|

|

|

|

|

|

|

|

Still Positive Despite Peak-of-Cycle Behavior |

| ATLANTA, GA., May 30, 2006 -- Hard statistical evidence gleaned from

interviews of U.S. hotel investors and lenders conducted in the 2006 first

half suggest that domestic hotel markets are fully recovered from the damaging

economic and horrendous social events early in the decade. Furthermore,

there is increasing evidence in the hotel real estate investment markets

that the industry may be closer to the peak of this cycle than the beginning.

These observations come from an analysis of data collected in connection

with the recently released 2006 edition of Hospitality Investment Survey

published recently by PKF Hospitality Research (PKF-HR), an affiliate of

PKF Consulting.

�Capital suppliers to the industry show no signs of altitude sickness

as the measures of financial performance evidence peak-of-the-cycle behavior,�

said Scott Smith MAI, vice president in the Atlanta office of PKF Consulting.

�Purchase and lending criteria used for this year�s lodging transactions

indicate a community of buyers willing to pay higher prices and financiers

offering liberal lending requirements. Virtually all measures are

equal to, or more positive than, those used to purchase properties during

the early stages of the 1990s growth cycle.�

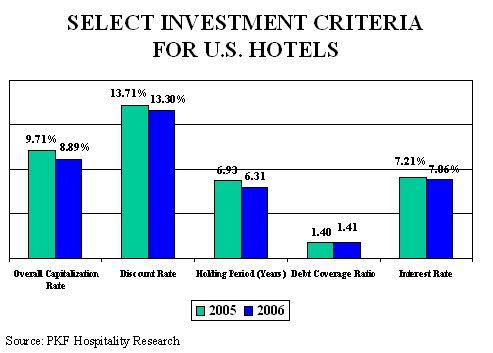

�Fortunately, the optimism is justified by solid industry fundamentals, as opposed to unsupported euphoria that we saw at the top of the last cycle,� observed Dr. John B. (Jack) Corgel Ph.D., the Robert C. Baker professor of Real Estate at the Cornell University School of Hotel Administration and consultant to PKF-HR. Hotel Outlook, a lodging industry forecast model designed by PKF-HR and Torto Wheaton Research, projects a continuation of strong growth for the U.S. lodging industry through 2006. By year-end, hotel RevPAR in 52 of the largest U.S. markets is forecast to rise 6.3 percent, the result of a 1.5 percent gain in occupancy and a 4.7 percent increase in average daily rates. This level of RevPAR growth should generate a 14.9 percent increase in profits for the typical U.S. property. The 2006 Hospitality Investment Survey presents the results from surveys of active hotel owners, equity investors, and debt providers about the criteria used for hotel transactions that have, or will occur during the year. The six-page report contains tables that show the current and historical averages of a dozen critical investment measurements, including capitalization rates and mortgage terms. Data are broken out for full-service and limited-service properties. In addition, the report contains topical essays that address the current investment and development climates. The Capital Continues to Flow Respondents to the 2006 Hospitality Investment Survey indicated that there continues to be an ample supply of money available for hotel lending and equity investment. �The combination of still modest interest rates by historical standards and rising cash flows keeps real estate in the spotlight. Without the friction of lease contracts and fears of increasing inflation, many non-traditional hotel investors view hotels as a favorable asset class in this environment,� Smith explained. Added to the mix is a sizeable population of hotel owners now willing

to sell. These investors held hotel properties beyond their expected holding

periods and find the current pricing of hotel property very satisfactory

for meeting their yield requirements. �With both buyers and sellers being

motivated to execute transactions, and financing readily available, we

expect that the hotel transaction market will continue to be active,� Smith

concluded.

Low Risk Leads To Attractive Lending Criteria Given the bullish performance forecasts for U.S. hotels, all parties involved perceive less risk in hotel investments, compared to both historical measures and other forms of real estate. This optimism has resulted in a relaxation of both investment return requirements and lending restrictions. �Yields, or IRRs, for hotels nearly match the historical low from this survey in 1998,� Corgel noted. �More importantly, the spread between the overall capitalization rate and the discount rate continues to hover in the 4 to 6 percent range, suggesting that owner expectations for growth in net operating income are exceeding recent historical performance.� Despite fears of rising interest rates and Federal Reserve actions, the cost of financing remains favorable for investment. �Loan-to-value ratios declined slightly from the 70 percent level in 2005 and debt coverage ratios continue to favor borrowers as they seek more leverage. These terms indicate that lenders feel adequately protected from a recurrence of delinquency and default risk experienced in 2002 and 2003,� Corgel observed. Full Service Is King! Historically, investors more highly value cash flows of hotels in the full-service segment than limited-service hotels, and this situation exists today. �With higher barriers to entry for full-service hotel development, investors see greater profit potential for this segment, and for longer periods,� said Thomas E. Callahan CPA, CRE, MAI, San Francisco-based chief executive officer of the western region of PKF. �Well-branded, full-service hotels in good condition located in major metropolitan or resort locations get the undivided attention of investors.� Lenders also are showing a preference for full-service hotels. �Differences in default risk are shown by the higher interest rates assessed to limited-service mortgages, as opposed to full-service loans,� Callahan noted. �Somewhat surprisingly, longer loan terms, slightly higher loan-to-value ratios, and lower debt coverage ratios can be obtained for limited-service properties.� Copies of the 2006 Hospitality Investment Survey are available for

purchase

PKF Hospitality Research (PKF-HR), headquartered in Atlanta, is the research affiliate of PKF Consulting, a consulting and real estate firm specializing in the hospitality industry. PKF Consulting has offices in New York, Philadelphia, Washington DC, Atlanta, Indianapolis, Houston, Dallas, Los Angeles, and San Francisco. |

| Contact:

Scott Smith MAI

|

| Also See: | Hotel Real Estate is Alive in 2005 / Scott Smith, MAI / June 2005 |

| Rampant Optimism in U.S. Hotel Investment Arena / PKF / June 2005 |