|

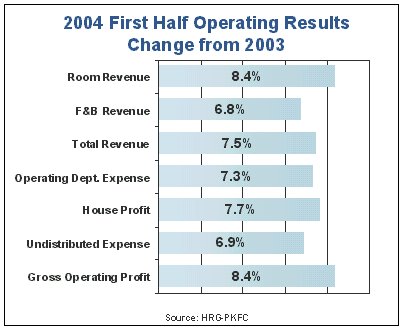

Based on the strong hotel improvements in occupancy and average daily rate already reported in the second half of 2004, HRG expects profit growth to be even higher for the second half and full year 2004. Despite these positive trends, the industry still lags far behind its past peak performance in 1998. The firm said that it doesn�t expect unit level hotel profits and profit margins to reach 1999-2000 levels until 2006 or 2007. �As we expected a year ago, hotel revenue has improved significantly in 2004 as travelers returned to the road and hotel prices continued to rise,� says R. Mark Woodworth, executive managing director of Atlanta-based The Hospitality Research Group. �But what has been overlooked in most reports are the tremendous gains made in profitability which benefits hotel owners and their lenders. But, there is still a lot of upside potential for the industry over the next few years, barring any unforeseen events.� Gross operating profit (GOP) is defined as income before management fees, property taxes, insurance, capital reserves, rent, interest, income taxes, depreciation, and amortization. Revenue Gains Fuel The Growth The tremendous bottom-line growth in hotel profits starts with the strong gains made in top-line revenues. Hotels in the survey sample achieved a 7.5 percent gain in total revenue from the first half of 2003. The main driver of the gain in total revenue came from an 8.4 percent increase in revenue derived from the rental of guest rooms. �The gain in rooms sales certainly has the most

influence on hotel profitability, but I�m sure hoteliers are glad to see

improvement in their other sources of revenue,� says Woodworth. �Of

note were the 7.4 percent increase in food revenue and 4.5 percent growth

in �Other Operated� departments. If operated properly, these supplemental

revenue sources can be significant contributors to a hotel�s bottom-line.�

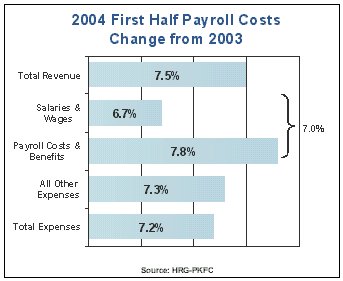

The only revenue source to show a decline from 2003 to 2004 was the telephone department (-5.2%). �This continues a trend we have observed since 2001. Clearly, guests using their own cell phones and calling cards has cut into the use of hotel phones to make toll calls,� notes Woodworth. Expense Control To Dictate Profit Recovery In theory, strong revenue growth automatically should lead to strong profit growth. However, based on an analysis of six U.S. hotel industry recessions dating back to 1960, HRG has found that growth in operating expenses tends to mitigate gains in profitability. �During the recent recession, hotel managers worked diligently to cut their expenses in the face of declining revenue,� says Woodworth. �Some hotel executives stated that these cost cuts would remain in place beyond the length of the recession. Based on our most current survey of hotel operating data, we find that, not surprisingly, increasing expenses once again have crept back into the picture.� While total revenue improved 7.5 percent during the first six months of 2004 for HRG�s study sample, total operating expenses grew 7.2 percent. This rate of expense growth is more than twice the pace of inflation during the same period and has not been seen since 1986. �Given the magnitude of revenue growth experienced thus far in 2004, I would have expected a better improvement in profits. Clearly, expense-creep has eroded the level of potential profit improvement,� says Woodworth. The fixed/variable nature of hotel operating expenses is the primary reason for the disproportionate rise in costs during periods of recovery. After cutting payroll, amenity, and service levels to match the reduced levels of business from 2001 to 2003, hotel managers had to rehire staff, buy extra supplies, and re-open restaurants to serve the needs of an increased volume of guests. �In addition, hotel managers are weary from running their operations on austerity budgets,� says Woodworth. �Now that revenues are up and expectations for sustained, and substantial, revenue and profit growth remain high, management is starting to add back the �little extras� to enhance the guest experience.� Labor Cost Pressure One of the most variable expenses in a hotel is labor. Payroll and related costs historically have averaged 45 percent of all operating expenses and 35 percent of total revenue. For those hotels in HRG�s 2004 mid-year survey, payroll expenses rose 7.0 percent. This compares to a 7.5 percent increase in total revenue. �Most of the bump in labor costs can be attributed to the increase in staff needed to service the additional occupied rooms,� noted Robert Mandelbaum, HRG�s director of research information services. �However, the 7.8 percent increase in employee

benefits is becoming a big concern for U.S. hoteliers. Our clients

are having trouble balancing the desire to offer their employees benefits

like health insurance and 401 K matching with the cost of providing such

benefits. In addition, some benefits are government-mandated with

little room for management control.�

Further compounding the issue are the recent activities of organized labor in certain markets, which will likely take on national prominence in the years ahead. �As the U.S. continues to evolve from a manufacturing to a service-based economy, we expect further upward pressure on hotel labor costs� noted Mandelbaum. For year-end 2004, HRG is projecting hotel-operating profits to be approximately $10,000 per available room. This represents an 11.7 percent gain from year-end 2003. For 2005, HRG forecasts an even larger increase in profits of 14.1 percent, or approximately $11,400 per available room. �The combined 27.5 percent boost in hotel profits from 2003 to 2005 is certainly noteworthy,� says Woodworth. �However, the $11,400 per available room profit level estimated for 2005 still falls short of the profits U.S. hotels were achieving in 1998. Given our projections of revenue beyond 2005, I don�t believe unit level hotel profits and profit margins will reach 1999 � 2000 levels until 2006 or 2007. This is when hotel owners and lenders, who depend on the bottom-line, will declare their recovery.� Everyone Is A Winner While all segments within the full-service hotel category have enjoyed growth in profits during the first half of 2004, certain hotel groups have clearly displayed a more rapid pace of recovery. �In general, hotels with higher room rates appear to have leveraged their revenue gains into profit growth more efficiently than the moderate-priced properties,� says Woodworth. �While hotels in the upper-tier categories are exhibiting greater profit growth during this recovery period, it should be noted that they suffered more during the depths of the recession. Therefore, they have the most ground to make up�. Another full-service hotel category that appears to have benefited greatly in 2004 are full-service hotels with less than 200 rooms. �Most of the relatively new �focused-service� brands fall into this category. These properties typically do not have the extensive food, beverage, banquet, and meeting facilities that require a lot of labor and other operating expenses. Therefore, cost controls are much easier to implement on a permanent basis,� Woodworth observes. To purchase a copy of the 2004 Mid-Year Trends

in the Hotel Industry report, go to www.pkfc.com.

About HRG and PKF Consulting

|