| The Global

Hospitality Advisor

-Outlook 2005:

Hotel Industry Fundamentals Where have we been? Where are we going? |

|

|

|

| The Global

Hospitality Advisor

-Outlook 2005:

Hotel Industry Fundamentals Where have we been? Where are we going? |

|

|

December 2004

Daniel Lesser: Hotel companies will certainly have more pricing power similar to what the industry experienced during 1999 and 2000 because of the steady decline in unemployment, a boost in corporate budgets, and an increase in corporate travel and group meeting business. Bill Reynolds: I think everyone on this panel would agree that pricing control has recovered considerably in the industry and that will continue. You all express some valid reasons for the recovery, but the brands have played the biggest role in this and consolidation of ownership has added to industry pricing discipline, as well. Occupied rooms, as an absolute number, are forecasted to exceed the

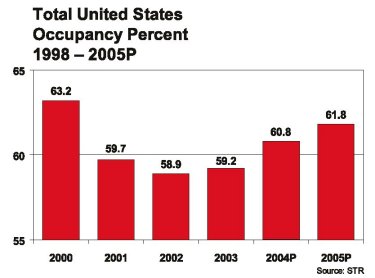

level of occupied rooms in 2000. Percentage occupancy is still several

points shy of 2000 levels, of course, but improving. As building continues

to slow, occupancy percentages will increase, enabling the strong ADR and

RevPAR growth projected by the analysts to reach 3.5% ADR growth and 5%

RevPAR growth this year, with 2006 not too far off those marks.

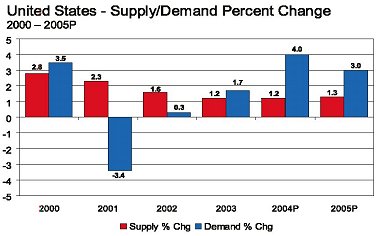

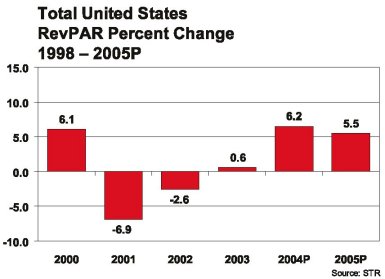

Mark Lomanno: Generally, at Smith Travel, we see continued improvement, especially from an ADR standpoint. Much of the ADR gains experienced this year have been the result of a changing mix rather than real ADR increases. By that I mean that as occupancies rise during the week, which are higher rated days, it pulls up the monthly average simply because of more rooms sold on days where hotels charge more. Because of that we believe that, with the exception of a few markets�New York City and others�real room rate increases are only at the very beginning of the cycle. If that is indeed true, the industry will still have the opportunity to increase ADRs at a pace well above the inflation rate. Butler: Historically, the hospitality industry is notorious for inflicting self injury by generating more new hotel rooms faster than demand can match. But we aren�t doing that yet, are we Mark? Lomanno: That�s right, Jim. At least for now, supply growth is at historically low levels, hovering around 1.1% per annum, and with demand increasing at levels not seen in almost four years, 2005 looks to be the second consecutive strong year for the U.S. lodging industry. Demand levels are so strong that, in 2004, U.S. hotels sold approximately 120,000 more rooms per day than were sold in 2003. While this level of growth will slow somewhat in 2005, it will still be growing much faster than supply, resulting in significant occupancy growth. With strong demand and improving occupancies, the door will be open

to accelerating room rate increases next year, well above of the projected

inflation rate. This will result in RevPAR numbers to reach all time highs

in 2005. However, in real dollars, after factoring in the rate of inflation,

RevPAR will still lag the highs reached in 2000.

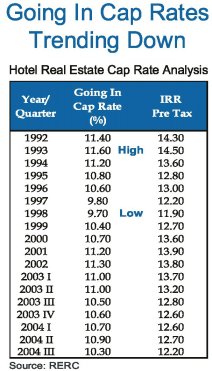

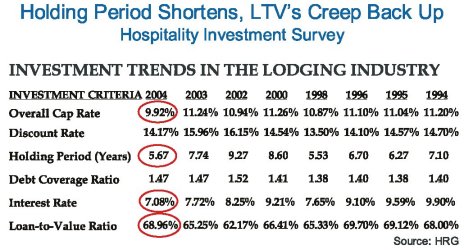

.  Butler: What is driving this growth in demand? Lesser: Well, Jim, economic fundamentals have been exhibiting positive trends, coupled with a rebound of consumer and business confidence. The "road warrior" is traveling again and Americans are continuing to vacation domestically. Increasing confidence has bolstered consumer spending. Lomanno: This will likely be one of the best years in recent memory for the hotel industry. The industry will sell more rooms than at any time in its history and the consumers of those rooms will spend more money than ever before on the purchase of those rooms. Butler: How long is the shadow on the hotel industry cast by the threat of terrorism in a post-9/11 world? Daniel Abrams: Jim, the hotel industry weathered the 9/11 attacks better than it is given credit for. Think about it. The recovery of the hotel industry from the 2001 downturn was hampered more by the dearth of business travelers, which can be laid at the feet of the recession, than lack of tourists, which can be attributed to a reaction to terrorism. Compared to the recession in the early 1990s, where the industry lost billions of dollars on an aggregate basis, the most recent recession, resulted in industry-wide profits falling from $23 billion to between $16 billion or $17 billion. Not bad for the worst situation you could imagine! Lesser: You make a good point, Dan, but we must understand that for the past three years, Americans have been living with a "new reality" that is not so new in many other parts of the world. Terrorism has been a fact of life in Israel and in European and Asian capitals such as London, Paris, and Tokyo, for decades. In spite of this unfortunate way of living, their underlying economies have, over the long term, been resilient and have grown. Look for a similar assimilation of this way of life to continue to bake into the American psyche and provide continued long-term growth in the U.S. economy and positive movement for the lodging industry. Tom Engel: All in all, the hotel industry will grudgingly accept doing business in and with a permanently changed world: managing through daily security risks, a fluky international economy, and a fickle and increasingly less-than-brand-loyal consumer. Accepting this changed world is a bitter pill to swallow because it injects uncertainty into managers� daily decision-making and removes certainty from their daily and longer term decision-making. How effectively our industry manages in this changed world remains to be seen, but I firmly believe this new mantra will become a permanent reality. Hotel Transactions and Pricing Butler: Aside from industry fundamentals, what is happening with hotel transaction pace and pricing? Is everyone seeing a significant upward trend on both fronts? Reynolds: Jim, this will be another very strong transaction year for the industry. Someone who is pursuing a turnaround strategy is simply going to price things differently than one who is paying today for long-term hold value. I think we will see more hotels trade hands and the mix of buyers will be somewhat different than we have seen in the hot market that has occurred since mid-2003. Abrams: Bill is right. I think you will continue to see large asset acquisitions, maybe on a corporate level, because people simply want to own more and have a larger asset base. Some of the larger branding companies will seek out other companies as a way to add additional brands to their stable where they perceive gaps or where their existing brands have reached saturation, nationally or in specific markets. But, once you have reached a certain size, I do not think that there are a lot of efficiencies to be gained from simply owning more properties. Bill Blackham: Jim, at Eagle Hospitality we are actively seeking to expand our portfolio of upscale full-service hotels in a hotel property sale transaction market that is likely to have volume levels significantly above 2004. If hotel acquisitions pricing continues to escalate at the growth rates that occurred in 2004, we will see a significant increase in the number of new hotel developments that break ground through 2005 and into early 2006. Christof Winkelmann: The overall result will be positive, but it is difficult to predict where we will end up. Despite some skepticism about the magnitude of the upturn that many sources in the industry are predicting, I believe that the underlying economics warrant an increase in RevPAR of around 6% to 7% for the year. With cost structures having been reworked continuously over the past three to four years, such an increase in RevPar should show disproportionably higher net incomes. To say that we would achieve pre-2000 levels this year would seem very optimistic and is not supported by the current hotel data and information available to us. Butler: What is happening with prices and cap rates? Rich Conti: I ask all of you, "Do you want to buy a hotel?" So do all of the opportunity funds. Accordingly, cap rates have been driven downward, so they will continue to be low on good properties in good markets. The market will remain heated in the hunt for a great deal. Just be prepared to pay up. Jonathan Roth: I agree with Rich. More assets are being placed on the sale block as sellers continue to take advantage of ever-decreasing cap rates driven by the low cost and tremendous availability of capital. A lot of capital has been raised for hospitality assets and the managers of that capital are under pressure to deploy it. I sense that this trend will continue through this year, as long as no single event, like 9/11, causes a significant and immediate negative impact in the hospitality industry. Baltin: Jim, cap rates are indeed

at a low point not seen in recent years and may rise modestly over the

next year, but not to any substantial degree. The bigger question is: Are

they low due to low interest rates and limits on alternative investments

or is the traditional spread between hotels and other forms of real estate

decreasing?

. .  In the first three quarters of 2004, there were more than 75 transactions for more than $10 million in the United States. Highland Hospitality has been the most active buyer with eight significant single-asset acquisitions, followed by HEI Hospitality Fund with five, and Host Marriott with three. Host Marriott has also been an active seller of significant single assets with four this year, followed by Fairmont Hotels & Resorts and HBE Corp. (Adams Mark) with two significant single-asset dispositions each. Viewed by transaction size during this time period, three of the top 10 single-asset hotel sales occurred in New York (the Plaza Hotel at $675 million, Mayflower Hotel at $401.5 million, and Paramount Hotel at $128.5 million). Two significant single-asset hotel sales occurred in Wailea, Hawaii: namely, the Fairmont Kea Lani Maui at $355 million and the Four Seasons Wailea at $280 million. And from the perspective of price per room, during this period two of the top 10 single-asset hotel sales occurred in New York (the Mayflower Hotel at $1.1 million per room and the Plaza Hotel at $838,5000 per room), followed by two in Wailea, Hawaii (the Fairmont Kea Lani Maui at $788,900 per room and the Four Seasons Wailea at $742,700 per room. It is interesting to note that both the Mayflower Hotel and the Plaza Hotel have reportedly been purchased for residential conversions. In terms of property size�number of rooms�the top 10 single-asset hotel sales all had 600 rooms or more. The Las Vegas Hilton was the largest hotel to be sold at 2,950 rooms, followed by the Hyatt Regency Capitol Hill Washington, D.C. at 834 rooms, the Plaza Hotel in New York at 805 rooms, and the Westin Michigan Avenue Chicago at 751 rooms. During 2004, there have been several notable mergers and acquisitions, with Blackstone taking the lead, having acquired Extended Stay America, Prime Hospitality Corp., and Boca Resorts Inc. Look for public and private investors such as Ashford Hospitality Trust, Highland Hospitality, MeriStar Hospitality, Host Marriott, HEI Hospitality, Blackstone, and DiamondRock Hospitality to be active acquirers of single-asset hotel properties, as well as portfolios of hotels. Furthermore, look for entities such as Host Marriott, InterContinental Hotels & Resorts, Blackstone, and Strategic Hotel Capital to continue to prune their portfolios and dispose of non-core hotel assets. Unprecedented Abundance of Capital? Abrams: The year 2004 saw an unprecedented abundance of capital, both debt and equity, chasing the hotel sector. This will continue because of the strength of the industry and because of investors� new-found respect for real estate as an investment class, and hotels, in particular. Capital providers have become extremely aggressive�cap rates have tightened, spreads have tightened and loan-to-value levels have increased. Since I am optimistic about the industry, I think that the capital providers will continue to offer funds on a generous basis, but I do not think that there is room for purchasers or lenders to get much more aggressive. Essentially, for those looking for capital, this is as good as it is going to get. Winkelmann: I guess I am a little more cautious than the debt and equity players you see Dan, who apparently are getting more comfortable with higher prices and greater leverage. Other major lenders and owners of hotels in the United States that I talk with reflect a growing consensus that real estate prices, especially for hotels, are becoming inflated and difficult to justify in many circumstances. On the other hand, I do recognize that deals are getting done every day, but I am a little worried about the never-ending influx of capital, both on the equity and debt side to the hotel industry stemming in large part from non-traditional hotel investors and lenders. The major challenge for the industry in the future will be to live up to the optimistic predictions sweeping the industry. I do believe that 2005 will be a good year. But will it be as good as many assume? Roth: At Canyon Capital, we are observing with great interest the changes in providers and structure of capitalization for hotel transactions. Tremendous amounts of capital are now flowing for hospitality finance from new capital providers, particularly opportunity funds� mezzanine and equity programs and firms that were traditionally owners and operators of hotel assets, now with mezzanine funds for hotel financing. Unlike more traditional capital sources, these new providers of capital are much more comfortable underwriting the risks associated with hospitality lending. As a consistent provider of debt capital to the real estate industry, particularly in the hospitality arena, we find these to be welcome developments and we are proud of our ability to help our clients with their capital needs and by providing them new and creative ways to capitalize their transactions. What will be interesting to see is how these new market entrants behave when assets begin to experience trouble. Butler: Dan Abrams thinks that "this is as good as it is going to get" for construction financing. Although there is clearly more capital available today than in the past few years, and it may be reasonably ample for existing product, construction financing is still scarce. What is happening with construction lending? Baltin: Jim, a lack of construction financing and the substantial ADR declines from 2001 to 2003 have served to keep new supply down. There is, however, pent-up demand in some markets, as noted above, and a strong desire by the brands to increase distribution and rates are increasing. As a consequence, I expect construction financing to loosen up and supply growth to begin increasing. Jim Holliman: Well, Jim and Bruce, San Diego National Bank is one of the few exceptions in the hotel construction lending arena right now. In fact, since 1999, we have been a consistent lender for hotel construction projects all over the United States. We can handle project sizes from the fairly small to the very large. In fact, we have several very large projects that will break ground in the first quarter of 2005. We are not looking for "commodity" lending, where rate is the most important factor. We are competitive, but we want to provide capital where we can earn a premium from our ability to understand hospitality product quickly and assess the risk�bridge loans and construction lending provide that opportunity for us. We like full-service hotels in large metropolitan areas or in irreplaceable locations and great sponsorship. In 2004, the two primary areas in hospitality that many developers focused on were hotels with condos and the rehabilitation of historic buildings into hotels. We see that trend continuing in 2005, or even accelerating, and we like this kind of product as well as the traditional varieties of branded hotels. What Appears in Your Crystal Ball? Butler: All of you share a certain sense of optimism for the hospitality industry. Limited supply increases coupled with higher demand will restore the industry into great shape. What is on the horizon for your companies? Reynolds: Jim, our company is in the midst of significant value enhancing and positioning renovations to our portfolio of luxury class hotels, to be completed this year. We are only looking at selective acquisitions of upper-scale hotels that are located in major urban centers or destination resort markets. Blackham: Hotel-by-hotel analysis to determine the steps or investment required to retain and expand our customer base will be an ongoing process for our company. The objective is to maintain a RevPAR yield index of No. 1 or No. 2 in our competitive sets and look out between two and three years to project what is required to maintain this position. Engel: We will continue to do increasing amounts of international investment advisory work in addition to working with our important U.S. investor clients. If someone told me 24 months ago that we would be doing daily advisory work on behalf of clients around the globe, I never would have believed them. But the world more than ever seeks experienced advice and direction. And TRE�s principals have that experience to offer. Regarding myself, I will spend a week in an Italian cycling guide school course so I can eventually live out my fantasy of living in Italy and being a "guida" part time. Roth: In 2004, through our equity and debt programs, Canyon deployed in excess of $300 million in capital with approximately $125 million of which is devoted to hospitality assets. We will continue to deploy capital within the hospitality industry, focusing on value-added repositioning opportunities. Winkelmann: All in all, we are positive about 2005. As a hotel lender, it is critical to focus on the underlying asset, location and quality of sponsorship, rather than being influenced greatly by industry perceptions, which are not always proving themselves as correct. This means that one should not go wild when everybody else does, just as one should not cease activity in the difficult times as many players do. Aareal has consistently provided senior debt financing for the hotel industry in good times and bad. We continue to be a steady provider of capital today and will do so in the future. Many of our good clients have valued this relationship, new ones have been established and only a few have proven to be "one way" relationships. Holliman: The most active developers that we see in the market are large institutional investors, pension funds, and wealthy individuals. These are normally the only groups that can meet most lenders� equity requirements. However, these equity requirements might loosen a little bit, especially if more financial institutions enter this segment. Butler: Thank you for your views and perspectives. It looks like

the growth that we saw in 2004 in the hospitality industry will continue

in 2005. RevPARs and ADRs are likely to continue upward and prospects are

good for continued longer term growth.

The Global Hospitality Advisor ® is published four times a year for the clients, business associates and friends of Jeffer, Mangels, Butler & Marmaro LLP. The information presented in this newsletter is intended as general information and may not be relied upon as legal advice, which can only be given by a lawyer based upon all the relevant facts and circumstances of each particular situation.

|

|

Jeffer Mangels Butler & Marmaro LLP 1900 Avenue of the Stars, 7th Floor Los Angeles, CA 90067-4308 Attn: Jim Butler 310.201.3526 � 310.203.0567 fax [email protected] http://www.jmbm.com The premier hospitality practice in a full-service law firm |