|

|

|

|

|

|

|

Outlook into 2003 |

| by Melinda McKay, Jones Lang LaSalle Hotels

October 2002 It has been nearly one year since the 9/11 terrorist attacks on New York City and Washington, D.C. Following the tragedy, the country began to regroup and formulate predictions on the overall economic and various industry sector performances in the year that would follow. In this report, Jones Lang LaSalle Hotels examines which post 9/11 predictions came to fruition and which did not, and in doing so discusses the status and outlook of the economy, hotel sector and capital markets. U, V or W � The Economic Alphabet Game Will it be a "U" or "V" shaped economic recovery? That was the debate

among economists around the world following 9/11. The "V" shaped recovery

depicted a contraction in the US economy during Q3-01 and Q4-01, risk to

the first two quarters of 2002, but strong growth expected by mid 2002.

This was considered likely 12 months ago given: (a) a robust consumer market

(via the housing sector); and (b) business balance sheet strength (mainly

via low cost of debt). The reality: a blend of a "U" and "W" shaped recovery,

which is spelled out in the following table

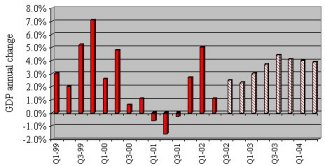

What does the next 12 months hold? The expectation is for a recovery to normalized growth rates by 2003. Weak profits and layoffs continue to characterize the corporate sector, although an improvement in earnings is expected in the second half of 2002. On reflection, the remainder of 2002 will record modest GDP growth of between 2.3 to 2.8 percent, with 2003 expected to measure 3.1 percent. These trends are reflected in the following graph. However, a crisis of confidence in the stock market could affect the timing and pace of recovery, with consumers and businesses likely to limit spending until equity prices lift decisively and the bond yield spread narrows. Borrowing costs remain at a 40-year low and capital investment is predicted to re-commence in the first part of 2003. Gross debt flows to real estate remain very strong; however, the net level is lower due to high level of refinancing. There is a real possibility of a war with Iraq, however the impact on the US economy is anticipated to be limited for a number of reasons. Firstly, the potential invasion has been highly publicized, with consumers and the stock market already pricing-in the effect of such a conflict. This contrasts to the 1990 Gulf War, which was unexpected shock and therefore had a significant impact on consumer confidence and the economy. Secondly, the actual cost of the war is unlikely to impact greatly on the economy or long term interest rates, with the estimated $8.0 billion price tag (if similar in scope to Desert Storm) increasing the budget deficit from 1.3 percent of GDP to 2.0 percent of GDP. While the most obvious impact would be on oil prices, it is doubtful a spike will occur as other oil producing nations have had time to increase oil productions and inventories have subsequently risen. Add to this the fact that a �war premium� has recently been built in to oil prices to take into consideration the likelihood of conflict. The mid case scenario forecast by Economy.com estimates a 45 basis point detrimental effect on GDP in 2003 translating into a revised growth of 2.7 percent. However, key risks remain including further terrorism attacks, unusually large losses of American lives, extended conflict and a complete destabilization of the Middle East region, all of which would negatively affect consumer confidence and national economic health. Yet many experts predict the relative likelihood of these events occurring as diminutive. US Avoids Double Dip Recession

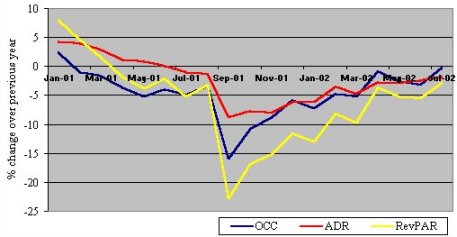

Hotel Performance � a Comparison of Realized Risk by Segment The U.S. hotel sector is dragging itself out of one of the sharpest downturns in history. Occupancy (OCC) and average daily rate (ADR) remain slightly below 2001 levels for ytd August 2002, resulting in a 6.2 percent decline in revenue per available room (RevPAR) during the period. The graph on the page overleaf depicts the pattern of OCC, ADR and RevPAR. This is not dissimilar to the outlook 12 months ago, although few predicted the depth and length of the decline, with performance levels anticipated to recover by mid 2002. However, the consensus that the industry was in a much stronger position to weather this downturn has been proven correct, as outlined in the table on the following page. US Hotel Performance, 2001 to 2002 ytd July

In our September 2001 FocusOn edition, we predicted a number

of segments would be more at risk than others, while certain others would

experience the least negative impact. Of the 10 predictions made 12 months

ago, eight have come true. These are detailed in the following two tables.

In a recent survey of key real estate executives from 50 of its largest (mainly Fortune 1000) clients, Jones Lang LaSalle looked to ascertain the impact of 9/11 on corporate real estate strategies. In many cases, these effects translate to the hotel sector, namely:

Year-on-year statistics during the last four months of 2002 will start to show a considerable improvement given that historical comparisons will include the impact of 9/11 and the full brunt of the economic recession. Luxury hotels, while remaining at the bottom of the performance ladder, have shown the largest improvement in performance ratios in 2002 and this is likely to continue. Real momentum, however, will not gather until the middle part of 2003 as corporate travel budgets begin to resemble historical amounts. In terms of location, airport hotels are likely to remain out of favor, at least until there is a dramatic recovery in air travel. Resort properties have shown the largest improvement since 9/11, and this recovery will continue as exchange rate influences keep domestic travelers at home and attract international tourists (particularly as their local economies improve). Leisure travel has rebounded faster than corporate visitation. However, with a continued built in GDP growth, eventual stabilization of financial markets and a return to corporate profits, major cities are likely to enjoy a commensurate lift in performance ratios. Yet these trends are unlikely to materialize until 2003, which places a real recovery for corporate-led markets later that year. Investors have become increasingly bullish on the outlook of major US cities. According to our Jul-02 edition of the Hotel Investment Sentiment Survey (HISS), San Francisco and Boston are among the top markets expected to enjoy the largest turnaround in trading performance between the short (six months) and medium (two years) term, with particularly strong medium term expectations for New York. In general, trading expectations for the remainder of 2002 are weighted toward the negative, but a significantly higher proportion of investors believe that the market will be flat or improve. Reflective of this outlook, investors consider that most of the hotel markets have reached the bottom of the cycle, and in fact some, namely New York, Los Angeles and Washington D.C., are positioned in the early upturn phase. Given investors' confidence in the medium term trading performance of the hotel markets, it would not be surprising to see all of the 15 North American markets on the upturn during the next HISS. Transaction Activity Rebounds Immediately following 9/11, the hotel capital markets froze, with virtually

all in-progress hotel transactions being cancelled or significantly delayed.

What followed was a skittish capital market, with cap rate expectations

soaring in compensation for what investors perceived as a highly uncertain

outlook for hotel performance. In turn, owners were reluctant to part with

assets given the dramatic short term decline in asset values. The prediction

that this "standoff" between buyers and sellers would come to an end was

proved correct as outlined in the following table.

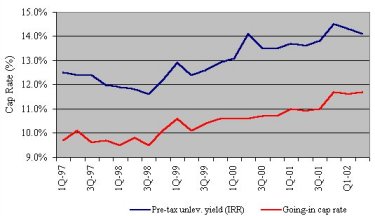

Further evidence that investors are being more realistic about asset values is the easing of cap rate expectations over the last six months, as confirmed by the Jul-02 of our HISS. Investors are less aggressive on cap rate requirements, with the required rate shifting down slightly, particularly in the Florida markets and in New York and Washington D.C. Other industry sources support these trends. As the graph overleaf illustrates, a spike in yield requirements has subsequently leveled or contracted in Q2-02. These movements are not so obvious as they represent national trends. Hotel Investor Yield Requirements

What does the next 12 months hold? Expectations for continued growth in transaction activity are well founded. The combination of increases in demand and limited new supply will help support growth in RevPAR during 2003. Combined with the existing pent-up investor demand, this creates an environment ripe for a record volume of transactions. Already, the number of investors hunting for assets exceeds product available for sale. This was reaffirmed in the Jul-02 edition of our HISS, in which over one-third of investors indicated they were seeking to buy hotels, while very few indicated a sell attitude Given these conditions, transaction volume is expected to reach approximately

$3 billion by the close of 2002, with 2003 set to record around twice that

amount of sales. These trends are detailed on a quarterly basis in the

graph on the following page. Cap rates will conform to historical numbers

during 2003 given the sentiment that the market has reached bottom and

investors will be pricing upside moving forward.

Hotel Transaction Trends by Quarter

|

|

Debt Markets Remain Open for Hotel Lending The debt markets have slowly recovered since 9/11 however, higher pricing

and lower leverage ratios exist compared to pre-9/11. Gearing ratios have

become increasingly conservative over the last six months, with higher

pricing and lower loan-to-value (LTV) ratios than other forms of real estate.

This trend was exhibited in the Jul-02 HISS results and underscores

the prediction made 12 months ago as featured in the following table.

Lenders will continue to approach hotel investments with caution until there is evidence of a real and sustained recovery in trading performance. Yet while lenders remain conservative there is in fact an excess of debt capital available given the comparatively limited number of deals in the market. On several recent debt placements, Jones Lang LaSalle Hotels has secured favorable financing terms due to lenders aggressively competing for deals. The availability of and the environment surrounding terrorism insurance

remains a notable issue when attempting to secure debt capital. Soon after

the 9/11 attacks, the cost of coverage increased dramatically, while the

available supply of terrorism insurance declined abruptly. According to

a survey by the Mortgage Bankers Association of America, the lack of terrorism

insurance has directly affected more than $8 billion in commercial property

deals in the first half of 2002. However, in the hotel sector it appears

that the issue of terrorism insurance has not stalled/cancelled any specific

deal. This prediction is spelled out in the following table.

The situation remains unsettled, as the market for terrorism coverage is unstable. Prices remain high and securing coverage is becoming increasingly difficult in certain markets. Some insurers, for example, will not write policies for property located in zip codes in which the level of terrorism coverage they already support makes them averse to assuming additional risk. Some capital sources are unwilling to lend on real estate assets unless the full value of the loan is covered against terrorism claims. For those properties managed by a major flag, the hotel is often eligible to be covered by the management company�s blanket insurance policy. For individually managed/owned hotels, securing terrorism insurance has been more problematical and costly. Federal legislation designed to resolve the problem remains stalled in Congress, where provisions in an existing bill have rekindled a long-standing fight over tort reform. At best, hotel owners and investors are investing substantially more time and money to secure adequate levels of coverage in this challenging climate. Conclusion One year later, it is clear that the combined impact of 9/11 and the economic downturn on the U.S. hospitality industry has taken shape and will continue to evolve for some time. The most striking example of this is the extent to which terrorism insurance will continue to affect acquisition financing underwriting of prime city hotels. While the hotel sector continues to struggle with low performance ratios, fundamentals remain strong and all indicators point to a real recovery in 2003. Industry stakeholders should take some comfort in the fact that the market has in general performed to expectations, with 12 of the 15 predictions made one year ago being validated. This reflects an industry that has matured greatly over the last decade, particularly in the capital markets arena. |

|

Anwar R. Elgonemy Associate Jones Lang LaSalle Hotels 2655 Le Jeune Road, Suite 1004 Coral Gables, Florida 33134 Tel: (305) 779-4958 Fax: (305) 779-3063 [email protected] www.joneslanglasallehotels.com |

| Also See | The San Francisco Hotel Investment Climate in the Post-Tech Boom Paradigm / Anwar Elgonemy / Oct 2002 |

| Debt Financing Alternatives & Debt Restructuring Strategies in the Lodging Industry / Anwar R. Elgonemy / Sept 2002 | |

| Concrete to Cash: Real Estate Sale-Leasebacks in the Lodging Sector / Jones Lang LaSalle Hotels / March 2002 | |

| The Dynamics of a Hotel Deal in Mexico / Jones Lang LaSalle / July 2002 |

To search Hotel Online data base of News and Trends Go to Hotel.Online Search