|

Strong Transaction Activity to Continue

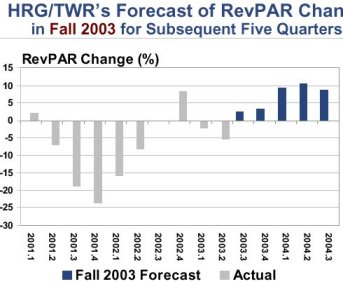

HRG, along with CBRE�s Torto Wheaton Research of Boston (TWR), prepare long-range forecasts for the top 50 U.S. hotel markets on a quarterly basis. Their estimates for the 2004 � 2005 period were released at a press briefing today at the Jacob K. Javits Convention Center in New York City concurrent with the American Hotel & Lodging Association�s annual International Hotel/Motel and Restaurant Show. Classic Recovery Scenario By year-end 2004, HRG projects that the Top 50 U.S. hotel markets will achieve an average occupancy of 64.8 percent, which represents a 5.4 percent gain over 2003 levels. Concurrently, average daily room rates are expected to grow from $94.37 in 2003 to $97.84 in 2004, or an increase of 3.7 percent. Going forward, occupancy is forecast to improve to 66.6 percent in 2005, while the ADR should jump 4.7 percent to $102.42. �In 2004, gains in rooms revenue (RevPAR) have been dominated by the increases in occupied rooms,� says Woodworth. �In 2005, ADR will be the main driver of RevPAR improvement, and when ADR dominates RevPAR growth, more dollars fall to the bottom-line.� Major U.S. city lodging markets currently are experiencing a classic

recovery scenario after experiencing a three-year industry recession, a

trend that not occurred since J.F.K. was the U.S. president. �The lodging

industry is a cyclical business,� notes Mr. Woodworth. �When coming out

of a recession, hotels initially see an increase in occupancy, followed

by gains in operating expenses, room rates, and finally, profits. In 2004,

U.S. hotels have achieved significant increases in occupancy and we are

projecting even stronger ADR growth in 2005. Selling more rooms and feeding

a greater number of meeting attendees understandably increases operating

expenses, which in turn serves to mitigate the benefits of strong revenue

growth.�

. Since revenue from guest room rentals comprises approximately 65 percent of a typical hotel�s total revenue, the previously described increases in RevPAR also have resulted in strong gains in total hotel revenue, (which include sales from such sources as restaurants, lounges, catering, gift shops, golf courses, and parking). In 2004, HRG estimates the average U.S. hotel will achieve an 8.5 percent gain in total revenue, which will mark the first time since 2000 that U.S. hotels realized an increase in total sales. For 2005, HRG is forecasting a 7.2 percent growth in total hotel revenue, to an average of approximately $44,000 per available room (a volume roughly equal to that last achieved in 2000). �It should be noted that this notion of �revenue recovery� is in nominal dollars and does not take four years of inflation into consideration. In real terms, the industry is still very much in the recovery mode,� Woodworth concludes. Expense Control To Dictate Profit Recovery In theory, strong revenue growth automatically should lead to strong profit growth. However, based on an analysis of six U.S. hotel industry recessions dating back to 1960, HRG has found that growth in operating expenses tends to mitigate gains in profitability. �During the recent recession, hotel managers did as good a job as possible cutting their expenses in the face of declining revenue,� says Woodworth. �Some hotel executives stated that these cost cuts would remain in place beyond the length of the recession. Based on our most current survey of hotel operating data, we find that, not surprisingly, increasing expenses once again have crept back into the picture.� HRG recently completed an analysis of the financial performance of 700 full-service hotels in the United States. For this sample, total revenue improved 7.5 percent during the first six months of 2004 compared to the first half of 2003. Concurrently, total operating expenses grew 7.2 percent, more than twice the pace of inflation during the same period. �Because of the operating leverage endemic to hotels, even a slight growth premium in revenues relative to expenses results in favorable increases to the bottom line. With revenues growing faster than expenses during the first half of this year, Gross Operating Profits did improve a healthy 8.4 percent,� notes Woodworth. �However, given the magnitude of revenue growth, I would have expected a better improvement in profits. In the future, the key to driving profitability will be the discipline to maintain control over the costs for which management has some degree of influence.� The impact on profits resulting from the 9.6 percent gain in revenues expected for 2004 will be mitigated by a 7.5 percent increase in expenses. �This level of cost escalation has not been seen since 1986� noted Woodworth. For year-end 2004, HRG is projecting hotel-operating profits to be approximately $10,000 per available room. This represents an 11.7 percent gain from year-end 2003. For 2005, HRG forecasts another strong increase in profits of 14.1 percent, or approximately $11,400 per available room. Operating profits are defined as income before capital reserves, rent, interest, income taxes, depreciation, and amortization. �The combined 27.5 percent boost in hotel profits from 2003 to 2005 is certainly noteworthy,� says Woodworth. �However, the $11,400 per available room profit level estimated for 2005 still falls short of the profits U.S. hotels were achieving in 1998. Given our projections of revenue beyond 2005, I don�t believe unit level hotel profits and profit margins will reach 1999 � 2000 levels until 2006 or 2007. This is when hotel owners and lenders, who depend on the bottom-line, will declare their recovery.� Full In 2004, Limited In 2005 All property types have been enjoying improved RevPAR performance in 2004 and are expected to do so again in 2005. However, the relative recovery of full- and limited-service hotels will vary. In 2004, full-service hotels are forecast to improve their RevPAR by 9.3 percent, while limited-service RevPAR is projected to increase 8.3 percent. �The main reason for the disparity in growth is the enhanced ability of full-service hotels to increase their room rates,� says Woodworth. �Full-service room rates are forecast to grow 3.9 percent in 2004, while limited-service hotels will only be able to improve their ADR by 2.8 percent.� In 2005, the relative pace of recovery switches. Limited-service RevPAR

is forecast to grow 8.4 percent next year, while full-service hotels will

see a 7.7 percent increase in RevPAR. �Looking at a long-term perspective,

the forecast RevPAR growth rates will allow limited-service hotels to exceed

their 2000 RevPAR levels by the end of 2005. Full-service hotels, on the

other hand, are still not projected to exceed their 2000 RevPAR rate until

2006,� notes Woodworth.

Why Expense Creep? The fixed/variable nature of hotel operating expenses is the primary reason for the disproportionate rise in costs during periods of recovery. After cutting payroll, amenity, and service levels to match the reduced levels of business from 2001 to 2003, hotel managers had to rehire staff, buy extra supplies, and re-open restaurants to serve the needs of an increased volume of guests. �In addition, I suspect that hotel managers get a little tired of running their operations on austerity budgets,� says Woodworth. �Now that revenues are up and the future looks bright, management is starting to add back the �little extras� to enhance the guest experience.� One of the most variable expenses in a hotel is labor. Payroll and related costs historically have averaged 45 percent of all operating expenses and 35 percent of total revenue. For those hotels in HRG�s 2004 mid-year survey, payroll expenses rose 7.0 percent. This compares to a 7.5 percent increase in total revenue. �Most of the bump in labor costs can be attributed to the increase in staff needed to service the additional occupied rooms,� Woodworth explains. �However, the 7.8 percent increase in employee benefits is becoming a big concern for U.S. hoteliers. Our clients are having trouble balancing the desire to offer their employees benefits like health insurance and 401 K matching with the cost of providing such benefits. In addition, some benefits are government mandated with little room for management control.� Further compounding the issue are the recent activities of organized labor in certain markets, which will likely take on national prominence in the years ahead. �As the U.S. continues to evolve from a manufacturing to a service-based economy, we expect further upward pressure on hotel labor costs� noted Woodworth. Impact on the Investment Community Hotel investors have noticed the current and projected improvement in hotel industry operating fundamentals. Transaction, lending, and investment activity are on the rise as real estate and financial executives continue to be attracted to the relative appeal of above-market returns, �an expectation that we believe is well-founded� says Woodworth. �Compared to other forms of real estate, hotels are now perceived as having a relatively high upside combined with a relatively low associated risk.� One beneficiary of the increase in hotel profits is the lending community. According to data from Trepp and JP Morgan, hotel loan delinquencies have reduced from 6.3 percent in 2003 to 5.0 percent in 2004. �In addition, HRG is tracking a reduction in the percentage of hotels in our database that are unable to generate sufficient cash from operations to cover their interest obligations. This number has declined from 19.2 percent in 2003 to 16.9 percent in 2004,� notes Woodworth. Enhanced performance has also led to increases in hotel values. Values have increased due to both the improvement in hotel profits, as well as a reduction in capitalization rates. �The reduction in cap rates is yet another indication of the favor in which investors perceive the hotel industry,� says Woodworth. �Although interest rates have begun to increase, the anticipated growth in hotel incomes in the near to mid term should effectively keep cap rates at their current level, if not slightly lower.� �Another indicator of investor interest in hotels is the quality of assets being bought and sold. In 2004, we have seen an increase in the number of larger, chain-affiliated, full-service, resort, and luxury hotels being transacted. From 2001 to 2003, most of the hotels being disposed of were smaller poor performing limited-service properties,� noted Woodworth. Limited Fear Of Overbuilding In the past, overdevelopment has been one of the biggest fears of hotel owners, operators, investors, and lenders. Prior to the 1990s, hotel development activity had few restraints, which led to highly competitive market conditions and had a negative effect on all hotels� performance. Since then, hotel developers and lenders have been more disciplined, but forecasts of improved conditions do stimulate fears of overbuilding. To examine the potential for overdevelopment in the next few years, HRG studied hotel development activity in 10 markets across the United States. In each market, HRG/TWR forecasts of supply for 2004 through 2009 were compared to the development activity in Smith Travel Research�s pipeline reports. �In general, this analysis compared the number of hotels rooms that will most likely be built in each market over the next five years to the number of rooms that are currently in planning or are under construction,� Woodworth explains. The results of the analysis found no markets that were in imminent danger of being over developed. Of the 10 markets studied, the Miami lodging market is furthest down the development pipeline. In Miami, 57.1 percent of the rooms that are eventually expected to be built over the next five years are currently either under construction or in the final planning stages. Conversely, in Atlanta, only 18.7 percent of the estimated build-out is currently under development. �When thinking about where to build a hotel, most developers look at the standard measurements of occupancy, ADR, and RevPAR. We believe our analysis sheds new light on how to identify markets that show the potential support for hotel development,� says Woodworth. Winners and Losers �The long-awaited road to recovery in the lodging industry is populated by those that benefit and those to seem to not fare as well� noted Woodworth. �The list of winners, however, far exceeds that of the losers.� Hotel owners (bigger deposits at the bank), franchise companies (royalty income continues to grow along with room sales), management firms (both base and incentive fees will increase significantly), lenders (they sleep better at night) and employees (remember those increasing payroll costs?) benefit by the good times, as do the product and service providers that service the lodging industry. Who loses? Perhaps it is the customer that will continue to pay more for their room and, increasingly, will find booking the space they desire more and more of a challenge. �While this is a trend we see evolving in certain key markets already (particularly New York City), it will be another two years before this becomes a real issue for consumers says Woodworth. New York City Forecast As part of the presentation, John Fox, Senior Vice President of the New York office of PKF Consulting shared his outlook for the New York City lodging market. The New York lodging market is recovering the severe fall off in performance that occurred after September 11, 2001. Occupancy rates are back above 80 percent and ADRs in 2004 will experience real growth above inflation for the first time since 2000. �By year-end 2004, New York City hotel occupancy is estimated to be 82.6 percent with an ADR of $208.38,� says Fox. �Despite having rooms rates less than 2000 levels, New York City still leads the nation in both occupancy and ADR. The city will sell-out approximately 200 times in both 2004 and 2005.� HRG is forecasting strong growth for New York City occupancy and ADR rates again next year. For year-end 2005, HRG projects New York City occupancy to be 84.0 percent, with an average daily rate of $236.89. �New York has benefited from increases in all types of travelers to the city since 2001,� says Fox. �People are coming to the city for both business and leisure purposes, as well as from both domestic and international points of origin. We have a very diverse demand base that should sustain us in the future.� Despite the strong performance of the lodging market, some hotels in New York are being converted to other uses. �In 2004, we�ve seen five hotels close and convert to residential use,� notes Fox. To view a complete copy of the press conference

The Hospitality Research Group (HRG) is the research affiliate of PKF Consulting a consulting and real estate firm specializing in the hospitality industry. PKF Consulting has offices in New York, Boston, Philadelphia, Washington DC, Atlanta, Indianapolis, Houston, Dallas, Los Angeles, and San Francisco. Hotel Outlook is an objective econometric model developed jointly by HRG and Torto Wheaton Research of Boston (TWR). The model is used by HRG and TWR to forecast the performance of 50 of the nation�s largest hotel market. The forecasts are prepared for both full- and limited-service hotels on a quarterly basis and project of a six-year period. The forecast are updated each quarter. |