|

|

|

|

|

|

|

|

Should Impact Hotel Rate Strategy |

.

| By: Gregory J. Miller, February 2005 / Author�s Note: The following

analysis was based on an evaluation of GSA

per diem rates as of October 2004.

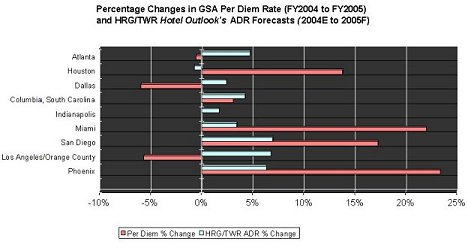

Although we sipped the champagne to celebrate the new year on December 31st, some hoteliers started singing Auld Lang Syne on September 30th. What brought about the early festivities? October 1st marked the beginning of the fiscal year (FY) 2005 General Services Administration (GSA) per diem rates, which defines maximum government rates at qualifying chain-affiliated hotels in the Continental United States. Because government travel is a significant market for many properties, PKF Consulting analyzed how the GSA rates changed from FY2004 to FY2005 in nine markets across the country. We compared the per diem changes against occupancy and ADR forecasts from Hotel Outlook, the joint collaboration of the Hospitality Research Group and Torto Wheaton Research (HRG/TWR). In many markets, FY2005 per diems changed considerably from fiscal year 2004. However, as we show below, hoteliers should not only pay attention to the changes in the GSA rates themselves, but also how comparative forecasts in occupancy and ADR should influence a property�s rate strategy. Per Diem Variables Before we focus on the impact of the FY2005 rates, it is important to understand the variables that make up a per diem rate. A per diem is defined by destination and seasonality. Destination While small markets tend to lack "destination" status, specific per diem rates are set for most large business and leisure destinations. Destinations are generally assigned on a county-by-county basis. Defining a destination by county has two major impacts. A county with notably different submarkets will maintain a common county rate. For example, for Cook County, Illinois, the GSA does not differentiate between the less expensive hotel rooms in the south suburbs and the higher priced rooms in downtown Chicago. Trends over the last ten years have shown that GSA "destinations" have evolved: suburban and exurban counties have taken on their own destination rate. For example, neighboring Anoka and Hennepin Counties of metropolitan Minneapolis used to have a common destination rate. In FY2005, their per diem rates differed by $35. Seasonality Over the past ten years, per diem rates have evolved significantly. In the 1995 fiscal year, destinations with any seasonality would generally be split between a high and low season, at most two rates during the fiscal year. This fiscal year, New Orleans and Palm Beach have four seasonal rates. With more specificity in the seasonality of destinations, the GSA has become cognizant of the complexity of certain markets. Analysis of Per Diems As indicated by changes in GSA rates from FY2004 to FY2005, hotels either celebrated or dreaded the new per diems. As a result of new procedures for calculating rate changes, both large and small markets saw tremendous adjustments for their per diems. Frederick County, Maryland saw a $28 or nearly 30 percent decline in their per diem rate. Conversely, San Diego County�s rate jumped $19, a 17 percent incline. Nationally, per diems rose 8.5 percent. As mentioned above, we evaluated per diem changes from FY2004

to FY2005 against forecast 2004 and 2005 occupancy and ADR figures from

HRG/TWR�s Hotel Outlook. The results are presented in the following

two charts.

In our sample set, one can visually notice that the GSA rate changes for FY2005 are generally more pronounced, either positively or negatively, than the Hotel Outlook forecasts. Among the sample markets, there is no statistical relationship between the per diem changes and the ADR or occupancy forecasts. Relative movements in forecast ADR and occupancy tend to be either opposite in direction and/or significantly different in magnitude from changes in the federal per diem rates. Among our sample set, we observed a few cities that will experience a larger positive per diem change compared to forecast changes in occupancy and ADR. For example, Hotel Outlook is forecasting respectable increases in occupancy and ADR in markets such as Miami, San Diego, and Phoenix for 2005. However, in these cities, the occupancy and ADR forecasts are not nearly as large as the per diem changes for 2005. The strong per diem increases made by the GSA in these markets might represent a correction of low prior year rates. A second scenario was found in markets where per diems will drop significantly in 2005. Dallas and Los Angeles/Orange County have significantly lower per diems in 2005 than 2004, each greater than a five percent decline. Interestingly, in both those markets, the Hotel Outlook forecast projects occupancy and ADR increases. Two markets showed less pronounced differences between the per diem changes and the forecasts. Columbia, South Carolina showed a fairly comparable movement between the per diem and the forecast ADR. Indianapolis had no change in the per diem and only a slight increase in forecasted occupancy and ADR. Nevertheless, for most other markets, the GSA changes and HRG/TWR forecasts were widely dissimilar. How Per Diem Changes Should Affect Rate Strategy Through the analysis of the new GSA rates, hoteliers should come away with a few conclusions.

In conclusion, the GSA per diem rates are just that � rates for federal government travelers. The changes the GSA makes in per diems are not indicative of general trends of occupancy or rate for a county, a market, or the country. As federal government travelers are an important market to service, hoteliers should not only consider the changes in per diem rates themselves, but also the magnitude of the per diem changes against forecasts for specific markets. While our analysis is based on nine selected cities, hoteliers can evaluate their own forecasts against changes in their destination�s per diem. While some might have thought that the title of this essay meant to begin, "Playing The Per diems," there was no misprint. One can exploit the effects of per diem changes with a rate strategy that answers this question: When a federal government traveler walks through your hotel doors, should you pop the champagne or flash the "No Vacancy" sign? |

| Contact:

Robert Mandelbaum

|