|

|

|

|

|

|

|

|

| by: Robert Mandelbaum, October 2004

In addition to conventions, leaves, and football, the fall season for most U.S. hotel managers is the time to prepare next year�s budget. After developing the marketing plan, which determines the revenue for the year, the controllers and department heads take over the process to add in the operating expenses. After review by several layers within the management company, the entire document is ultimately presented to the owner for final approval. Together, the marketing plan and budget provide guidance in the following areas:

From PKF Consulting�s Trends in the Hotel Industry database of 4,000 hotel financial statements for 2003, we identified approximately 1,000 statements that contained 2003 budget data. Based on these statements, we compared the revenues and expenses budgeted for 2003 with what was actually earned and spent. Heading into last year, most U.S. hotel managers were clearly optimistic

that 2003 would be a year of recovery after the dramatic declines of 2001

and 2002. Unfortunately, as has been well documented, the spring 2003 war

in Iraq, along with other economic factors, delayed the start of the industry�s

recovery until later in the year. The disparity between the hopefulness

felt in the fall of 2002 and the reality now observed from 2004 becomes

very evident when comparing actual versus budgeted hotel performance for

2003.

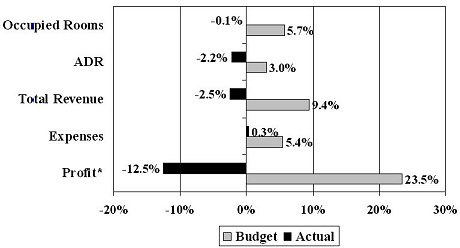

Budget vs Actual (Percent Change From 2002-2003)

Note: *-Before deducting capital reserves, rent, interest, income taxes, depreciation, and amortization. Source: The Hospitality Research Group Starting at the top of the income statement, we see the hotels in our sample budgeting for a 9.4 percent increase in total revenue in 2003. This projection was based on an expected 5.7 percent increase in occupancy, as well as a 3.0 percent rise in room rates. While a second-half recovery did offset most of the first-half loss in occupied rooms, hotel managers continued to discount their rooms throughout the year. The actual results for 2003 were a slight decline (0.1 percent) in occupancy combined with a 2.2 drop in average rate. Ultimately, the hotels in our sample experienced a 2.5 percent decline in total revenue, far off the 9.4 percent increase planned for in the 2003 budget. Expecting revenues to grow 9.4 percent, hotel managers budgeted for a 5.4 percent increase in operating expenses in 2003. With revenues planned to grow greater than expenses, the hotel budgets called for a tremendous 23.5 percent increase in operating profits for the year. Operating profits are defined as income before deducting capital reserves, rent, interest, income taxes, depreciation, and amortization. With the number of rooms occupied and total revenue actually declining, hotel managers did refrain from spending the dollars allotted in their 2003 budget. However, by the end of the year, operating expenses at the hotels in our sample did increase 0.3 percent. Therefore, with revenues declining and expenses increasing slightly, actual profitability fell off 12.5 percent in 2003. Again, this compares to an optimistic budget calling for a 23.5 percent increase in profits for the year. What�s Expected In 2005? Most U.S. hotel owners, operators, and analysts (our firm included)

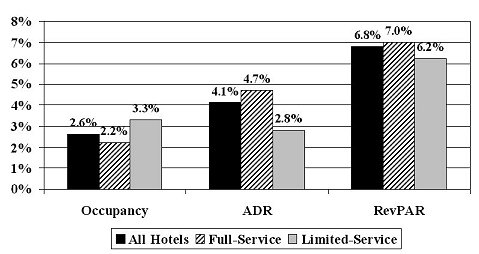

expect the industry growth experienced in 2004 to continue in 2005. Barring

a catastrophic event, the Summer 2004 edition of our Hotel Outlook calls

for a 6.8 percent increase in RevPAR in 2005. This is the result of a projected

2.6 percent gain in occupancy and a 4.1 percent increase in ADR.

Major US Markets* Change from 2004

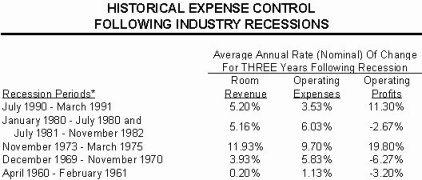

Note: * Based on HRG/TWR Summer 2004 forecast for chain-affiliated hotels. Sources: The Hospitality Research Group, Torto Wheaton Research Hotel Outlook is an econometric forecast jointly developed by The Hospitality Research Group of PKF Consulting and Torto Wheaton Research. The model forecasts the performance of chain-affiliated hotels in the nation�s largest markets. Both full-service and limited-service hotels are forecast to achieve relatively strong gains in RevPAR in 2005. However, market conditions dictate that each segment will achieve their RevPAR increase by employing different yield management strategies. In general, limited-service hotels should enjoy a greater increase in occupancy compared to their full-service counterparts. On the other hand, full-service hotel managers are expected to be more successful in raising room rates than limited-service operators. Expense Control To Dictate Profitability Given the optimistic outlook for hotel revenues, it would be expected that hotel profits grow at a similar pace. This position is bolstered by the fact that RevPAR gains in 2005 should be more heavily influenced by growth in ADR, as opposed to gains in occupancy. Traditionally, hotel profits show their greatest gains when revenue growth is dominated by rate growth. A key to maximizing profitability gains will be the discipline of hotel management to maintain control over the costs for which they have some degree of influence. Unfortunately, hotel operators, historically, have not demonstrated an ability to control costs during periods of recovery. Separate research conducted by HRG reveals that coming out of industry recessions, hotel managers have spent money at a pace greater than the growth of revenues, and/or at a pace greater than inflation. These practices have limited the bottom-line benefit one would expect to receive from increases in revenue. The following chart lists the relative growth of hotel revenues and

expenses in the three years following historical U.S. economic recessions.

Note: *As defined by the National Bureau of Economic Research Source: The Hospitality Research Group of PKF Consulting We have already begun to take notice of expense creep in certain areas of hotel income statements. At 45.3 percent of all operating expenses, labor and related costs represent the largest expense item for hotels. Therefore, they have the greatest influence on hotel profitability. After two years of declining labor costs in 2001 and 2002, these costs increased 3.1 percent in 2003. PKF Consulting projects labor and related costs to increase another 5.0 percent in 2004. While the increase in labor costs do reflect the increased staffing required to service the increase in occupied rooms, management should think about the necessity to restore positions cut during the recession. Fortunately, most operating expenses moved in relative proportion to revenues in 2003. The exceptions were the expenditures made for maintenance, utilities, and insurance, all of which increased "above average". Arguably, hotel managers have limited control over their expenditures for energy and insurance. In addition, hotels should also avoid deferred maintenance. It is hoped that managers have the discipline to continue effectively controlling fixed and variable expenses in 2005. Given the projected increases in revenue and occupied rooms, as well as historical expense trends, PKF Consulting is estimating hotel operating expenses to increase approximately 5.0 percent from 2004 to 2005. With revenues forecast to increase approximately 7.0 percent, this should result in the average hotel achieving a 10 to 12 percent gain in profits in 2005. * * * |

| Contact:

Robert Mandelbaum

|

.