|

|

|

|

|

|

|

|

| By John (Jack) B. Corgel, Ph. D

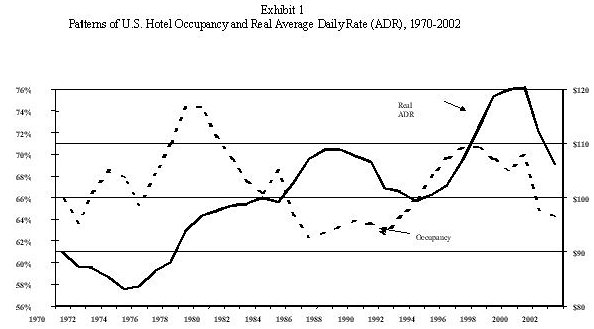

Whether we want to accept the fact or not the hotel business (both the sale of rooms and assets) is a cyclical business. Cycles exist in the hotel business for some good and well documented reasons. Most importantly, hotels are not the same as most other commodities like, say, tooth paste. By this I mean that when the demand for rooms suddenly spikes, as it did during the recent holiday season in New York City, the supply of rooms cannot correspondingly expand within a short period to satisfy the new level of demand. Should the same circumstances occur in the market for tooth paste, producers will turn up the machinery not operating at full capacity, add another work shift, and turn out more tubes before you can say �dental bills.� Thus, hotel supply change lags demand in both the upward and downward directions meaning that RevPAR persists at relatively high levels and growth rates following an upward movement in demand and RevPAR persists at low levels and growth rates following a decline in demand. The cycle�s story just told appears quite tragic unless participants are somehow clever enough to predict the turning points and avoid downturns and troughs. Despite the financial wreckage they created in the past, hotel cycles now generate some underappreciated predictive powers. These powers are fueled by the availability of Smith Travel Research and other data covering a complete cycle (i.e., down from 1987 to 1992, up from 1992 to 2001, and down from 2001 until quite recently). During the latest complete cycle, all the moving parts behaved much as economic theory suggests. If the hotel market recently made an upward turn at the bottom of the cycle as many feel, then we have in our possession the map of how a recovery will unfold. In this article, I attempt to use the knowledge gained during the latest complete cycle to chart a near-term course of events in the U.S. hotel market. Occupancy and ADR - Cycling through Time The existence of hotel market cycles is a well-recognized phenomenon. Smooth and regular fluctuations around an equilibrium level may occur for two reasons. First, a strong correlation exists between measures of national and local market economic activity (e.g., GDP, real personal income, and employment) and hotel demand. Consequently, cyclical patterns in hotel performance measures emanate from business cycle patterns through the demand side of the market. Second, supply changes should logically follow shifts in demand, albeit with long delivery lags. If the business cycle is smooth and construction predictably responds, then the hotel market cycle will have a correspondingly smooth appearance over time. Abnormally wide swings in hotel market performance observed during recent decades occurred because of shocks to the economy and hotel markets. These events either impacted the supply of hotel rooms, demand for hotel room nights, or both. Government intervention of the early 1980s, for example, artificially inflated the supply of hotels. With occupancy already below normal levels in the late 1980s, the recession and Gulf War in the early 1990s stymied the market recovery. Similarly, the combined effects of the demand-based general economic recession beginning in 2001, the terrorist attacks in September 2001 that created a stigma on domestic and international travel caused demand for air travel, and the Iraqi war produced steep declines in hotel occupancy and average daily rate (ADR) during 2001 and 2002. Exhibit 1 shows the cyclical patterns of occupancy and real ADR for U.S. hotels during the past few decades. The following observations come from an examination of these trends: |

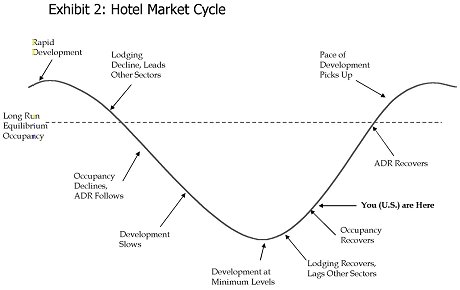

The economics of hotel markets suggest that occupancy represents the current relationship between demand and supply. Occupancy reaches levels above (below) normal when demand exceeds (less than) supply. During periods of abnormally high (low) occupancy, ADR increases (decreases) causing occupancy to fall (rise). The economics of hotel markets also suggest that ADR represents the current relationship between demand and supply, and accordingly, ADR reaches levels above (below) normal when demand exceeds (less than) supply. Once ADR reaches a level in the market for which development becomes feasible. To complete the market process, hotel construction eventually satisfies the excess demand that drove occupancy and ADR above normal. As more rooms are added to the stock, occupancy and ADR fall back to normal levels. At the peak of the cycle the market may become unstable with supply growth continuing after demand is satisfied (i.e., overshooting). This problem of overbuilding is an unfortunate byproduct of cyclical markets. Exhibit 2 presents a graphical representation of the hotel market cycle. The hotel market process involves an observable lag between occupancy change and ADR adjustment. As markets move from the peak of the cycle to the trough, such as during the recent cycle phase from 1998 to 2002, softness in demand forces hotel managers to reduce room rates in an effort to maintain occupancy percent. These actions retard the decline in occupancy during periods when demand drops. The opposite of this process occurs as markets move from the trough of the cycle to the peak. An increase in the demand for hotel rooms causes immediate improvements in occupancy. The upward trend in occupancy moderates as hotel managers begin to raise room rates, which begins occurring as occupancy approaches the natural level of the market. Exhibit 3 provides a summary of how markets �should� behave through an ordinary cycle and in response to external events.

Exhibit 3: Hotel Market Processes in a Normal Cycle and Following Extraordinary Events

Preparing the Map for 2004 and 2005 Armed with recent evidence about the cyclical behavior of the hotel markets can we make any predictions? Returning to Exhibits 2, it appears that the U.S. hotel market at the start of 2004 is in the early stage of an upward movement toward a peak. This movement is conditioned by the general economic recovery which governs its direction. Theory suggests that modest increases in occupancy starting in 2003 IV will continue until occupancy percents reach the long- run average (i.e., somewhere between 65 to 70 percent in most local markets). As the market approaches this point, hotels will be able to begin increasing room rates. From thereon up the slope, occupancy gains will slow and room rate increases will begin to dominate RevPAR growth. In some metropolitan markets, such as New York, occupancy is already near the long-run average. Econometric forecasts from the Hospitality Research Group and Torto Wheaton Research Hotel Outlook indicate that many major markets in the U.S. will experience occupancy at long-run average levels by the end of 2004, meaning their will be room rate growth in 2004 as well. During 2005, room rates will begin approaching development feasibility levels. What does the cycle pattern not help predict? First, cycles have turning points that are nearly impossible to forecast because they often occur as a consequence of unpredictable external stimuli. Second, the extent of overbuilding cannot be anticipated. Academics and financial institution regulators are focusing considerable attention to the problem of real estate market overbuilding today. References Corcoran, P. J. 1987. Explaining the

Commercial Real Estate Market. Journal of Portfolio Management 13

(Spring): 15-21.

* * * John (Jack) B. Corgel, Ph. D is a Professor at the Cornell University School of Hotel Administration. In addition, he serves as Managing Director of Applied Research at The Hospitality Research Group of PKF Consulting. This article was Reprinted from Real Estate Issues with the permission of The Counselors of Real Estate of the National Association of REALTORS®, Vol. 28, No. 4, Winter 2003-2004 |

| Contact:

Robert Mandelbaum

|

.