraisal and consulting services for hotels and resorts around the world. For the purpose of this study, data was collected from spas in hotels located in urban and destination resort areas from coastal California to Orlando, Florida. The spas ranged from 3,500 square feet to 45,000 square feet, with 2 to 43 treatment rooms. Properties for which several years of spa operational performance was available were selected. The following data (Table 1) includes the composite results from 13 properties containing a total of over 4,600 guestrooms. The initial trend indicated by the data is that while revenue increased during the three years analyzed, the greatest impact on the departmental profitability is improved operational efficiency. On an aggregate basis, spa revenues increased at a faster pace than expenses, resulting in significant improvements in departmental profitability. The spa comparables indicate an average expense ratio of roundly 73% in 2005, down from an average of roundly 81% in 2003, as a result of greater revenues and good expense control.  As with other hotel operating departments such as food and beverage, spa operations illustrate a wide range of results from hotel to hotel. Factors such as property location, spa design and operating structure, importance of the spa to the hotel�s identity, spa size, hotel market position, and competition from other amenities such as golf courses all affect spa revenue potential. The data from the sample of 13 hotels, which ranged in size from 99 to 1,042 rooms, indicates that spa revenue does not show consistent correlation to any particular property attribute. For some hotels, spa revenue per available room grew faster than RevPAR. Whether evaluating an existing spa operation or planning for a new facility, an analysis of spa performance is highly dependent on the market orientation of the hotel property and the physical and operational attributes of the spa. In our survey, the existing spas averaged 19,300 square feet. Table 2 shows the size distribution of the sample.  Spa Revenue Analysis Based on the data analyzed, spa revenues are divided into three main categories: spa service revenue, spa retail and other revenue, and spa membership and daily-use revenue. The majority of spa revenue comes from spa services such as massages, facials, nail services, and so forth. Depending on the facility program of the spa, spa service revenue ranged from 48.2% to 93.1% of total spa revenue. All of the spas sampled also included retail revenue from spa merchandise and products. For the properties included in the sample, spa retail revenue contributed 6.4% to 18.5% of total spa revenue. Most of the spas also generate revenue from spa membership and daily-use revenue, which include fees to use the general spa or fitness facilities. Membership and day-use revenue can be substantial depending on the exercise facilities and the hotel or resort�s location relative to a large residential population base. Many hotels and resorts actively promote a local membership program for spa facility use. Typically, those hotels that include this program offer extensive workout facilities as part of the spa so the spa is an alternative to a local health club. If the hotel or resort has the right facilities and a supportive surrounding residential population, the revenue contribution of a membership program can be substantial. Because the membership contribution can be a major revenue source for

a spa operation, revenue contribution ratios for spas with membership and

daily-fee programs were compared to those for spas without such programs.

For spas that include spa membership and/or daily-use revenue, these revenues

ranged from 1.6% up to 44.5% of total spa revenue, at an average of 13.1%.

Spas that include spa membership revenue had spa service revenues ranging

from 48.2% to 90.2%, at an average of 75.1%. These spas had spa retail

and other revenues ranging from 1.6% to 44.5%, at an average of 11.8%.

, .  While the revenue composition for the spas varied, the data does not reveal a correlation between overall department profitability and the revenue mix. Net Operating Income and Feasibility Analysis A spa can have a number of different impacts on a hotel or resort operation. Depending on the investor�s objective and the market position of the property, a spa can be included to help sustain a property�s RevPAR, and/or to improve its RevPAR and competitive positioning, and/or to enhance net operating income. Spa facilities do not always contribute significantly to a property�s net operating income, but, at the very least, the department should not cause a reduction in overall property profitability. To illustrate the financial impact of a spa department on overall hotel performance, we compared the hypothetical operating statements of a full-service property with a spa to that of a base case scenario without a spa operation, and that of a spa generating a reasonable return on the spa development cost. A return on investment analysis was then performed to demonstrate the potential return on the addition of a spa facility. Table 5 sets forth three operating statements. The first statement shows the profit and loss data for the base case scenario, a property without a spa. The second statement includes a spa facility where the expense level of the department results in the same net operating income as the base case. The third statement shows a spa with an expense level that provides a net operating income for an acceptable return on the spa�s development cost.  All things being equal, the spa, in this hypothetical scenario, has to operate at a modest departmental profitability level (92.9%) for the property to achieve the same overall net operating income as that of the facility without a spa (base case). Increased operational efficiencies would result in positive increases to the net operating income dollars compared to the facility without a spa. This would indicate that running spa departmental expense margins in line with the averages set forth earlier would contribute significantly to the bottom line. But even with the average expense level, the spa department would not generate enough incremental income to warrant its development. To estimate the incremental income necessary to support the spa development in this hypothetical scenario, a market rate of return was applied to an estimated spa build-out cost. Based on published articles, the cost of building a spa in 2006 dollars is estimated at roundly $650 per square foot. Assuming an 18,000-square-foot spa, the turnkey development cost would be roundly $11,700,000. If the investor required an 8.0% return on that cost, the incremental net operating income resulting from the spa operation would have to be $936,000. The total hotel net operating income of the base case in our hypothetical property is $10,222,000. The incremental spa income would increase the net operating income to $11,158,000. As illustrated in the preceding chart, the �Positive Spa ROI� shows that the spa department would have to operate at an expense level of 70.3%, slightly below the average expense ratio from 2005, to generate an 8.0% return on the spa investment. Table 6 shows the assumptions for this analysis.  About the Authors: Elaine Sahlins is Senior Vice President with HVS International�s San Francisco, California office. She holds an undergraduate degree from Barnard College, Columbia University in New York City and an MPS degree in Hotel Administration from Cornell University. After graduating from Cornell she worked for VMS Realty in Chicago analyzing hotel investments, and then went on to join Security Pacific in San Francisco, which was subsequently acquired by Bank of America. She joined HVS International in 1987 as a Director in the San Francisco office. Ms. Sahlins also, with Suzanne Mellen, directs HVS Gaming Services. Amy Peterson is an Intern with HVS International�s San Francisco, California office. She is currently studying Hospitality Management and Finance at the University of San Francisco. |