|

. INNvestment Canada Third Quarter 2004 |

|

|

Oxymoron or Reality? Q3 2004 Canadian Hotel Transaction Summary by Robert Shiller, Vice President Capital Markets, Colliers International Hotel financing continues to be difficult to obtain and is largely driven by relationship lending and the quality of the project/sponsor. Loan amounts typically do not exceed 50% to 55% of the underlying value of the property. Most lenders view hotel financing to be more business than real estate financing. As such, the capabilities of the sponsor/ management team, as well as their financial wherewithal, are key components in obtaining attractive financing. Most lenders will require some recourse to the sponsor. Also important is the track record of the hotel. Typically up to three years of healthy financial results will be required. Financing of a new development becomes more difficult and will likely require separate lenders for the construction and long term financing of the hotel. Hotels located in a major metropolitan area will also be advantageous. Hotels in secondary markets pose challenges unless they are part of a larger portfolio of hotels/motels. In addition, hotels flying a well-established flag are often a prerequisite. The amount of leverage available for hotel financing is usually less than what is available for traditional commercial real estate. Many lenders that are comfortable with hotels would limit leverage to 50%-55% of the value of the property. Pricing will usually be 225-250 basis points (�bps�) over the corresponding Bank of Canada Rate for a fixed rate, term of five to ten years. This is 75 bps to 100 bps greater than spreads for other real estate. Pricing can be thinner, possibly as low as 200 basis points over the Bank of Canada Rates on hotels flagged by a major chain and with strong operating results for the past three to five years. Debt service coverage (�DSC�) needs to be at least 1.4 times. Mortgage Backed players (Conduit Lenders), which include CMO, Merrill Lynch, Column Financial, GMAC and GE Capital have been fairly active with hotel financing. Conduit Lenders pool a series of real estate mortgages which are then sold to the public and private markets in different tranches, based on risk, as determined by Loan to Value. They are basically selling cash flow generated by these pools of mortgages. Often Conduit Lenders cater to the �B Piece� buyers (buyer of the most risky tranche), which determines the parameters of these loans. The lending parameters for most Conduit Lenders are fairly similar and with little flexibility in the structure offered. They will finance single asset properties, however most of these lenders like the diversification of portfolio deals. Other lenders offer floating rate options and more flexibility. Again leverage will peak at the 50%-55% range, with a 25-year amortization. Interest-only financing during the initial years is sometimes offered for turnaround situations. The other contributing factors such as sponsorship and track record would still apply, and are more relevant in these situations. Pricing is usually a spread over 30-day Banker�s Acceptances (BAs), which are currently approximately 2.25%. Spreads can range from 300-400 bps over BAs for an indicative current all in rate of 5.25%-6.25%. These lenders generally provide financing on a non-recourse basis. This type of structure works particularly well in a situation where repositioning or extensive capital expenditures are required. An example on this type of structure is presented below. The name of

the project and lender has been intentionally omitted:

This is only one example of the type of financing that is available.

Hopefully it provides some insight on how lenders perceive hotel loans

and how they are structured. It is important to remember that hotels are

not viewed as typical real estate but as businesses. To be successful in

obtaining alternative financing, one needs to formulate a strong business

plan. Once you have developed this and the numbers make sense, you

will be in a good position to obtain the financing that suits the project.

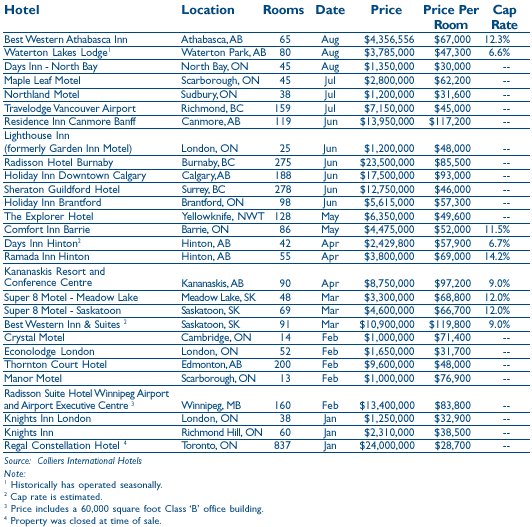

Robert Shiller is Vice President of Capital Markets, Colliers International. Robert has worked extensively with GE Capital and Citibank in various capacities including, but not limited to, Senior Loan Originator and Manager of Asset Management Services. Prior to joining Colliers, Robert was Director of Mezzanine Debt at Caber Capital Inc. where he started a mezzanine debt fund for Cargill Inc. Robert continues to represent Cargill�s Mezzanine Debt Program at Colliers, in addition to working on other Capital Market endeavours. Despite the strong appetite to invest in hotels by a variety of investors, transaction activity for the first three quarters of 2004 was slower than the prior year period, with only 28 hotels sold compared to 40. With approximately $194 million ($57,100 per room) of transaction volume reported nationally, total volume was down some 40.5% year-to-date September 2004 compared to the same period in 2003 when volume reached approximately $326 million. The two most significant trades this quarter were the sale of the Travelodge Vancouver Airport, a 159-room, full-service, airport hotel, which sold in July 2004 to a private investor for $7.15 million and the Best Western Athabasca Inn, which sold for $4.36 million to a private investor in August 2004. Hotel Transaction Summary - YTD September 2004

|

|

INNvestment is published quarterly by Colliers International Hotels. Comments and suggestions are welcome |

###

|

Colliers International Hotels Hotel Investment Advisory Services Bill Stone Alam Pirani Deborah Borotsik Sylvia Occhiuzzi [email protected] One Queen Street East Suite 2200 Toronto, Ontario M5C 2Z2 Phone: (416) 777-2200 Fax: (416) 777-9232 http://www.colliershotels.com |

| Also See: | Hotel Growth Strategies; Value Creation and Preservation / Colliers International / September 2004 |

| Mid Year Canadian Hotel Investment Industry Summary / Colliers International Hotels / July 2003 | |

| Slow, Steady and Strong Wins the Race / Colliers International Hotels / INNvestment Canada Fourth Quarter 2003 / January 2003 | |

| Canadian Hotel Investment Report 2002 - Colliers International Hotels / Feb 2002 | |

| Canadian Hotel Investment Report 2000 - Colliers International Hotel Realty / Feb 2000 |