|

|

|

|

|

|

|

|

|

| by: Robert Mandelbaum, February 2006

Changes in supply and demand patterns are the two factors that cause shifts in the hotel industry cycle. Currently, most hotel owners, operators, and analysts are bullish with regards to the short- and intermediate-term outlooks for the lodging industry. On the demand side, occupied room nights continue to climb despite rising gas prices and multiple hurricanes. Barring an unforeseen catastrophic event, our PKF Consulting/Torto Wheaton Research Fall 2005 Hotel Outlook forecast calls for growth in demand each year from 2005 through 2008 at a 2.5 percent compound annual growth rate. What is foreseeable with a fairly high degree of certainty is the relative lack of new supply growth in the next few years. Given the lead-time needed to build hotels, projections of supply growth are somewhat predictable for a period of at least three years. Despite continued economic growth, rising demand, and growing room rates, the supply side of the performance equation appears to be in check from now through 2008. The Fall 2005 Hotel Outlook forecast shows a compound annual growth rate for supply of 1.9 percent from 2004 through 2008. For comparison purposes, climbing out of the industry recession of the early 1990s, lodging supply grew at a compound annual rate of 3.9 percent from 1994 through 1998. It is the relative lack of new lodging supply projected to come on line during the next years that has operators and owners of existing hotels most happy. Why is hotel construction slow given the positive outlook for hotel demand and average daily room rates? One theory is that in most markets, it is still cheaper to purchase an operating hotel than build a new one. And, this is not because hotel values are depressed. We are currently in a unique situation when the industry is approaching a period of peak performance, yet the rise in development costs is outpacing the growth in hotel values. To gain a better understanding of current market conditions, we analyzed the factors that have driven historic development costs and values. Our Analysis In addition to our firm�s proprietary Trends in the Hotel Industry database,

we rely on data from the following sources to examine the relationship

between hotel values and development costs: Smith Travel Research

(STR), Real Estate Research Corporation (RERC), Bureau of Labor Statistics

(BLS), and the U.S. Department of Agriculture (USDA). Due to the

availability of certain data, our analysis is limited to full-service hotels.

To estimate historical changes in value, we utilized profit data from the

Trends database and capitalization rates from RERC. A three-year

weighted average of advanced profit data is used to simulate the �forward

looking� nature of hotel buyers and sellers. Construction cost data

from the BLS, combined with land value information from the USDA, measure

annual changes in development costs. Changes in full-service lodging

supply for major urban markets come from STR.

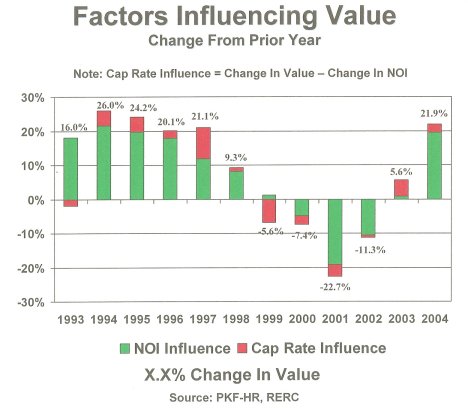

Profits and Value The price a buyer is willing to pay for a hotel is influenced by two factors � the income (NOI) generated by the property, and the prevailing capitalization (cap) rate that reflects the perceived risk of the income going forward. From 1993 through 2004, our analysis shows that changes in NOI had the most impact on changes in value during all but two years. The two years were 1999, the first year that hotel values declined during that decade�s market recovery, and 2003, the first year that values showed an increase coming out of the 2001 recession. In 1999, despite current gains in NOI, investors apparently perceived an imminent downturn in market conditions, thus precipitating a strong increase in the cap rate. In 2003, optimistic buyers foresaw a strong recovery, cap rates declined significantly, and values surged despite declining NOIs during that year. Strong profit growth appears to have had the greatest influence on rising

values during the heart of recovery cycles. From 1994 through 1997,

and again in 2004, NOI gains were the dominant factor causing values to

rise. In each of these years, U.S. hotels recorded double-digit NOI

growth, combined with declining cap rates. Short-term, and long-term,

optimism combined for soaring values in excess of 20 percent during these

years of recovery.

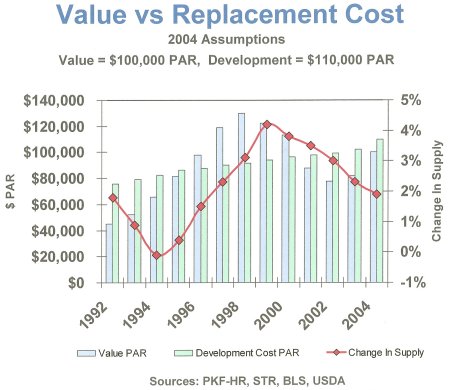

Replacement Costs Typically, when the lodging industry is in the midst of a strong recovery, hotel values soar to such a point that it becomes cheaper to build a new hotel than to buy an existing one. Such was the case during the recovery from the 1991 industry recession. From 1992 through 1995, hotel values lagged behind replacement cost. A surge in hotel construction that started in 1996 resulted in strong (greater than 3 percent) increases in supply from 1999 through 2002. With hotel values on the rise once again in recent years, why is the current outlook for new development suppressed? The main reason is our belief that hotel development costs will continue to raise the bar that hotel values must reach to make projects feasible. The driving force behind the rise in hotel development cost is the recent surge in both construction and land costs. Based on data from the BLS, construction costs in the United States rose 8.3 percent in 2004. This compares to a compound annual average of just 1.7 percent from 1992 through 2003. Similarly, land costs are currently growing above long-term averages. In 2004, land prices soared 7.0 percent extending beyond the 5.3 percent annual average from 1992 through 2003. Compounding the high land cost issue is the difficulty developers are having with market entitlements (i.e., land use regulatory approval) in some markets. Based on conversations with our clients, as well as analysis of recent construction budgets, we believe the sharp rise in development costs and presence of strict regulatory obstacles will continue for the next few years. Replacement To Outpace Value Looking forward, we expect to see hotel values rise, but continue to lag behind the growth in development costs. On the value side, our projections call for NOI growth to continue, but at a slower pace than the strong 2003 through 2005 recovery period. We expect to see stabilization in the decline of cap rates largely due to rising interest rates. The combination of these two factors will result in moderate growth in property values. Conversely, look for construction and land costs to rise above long-term average growth rates. Consequently, replacement costs will stay above values, thus mitigating supply growth. Given the outlook for limited supply growth, the industry is crossing its fingers that we don�t experience a catastrophic event that will cause dramatic declines in demand. |

| Contact:

Robert Mandelbaum

|

| Also See: | Hotel Construction Signs Along the Road to Recovery; Measuring Hotel Developer Intent / R. Mark Woodworth and Robert Mandelbaum / January 2005 |

| Fewer Hotels Deficient on Interest Payments; Low Interest Rates, Refinancing, and Rising Profits Are Major Factors / PKF Study / July 2005 | |

| The Hotel Terminal Cap Rate Delimma / PKF / August 2005 |