| by: Robert Mandelbaum, December 2004

During the recent industry recession, convention

hotels have suffered more than any other property type covered in PKF Consulting�s

Trends in the Hotel Industry reports. The typical convention hotel

showed a staggering 40 percent decline in profits during the past three

years. From 2000 to 2003, convention hotel revenue has declined 17.4 For convention hotels, the return of corporate and association meetings will drive their recovery. In its heyday, the meetings business accounted for 51 percent of the total room nights occupied at these hotels. For convention business to begin to boom again, both corporate budgets and personal pocketbooks must expand to stimulate increased meeting production and attendee travel. To get an update on the current status of the meetings market, PKF Consulting, on behalf of Convention South magazine, surveyed 100 meeting planners throughout the nation that conduct meetings in the Southeast region. The mix of the planners was as follows:

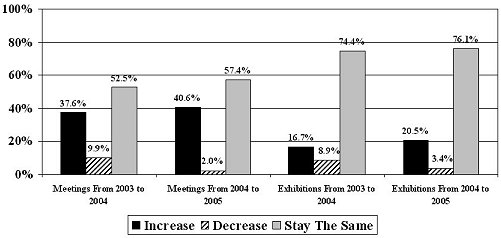

To better understand the recovery that is occurring in the meeting�s market, as well as familiarize hotel operators with the current thinking of meeting planners, we present the following highlights of our survey. Number of Events The majority of planners polled believe that the

number of events they will coordinate in 2005 will be the same as the amount

planned in 2004. However, we have seen an increase in the percentage

of planners anticipating a rise in events coordinated in 2005. The

planners responsible for meetings appear to be more bullish than the planners

that coordinate exhibitions. Chart A shows the expectations of meeting

planners regarding the number of events they will coordinate in 2004 and

2005.

CHANGE IN NUMBER OF EVENTS Percent of Meeting Planners

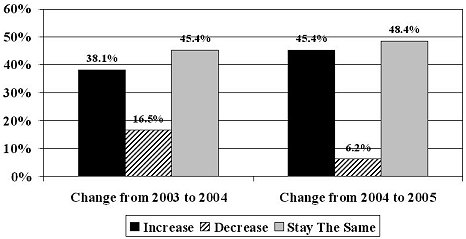

. More Money and Time Two more indicators of the increased confidence meeting planners have when looking towards the future are the increases noted for booking lead times and event budgets. An increasing number of meeting planners are receiving

larger budgets to hold meetings (see Chart B). The percentage of

planners noting an increase in their budgeted per attendee expenditures

grew from 38.1 percent (for their 2004 budgets) to 45.4 percent (for their

2005 budgets). Given the previously noted increases in expected attendance,

combined with the increases in per delegate budgets, it can be assumed

that these corporations and associations believe that meetings are an important

part of their operations and deserve greater investment.

MEETING BUDGETS Percent of Meeting Planners

The increase in booking lead times is another indication that meeting planners are more assured of coordinating a growing number of events in the future. Although the growth in lead time has not been dramatic, the trend has been moving upward each year from 21.6 months in 2002 to 23.4 months in 2004. Satisfaction Having had more leverage during negations from 2001 through 2003, meeting planners were in a stronger position to express their thoughts regarding the service they received at meeting sites. Given this opportunity to be candid, it is worth noting that the majority of meeting planners (62.0 percent) have not perceived a change in the quality level of service they have received. Knowing the cuts in staffing and amenities that hotels have had to make in the past few years, this is somewhat encouraging. In addition, more planners (22.8 percent) believe service levels have improved, as opposed to declining (15.2 percent). Technology Hotels have invested a lot of time and money in technology for guest use. Investments have been made in both guest room and meeting room technology. Fortunately for hotel owners, this investment appears to have paid off in the minds of meeting planners. The majority of respondents (69.2 percent) indicated that they have been satisfied or very satisfied with the technology at their meeting sites. Measuring the importance of technology within a hotel, meeting planners appear to be more concerned with the technology that is available for use by their attendees in the guest room, as opposed to the meeting room. For example, high-speed internet connectivity in the meeting room was rated as very important or essential by just 40.2 percent of the planners. On the other hand, the availability of the same technology in meeting rooms was rated as very important or essential by 52.1 percent of the respondents. Wireless technology (Wi-Fi) has been a hot-button technology issue for hoteliers in the past years. While this technology is believed to be of great importance for individual business travelers, meeting planners do not perceive it to be so vital. Close to eighty percent of the planners surveyed ranked wireless connectivity in both meeting rooms and guest room as only somewhat important or unimportant. IMPORTANCE OF TECHNOLOGY IN MEETING ROOM

Percent Of Respondents

Summary Barring catastrophic events, we believe that the meetings market segment should rebound along with the corporate travel market during the next few years. However, because of the necessary lead times for most meetings, convention hotels might not recognize the optimism shown in today�s survey until a few years out. Other research conducted by PKF Consulting has found that current market conditions do influence the tenor of current contract negotiations for future meetings. Therefore, look for the pendulum of negotiating leverage to begin to sway back towards the hotel sales manager as occupancies and average room rates grow in the next few years. Robert Mandelbaum is the Director of Research Information Services for the Hospitality Research Group of PKF Consulting. He is located in the firm�s Atlanta office. |