|

|

|

|

|

|

|

|

|

| Atlanta, Ga., April 10, 2007 � U.S. hotel owners continue to ride the

wave of prosperity that has characterized the lodging industry since mid-2003.

Twelve successive quarters of year-over-year demand growth, fueled by an

expanding economy, has attracted a flow of debt and equity capital that

has driven property values, and transaction activity, back to pre-9/11

levels in most markets. Of all the factors that have contributed

to the robust health of the lodging industry, none has been more important

than the unbalanced relationship between the above-average growth of demand

and the minimal levels of new hotel construction. Now, however, according

to a new study released by PKF Hospitality Research (PKF-HR), there is

growing evidence that the imbalance may be coming to an end.

High Prices Begin to Impact Travel Since 2003, demand has increased by 10.2 percent, while the net change in supply has been almost flat, which in turn has placed pricing power firmly in the hands of hotel managers. According to Smith Travel Research (STR), the average cost of renting a hotel room in the top 50 U.S. cities has increased by 23.0 percent during this time period. Consumers in many markets have begun to say �Enough!� and hotel occupancies have started to moderate as a result. STR also reports that annual demand levels in 12 of the top 24 U.S. markets (New Orleans is excluded from this list) actually declined in 2006. This trend has carried over into 2007, with first quarter industry-wide demand levels below their 2006 amounts. So long as hotel construction volumes remain at historic lows, property owners who have been enjoying healthy profits had little to fear. However, PKF-HR�s recently published study, The Hotel Supply Conundrum, which provides new insights to the current state of hotel development activity, suggests that the industry may be in for a wave of hotel construction. In the report (available at www.pkfc.com/supplyconundrum), author Dr. Jack Corgel of Cornell University and Senior Advisor to PKF Hospitality Research, focuses on the variety of factors that have made the economic justification of lodging development extraordinarily difficult. A unique combination of events led to dramatic increases in construction costs in recent years. High GDP growth rates in China and India pushed up prices of raw materials such as cement and metals. The expanding housing market also caused upward pressure on the prices of developable land, construction labor and materials. Add to the mix the large speculative premium that resulted from the rush of hedge funds into the commodities markets, and the developers� nightmare became complete. Mark Woodworth, president of PKF-HR, notes that a select group of upscale and luxury developers have been able to close the gap between market values and replacement costs by incorporating residential units into their hotels. �We have also seen limited service hotel development in secondary and tertiary market areas where cost pressures have been less severe,� Woodworth noted. But a review of the volume and period-to-period movement within the development pipeline tells the bigger story. The Flow is a Trickle The last time the U.S. lodging industry experienced a comparable period

of strong demand growth with limited new construction was 1994 through

1996. This was followed by robust levels of domestic construction

activity through the last half of the 1990�s. During this period,

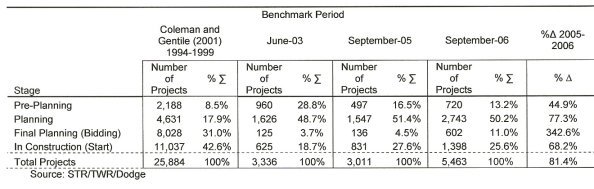

according to data compiled by STR/Torto Wheaton Research and Dodge (STR/TWR/Dodge

- see accompanying Table 1), total projects in the development pipeline

averaged approximately 4,300 per year. On average, over 70 percent

of these projects were either under construction (42.6 percent) or in the

final planning (or bidding) stage (31.0 percent). By 2005, deteriorating

industry fundamentals, followed by the aforementioned run-up in development

costs, resulted in the decline of the total number of projects in the pipeline

to approximately 3,000, with only 32.1 percent in the under-construction

or final-planning stages.

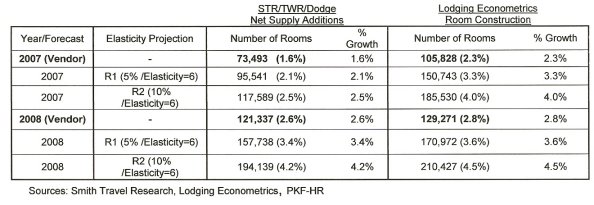

STR/TWR/Dodge Construction Pipeline (Number of Projects)  Rapidly escalating market values caused the total number of projects in the development pipeline to grow by 81 percent from 2005 to 2006. The 5,463 projects identified by STR/TWR/Dodge in their September report were well above the 1990�s average of 4,300. Not surprisingly, the number of projects that entered the final-planning or under-construction stages more than doubled in 2006. Is the Dam About to Burst? �It is clear from our research that many of the factors that have caused the dramatic escalation in hotel replacement costs have begun to subside,� noted Dr. Corgel. �Our clients have yet to report noticeable declines in construction prices,� Woodworth stated, �but there is an increasingly clear level of optimism that the cost increases realized in recent years are now a thing of the past.� Logically, if construction costs start to decline, the volume of hotel construction activity will likely increase. While no empirical research addressing the cost elasticity of lodging supply exists, some insights can be gained from a review of housing economics literature. Using this as a guide, Dr. Corgel hypothesizes that a 5 percent decline in development costs may cause a 30 percent increase in the volume of actual construction activity in the pipeline. Similarly, a 10 percent decline in development costs may cause a 60 percent increase in activity levels. Using data from both STR/TWR/Dodge and Lodging Econometrics, hotel construction levels could escalate to levels (rounded) between 150,000 and 185,000 this year and to more than 200,000 rooms in 2008 (see Table 2). �To lend perspective to these estimates, the level of hotel construction activity in the decade of the 1990�s peaked at 150,000 units in 1999,� Woodworth stated. Table 2

Where is Supply Likely to Grow the Most? With conditions facing hotel developers in 2007 moving in a more favorable direction, which markets will likely experience the greatest levels of construction activity? In his report, Dr. Corgel analyzed the level of supply growth that has occurred between 2002 and 2006 in the 50 largest hotel markets, with a focus on the key performance metrics that led to above average levels of construction activity during this period. Two factors were typically present in the vast majority of these high supply growth cities: the occupancy level in 2000, and the magnitude of annual average daily rate growth realized during the last half of the 1990�s, which was well above long term averages. �Using history as a guide,� Woodworth noted, �hotel development activity

should accelerate in markets such as Charlotte, Ft. Worth, Houston, Nashville,

Phoenix and Tampa.� While the availability of both land and appropriate

lodging brands remain formidable obstacles in many of these markets, the

signs are becoming clear that a significant increase in hotel construction

levels may very well be looming on the horizon.

Historic and Possible Future High Supply Growth Markets .

Source: PKF Hospitality Research This outlook, combined with softening demand conditions in many key U.S. hotel markets, will cause industry profit growth to diminish and bring an end to the dramatic run-up in property values that hotel owners have enjoyed since the start of this decade. To receive a copy of the Hotel Supply Conundrum, please visit the firm�s website at www.pkfc.com/supplyconundrum. PKF Hospitality Research (PKF-HR), headquartered in Atlanta, is the research affiliate of PKF Consulting, a consulting and real estate firm specializing in the hospitality industry. PKF Consulting has offices in Boston, New York, Philadelphia, Washington DC, Atlanta, Indianapolis, Houston, Dallas, Bozeman, Los Angeles, and San Francisco. |

| Contact:

R. Mark Woodworth

|

| Also See: | New Lodging Supply Growth in Check / Robert Mandelbaum / February 2006 |

| Hotel Construction Signs Along the Road to Recovery; Measuring Hotel Developer Intent / R. Mark Woodworth and Robert Mandelbaum / January 2005 |

.