|

. INNvestment Canada First Quarter 2005 |

|

|

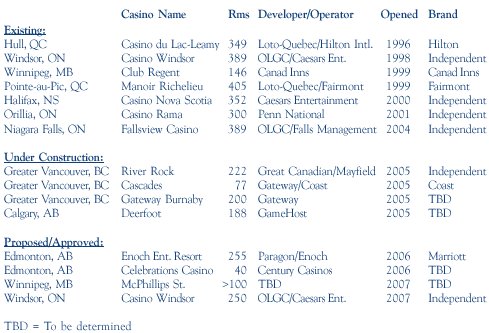

Q1 2005 Transaction Summary Written by Lyle Hall, Hall Hospitality Advisors Casino gaming has been one of the fastest growing entertainment products of the past decade not only in Canada but also in the United States and internationally. More than seventy five casinos and �racinos� (i.e., slot machines at racetracks) currently operate in Canada with several others either under construction or renovation/expansion. Casino gaming (including racinos but excluding all other forms of gaming such as lotteries and bingo) generated $6.2 billion in Canada last year, an increase of more than 50% in just the last four years. Consumer acceptance of gaming as an entertainment alternative has seen sustained supply growth. By the end of 2005, all Canadian provinces except Newfoundland and New Brunswick will offer some form of casino or racino product. But as gaming supply continues to grow so does the need to differentiate one gaming site from another, a process often addressed through the addition of non-gaming amenities such as food and beverage, retail and entertainment offerings and in a growing number of instances, hotels. New hotel supply in Canada has increased at a relatively modest rate since the mid/late 1990s, on a national average not much more than 2% per annum. However, the number of hotels built in association with, or to support a casino, is growing. Since 1996, some seven casino hotels offering more than 2,300 rooms have opened in a variety of urban and resort settings. Another four hotels with 680 rooms are under construction while at least four others (600 plus rooms) are in the planning and/ or approval stage. And, of course, these numbers do not include new rooms in markets like Niagara Falls, that were built to support the influx of gaming visitors. The situation in the United States is, arguably, even more aggressive. Leaving aside established overnight gaming destinations like Las Vegas, Atlantic City and the Gulf Coast of Mississippi, hotel accommodation is rapidly becoming �table stakes� at new and existing casinos everywhere from urban destinations to First Nations� on-reserve casinos and even to one-off racinos. In fact, racino and more remote casino projects have been among the most aggressive in the development of non-gaming amenities such as Dover Downs, Delaware (232 rooms and 25,000 sq ft meeting/ entertainment centre), Mountaineer Park, West Virginia (2 hotels with 360 rooms and entertainment centre) and Hollywood Casino Shreveport, Louisiana (450 rooms, four restaurants and meeting space). Why the interest in such amenities, particularly hotels? Simply put, hotels create an ability to extend the marketing reach of the casino beyond the resident population. Packaged with food, beverage and/or entertainment offerings a casino visit can be transformed into a weekend or other short-term getaway. Typically, the more remote the casino location and/or the more reliant on visitors from outside the market area, the more likely is a casino to offer hotel accommodation (either on site, or in conjunction with arms-length providers). In those jurisdictions where regulations permit, the casino operator can use the offer of free overnight accommodation as part of the marketing package to entice regular gamblers back to the casino. The practice of �comping� rooms (as well as meals and entertainment) is an established casino marketing approach but the degree to which it is permitted in Canada varies considerably by jurisdiction. The interest by casino operators in developing or co-locating with a hotel is typically a function of several factors, including the permissibility of comping. Where comping is permitted, the casino operator will want more control of the hotel and other non-gaming assets, as the �revenue line� of these amenities is essentially the �marketing expense� line of the casino. This doesn�t necessarily imply a lack of opportunity for third-party management, but does greatly reduce the prospect of shared profitability. Other factors include:

In British Columbia, Alberta and Nova Scotia private-sector companies

are contracted to the Crown Agent to build, finance and operate casino/racino

venues as well as any non-gaming amenities. In these jurisdictions, a �commission�

on gaming revenue is paid by the province, to compensate for capital and

operating costs. Ontario is a hybrid where the private sector provides

management services in some cases (i.e., Niagara Falls, Rama, Windsor,

Great Blue Heron) and the Crown Agent in others (i.e., slots at racetracks

and charity casinos).

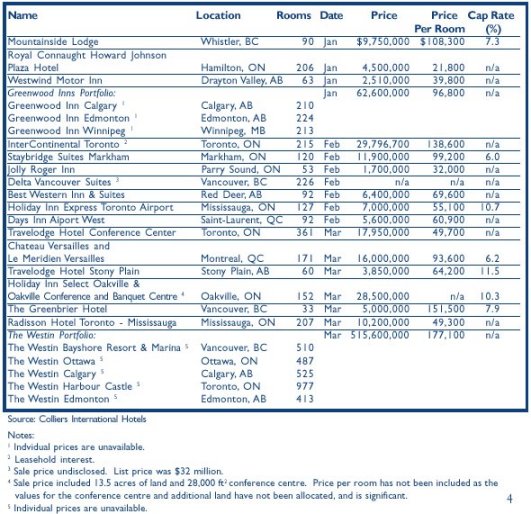

One overarching consideration is the degree to which casinos are used to enhance tourism and visitation within a given community. Casino development based on the potential to increase tourism, particularly overnight tourism, is becoming a norm in many North American jurisdictions. As pressures build to increase casino supply, we can expect to see more tourism-based justification in the future. And, with markets like Niagara Falls providing good examples of the positive impact a properly executed, full-service casino can have on building tourism demand, such justification can be warranted. In Canada, future development opportunities are most pronounced in those jurisdictions where private service providers are involved in delivering gaming product. A sure bet for the future though, is continued growth of gaming supply supported by a range of non-gaming amenities such as hotels, as interest in this entertainment alternative swells. There was tremendous hotel transaction activity in first quarter 2005. While the number of trades increased from 12 (Q1 2004) to 24 (Q1 2005), the most notable change was volume, increasing ten-fold from approximately $75 million to some $771 million (including strategic acquisitions). In fact, Q1 2005 volume more than doubled the total transaction volume reported in 2004 of $372 million. When strategic acquisitions are removed, the average price per room increased by 69.2% from $46,200 in Q1 2004 to $78,200 in Q1 2005. With more than one-third of the hotels trading in excess of $90,000 per room in Q1 2005, the average price per room is some 22% to 28% above the annual price per room reported in 2003 ($61,300) and 2004 ($63,900). We anticipate activity will remain strong throughout 2005, estimating aggregate volume to exceed $1 billion. This surge in activity is fuelled by the abundance of capital in the market, a sustained low interest rate environment and growing demand for hotel product by a wide variety of investors, including private investors/high net worth individuals, international capital sources, opportunity and pension fund advisors, REITs and other public companies. Hotel Transaction Summary - Quarter 1 2005

|

|

INNvestment is published quarterly by Colliers International Hotels. Comments and suggestions are welcome |

###

|

Colliers International Hotels Hotel Investment Advisory Services Bill Stone Alam Pirani Deborah Borotsik Sylvia Occhiuzzi [email protected] One Queen Street East Suite 2200 Toronto, Ontario M5C 2Z2 Phone: (416) 777-2200 Fax: (416) 777-9232 http://www.colliershotels.com |

| Also See: | Hotel Financing - Oxymoron or Reality? Robert Shiller, Colliers International / Including Q3 2004 Canadian Hotel Transaction Summary / October 2004 |

| Hotel Growth Strategies; Value Creation and Preservation / Colliers International / September 2004 | |

| Mid Year Canadian Hotel Investment Industry Summary / Colliers International Hotels / July 2003 | |

| Slow, Steady and Strong Wins the Race / Colliers International Hotels / INNvestment Canada Fourth Quarter 2003 / January 2003 | |

| Canadian Hotel Investment Report 2002 - Colliers International Hotels / Feb 2002 | |

| Canadian Hotel Investment Report 2000 - Colliers International Hotel Realty / Feb 2000 |