|

|

|

|

|

|

|

|

|

|

| by Robert Mandelbaum, January 2006

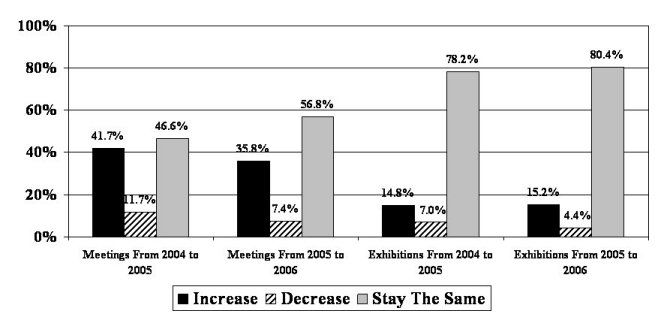

Like other businesses, the meetings industry operates over time on a cyclical basis. There are years of industry recession when the number of events and attendees decline. Conversely, there are years of recovery and expansion when both attendance and event counts rise. The U.S. meetings market, like the domestic hotel industry, has just completed all the phases of a business cycle. From peak performance in the late 1990s, to contraction from 2001 to 2003, to recovery and growth in 2004 and 2005, the U.S. meetings market appears to have reached a period of stabilized performance for the next few years. These are the findings from a survey of meeting planners recently conducted by PKF Hospitality Research (PKF-HR) on behalf of Convention South magazine. Although the survey questions focused on meetings planned for the Southeast and South Central regions of the U.S., responses were received from 163 meeting planners located all across the nation. The majority of the respondents were association planners (55.5%), followed by corporate planners (21.0%), independent planners (13.0%), and those that classified themselves as �other� (10.5%). On average, each of the 163 meeting planners was responsible for 27.1 meetings and 3.0 exhibitions/trade shows in 2005. Indicators Of Stability When asked about the number of events they were planning for 2006, 56.8

percent of the planners in our survey indicated that the volume of meetings

would be the same as 2005. An even greater percentage of planners

(80.4%) thought their 2006 exhibition/trade show activity would equal that

worked on in 2005.

Percent of Meeting Planners

Source: Convention South, PKF Hospitality Research Not only will the number of events planned for 2006 be roughly equal to 2005 levels, but the duration and geographic nature of the events will likely be that same. More than three-quarters of the planners (77.2%) believe the duration of their 2006 events will last the same number of days as in 2005. In addition, 73.3 percent of the planners think that the geographic scope of the events will be the same in 2006 as it was in 2005. For reference purposes, the 2005 events for our survey sample were fairly evenly distributed between state, regional, and national meetings and exhibitions. Few of our respondents organize locally oriented events for their association, corporation, or clients. It seams that the lead time to book events has stabilized as well. Our survey respondents noted that, in 2005, they are selecting the site for their largest events 20 months in advance. This is the same number of lead-time months as reported in 2004. Given the outlook for increasing hotel occupancy levels the next few years, it may be that 20 months is the maximum time hotels are allowing planners to tie up meeting space and guest rooms. Event planners� perception of service seems to have remained stable as well. When asked how what they felt about the service they have received at their meeting sites in 2005, 60.9 percent of the planners believe that service levels have remained the same as they were in 2004. Twenty-three percent (23.0%) of the survey sample believed service levels improved in 2005; however, 16.1% were less satisfied with the service they received during the year. While the volume, duration, and scope of the events will remain stable

in 2006, we noted a recent trend towards greater-than-expected attendance

at each event. Slightly over half (50.9%) of the planners surveyed

felt the attendance at their 2005 meetings was equal to what they expected

it to be. However, 34.6 percent of the survey sample enjoyed meeting

attendance figures that exceeded their expectations. This pleasant

surprise showed an increase from 2004, when 22.8 percent of planners found

their expectations had been exceeded.

Planner Expectations

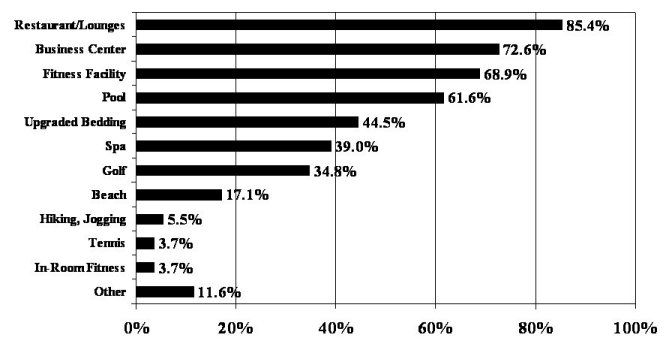

Source: Convention South, PKF Hospitality Research Areas Of Growth The good news for U.S. hoteliers is that just over half (52.2%) of the meeting planners surveyed believe that their per-delegate expenditures will increase in 2006 compared to 2005. This comes off a year (2005) when only 43.0% of the respondents spent more per delegate than they did in 2004. However, it should be noted that meeting planners do not have an open ended-budget for 2006. Planners who are feeling economic pressure from their bosses or clients are being asked to make cuts in their food and beverage (45.7%), off-site events (37.8%), audio/visual (36.6%), and rooms (24.4%) budgets for 2006. Another way meeting planners are being asked to control costs is to avoid large metropolitan markets. Thirty-eighty percent (38.0%) of the planners reported pressure from their sponsoring organizations to consider second- or third-tier cities in 2005. This number is up from 35.3 percent in 2004 and 27.7 percent in 2003. Wants And Desires The meeting planners were asked to rank the importance of certain technology-related amenities in the site selection process. In the meeting room, LCD projectors are virtually required by almost all meeting planners. High-speed Internet access (HSIA) ranked as somewhat less important, along with WiFi access. Videoconferencing and downlink capability were frequently deemed as �unimportant�. In the guestroom, over half of our survey respondents felt that HSIA was very important and essential for selection of a hotel. In-room WiFi access ranked as �somewhat important�, followed by HiTech entertainment which was believed to be �unimportant� in the hotel selection process. As for the wishes of the meeting attendees, 85.4 percent of the planners said delegates want on-site hotel food and beverage outlets. The next highest rated attendee requests call for business centers (72.6%), fitness facilities (68.9%), and pools (61.6%). This is consistent with recent studies verifying that travelers want to be productive and healthy while on the road. Two hotel amenities of growing importance for meeting attendees are

upgraded bedding (44.5%) and spas (39.0%). Given the recent moves

of most major chains to add enhanced beds and spa facilities to their properties,

hotel companies are clearly paying attention to the feedback received from

meeting planners and guests.

Percent of Respondents

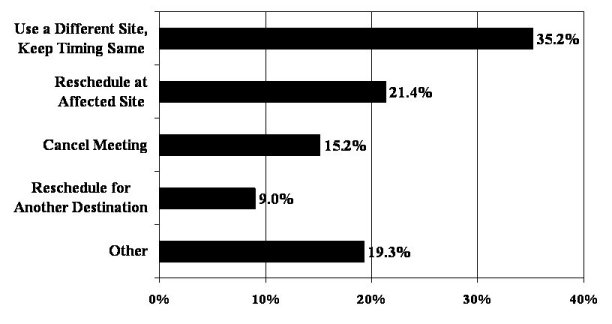

Source: Convention South, PKF Hospitality Research Current Events Given recent events in the Southeast and South Central area of the U.S., we asked the meeting planners how the increase in hurricane activity has affected the meetings they plan for the region. The majority of the planners polled (69.4%) stated that the hurricanes have not affected the timing of the events they hold in the South at all. Of those that have been influenced, 12.2% said they would just move the timing of their meetings to outside of hurricane season. No one stated that they would avoid meetings in the South all together because of the fear of hurricanes. What if a hurricane, or another Act of God, were to force the displacement of a meeting from its intended site? Most frequently, meeting planners would keep the same timing of the meeting and move the event to a different site (35.2%), or they would reschedule the meeting for the same site at a later date (21.4%). Some planners (15.2%) would cancel the meeting outright, while others (9.0%) would reschedule the meeting for another time and location. When asked if rising gas prices would have a negative effect on meeting

attendance, the planners were evenly split. Half of the sample thought

event attendance would not be negatively affected, while the remaining

planners believed their attendance would fall if gas prices continued to

rise.

Percent of Respondents

Source: Convention South, PKF Hospitality Research . For event planners, stabilization in the meetings market could provide some degree of normalization in their lives. On the one hand, planners do not have to worry about their job security due to budget cuts. On the other hand, coordinating an overload of events and searching for available meeting space should not be too burdensome. For hotel managers, it appears to be that awkward time when the pendulum

of negotiating leverage is stuck in the middle. Yes, hotel occupancy

levels are rising and sales managers should be able to negotiate favorable

meeting contract terms. However, the meeting planners are just as

ready to move their business to a second-tier city, or cut back on their

food and beverage, in order to retain the stability of their meeting budgets.

Robert Mandelbaum is the Director of Research Information Services for PKF Hospitality Research. Special thanks to Kristen McIntosh, editor of Conventions South, for sponsoring the survey. |

| Contact:

Robert Mandelbaum

|

| Also See: | The Evolving Relationship Between Hotel Sales Managers and Meeting Planners / What's in the Minds of Meeting Planners Today? / Robert Mandelbaum / January 2004 |

| Understanding the Recovery Occurring in the Meeting�s Market; Surveying the Meeting Planners / Robert Mandelbaum / December 2004 | |

| Understanding Meeting Planners / Patrick Quek / PKF / March 2001 | |

| Survey Shows Meeting Planners Not Ready to Flex Their Muscles / Patrick Quek / PKF / March 2000 |