|

|

|

|

|

|

|

Investment Review May 2003 |

| By Anwar Elgonemy, Jones Lang LaSalle Hotels

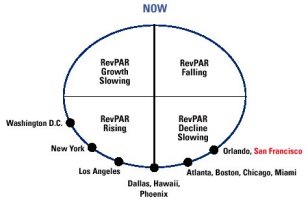

June 2003 The Investors Choice The set-backs to San Francisco�s economy have been well chronicled. Its underlying fundamentals are so compelling that it ranks as one of the nation�s key "buy" markets. It is down, but not out. The San Francisco Bay Area is comprised of nine counties of over 6.8

million people with the nation�s highest household income. The region benefits

from its top universities, an innovative business community and its natural

beauty. The city of San Francisco is recognized as an international business

center, the financial hub

Hotel Investment Opportunities in 2003

The Bay Area, headquarters to 25 of the nation's leading Fortune 500 companies, already has the world-class infrastructure and economic base in place to facilitate the upcoming recovery. As the regional economy recov-ers, the Bay Area is expected to once again attract a highly educated and affluent work force in the technology, finance, biotech, and the law sectors, all potential demand generators for the area�s hotel markets. San Francisco Bay Area

.

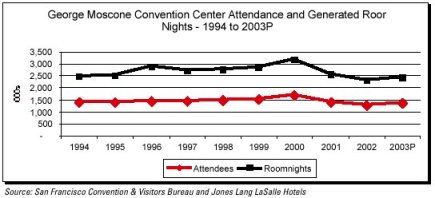

Source: Jones Lang LaSalle Hotels Relief Is On the Horizon According to the San Francisco Convention & Visitors Bureau, the

Moscone Expansion Project is currently underway and expected to be completed

by July 2003. The project involves an addition of approximately 300,000

square feet of net meeting space divided among 38 meeting rooms increasing

the Moscone Conventions Center�s total capacity to close to 902,000 square

feet of net exhibit/meeting/banquet space upon completion.

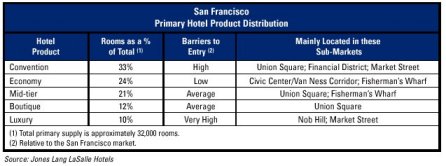

Inventory The San Francisco MSA hotel market consists of approximately 49,000 rooms in 360 properties. The market area includes the City of San Francisco, as well as San Mateo County to the south and Marin County to the north. The distribution of the market�s room inventory is presented in the following table. Convention center hotels, comprising approximately one-third of the

city�s total room inventory, dominate the San Francisco hotel market. The

luxury hotel segment, in turn, has the lowest share of product, but boasts

the highest barriers to entry.

As a percentage of total major-brand hotels, the market leader in the city is Marriott with a 13.6 percent market share, followed by Holiday Inn, Hilton and Hyatt. Some of the brands still not represented in San Francisco include Embassy Suites, J. W. Marriott, Sofitel, Sonesta, Swissotel and Raffles. San Francisco Major Hotel Brands

Source: Jones Lang LaSalle Hotels New Supply Seven hotels with a total of 1,994 rooms opened in San Francisco between 1999 and 2002. Only two properties are currently under construction, the 252-room Argonaut and the 276-room St. Regis Hotel, both expected to open by the end of 2003. Carpenter & Co. is building the St. Regis Tower, which includes 100 condominiums atop the 276-room Starwood-brand hotel. Hotels with condominiums are common on the East Coast, but have only recently arrived to the western United States. San Francisco

There are seven proposed hotel development projects in various planning stages in San Francisco with a total of 2,715 rooms. These are summarized as follows. , Planned/Proposed Hotels

Despite significant barriers to entry, and as presented earlier seven (and one expansion) were already added to the city�s inventory over the last four years. Given the current uncertainty in the lodging and capital markets, it is unlikely that the planned/proposed properties with a total of 2,715 rooms will materialize, supporting the notion that the San Francisco hotel market wil not be in a position to absorb additional new supply until 2006 at the earliest. Foster City Enterprises� Bloomingdale's hotel project in San Francisco, which Le Meridien was pursuing, has been abandoned due to financing challenges. Forest City still has the planning/building rights for a large mixed-use development project on Market Street in San Francisco, including a 365,000-square-foot Bloomingdale's, 375,000- square-foot of upscale shopping, 235,000-square-feet of Class A office, and a 435-key hotel. Market Performance Levels

Factors indicating that San Francisco�s performance will once again strengthen include the following:

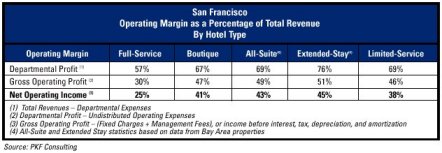

With high payroll costs, operating margins for San Francisco hotels

tend to be slightly lower than other cities in the U.S., especially for

full-service properties, which are further "burdened" by food and beverage

operations. Boutique hotels and extended-stay products tend to fare much

better.

Hotel Development A major wave of new hotel development took place in the San Francisco Bay Area during the halcyon years of 1998, 1999 and 2000. New construction is virtually at a standstill given the dismal market conditions. One of the most recent properties to be built in the Bay Area was the 280-room Hilton Santa Clara, which opened in December 2000 at approximately $118,000 per key in development costs. The Four Seasons in East Palo Alto is currently under construction at $1.1 million per key. San Francisco Bay Area

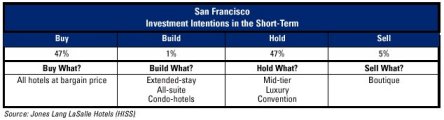

(2) Includes land costs and construction costs for 285 hotel rooms, 200 luxury condominiums, a 100,000-square-foot spa, 60,000 square feet of retail space, and 20,000 square feet of food and beverage outlets. * Planned, proposed or under construction. Transactions While investors are currently negative concerning the short term trading performance of San Francisco, reflective of its exposure to the tech sector, the city is among the top five markets expected to enjoy the largest turnaround in trading performance between the short and medium term. Given San Francisco�s longstanding prominence in the convention and leisure travel segments, the current decline is not expected to presage an enduring collapse like the 1980s. In a show of confidence in the stability and long-term strength of the

market, and according to the most recent Hotel Investor Sentiment Survey

(HISS) by Jones Lang LaSalle Hotels, approximately 47% of investors indicated

that they want to buy hotel assets in San Francisco. However, as it takes

both a motivated buyer and seller to execute a transaction, sellers in

San Francisco are still scarce.

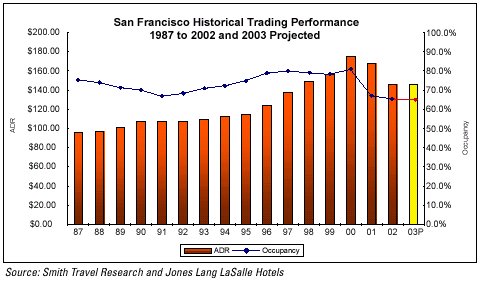

Major transactions in the San Francisco hotel market between 1998 and mid-2001 indicate that the highest price per key recorded during that period was for the sale of the Ritz-Carlton ($479,200 per room), with the average price per key at approximately $255,000, one of the highest in the nation. The average initial yield for new acquisitions in San Francisco at the beginning of 2003 is close to 9.6%, the average leveraged IRR is currently close to 21%. San Francisco

With the July 2002 sale of the Courtyard by Marriott being the most recent major deal in the city, the hotel transaction market is just beginning to come to life. Kimpton Hotel & Restaurant Group, a San Francisco-based owner/operator of boutique properties, is selling five of the 16 San Francisco properties it runs. In addition, the Pan Pacific is currently on the block. Pertaining to the Courtyard by Marriott transaction, CNL acquired a 50 percent interest in the property through a joint venture with an affiliate of Marriott International. This joint venture financed the $82 million acquisition with equity investments of $13 million from each of CNL and Marriott, as well as $41 million of borrowings from a third-party lender, and $15 million of mezzanine financing provided by Marriott. CNL then leased the property to a subsidiary organized to qualify as a taxable REIT subsidiary (TRS), which entered into a long-term management contract with Marriott International. In San Francisco, as in other markets nationwide, the funding void left by the absence of Wall Street will continue to be filled mostly by private equity and institutional capital. Increasingly, investors are discovering that hotel real estate investments held by private equity funds hold a number of advantages. First, they generally provide investors with relatively steady cash flows while also taking advantage of many of the tax-efficient features of real estate investing, namely significant depreciation and interest expense write-offs, while freeing investors from the hassle of owning and managing real estate assets. Second, with properly placed investment choices, lodging real estate investments often can yield significant asset appreciation. Although hotel financing in the Bay Area is extremely difficult to attain, lenders are still providing leverage and borrowers who have experience will find financing much easier to obtain. For example, Jones Lang LaSalle Hotels recently secured a construction loan for mixed-use luxury development in northern Napa Valley. In San Francisco, a city celebrating both shrewd finance and high romance, it is evident that until the overall economic conditions improve, many hotel investment groups will continue to hold off on their strategic real estate decisions. All variables considered, San Francisco will always be a world-class destination that offers its business and leisure travelers tremendous variety. However, San Francisco has demonstrated over the last two years that, albeit diverse, it has an extremely cyclical hotel market, lacking the depth of such cities as New York City or London. The coming months will be, without doubt, telling in terms of whether the San Francisco lodging market has actually "bottomed-out", or whether the worst has yet to come in light of current geopolitical events. All hopes are on the former, not the latter, with "survive until 2005" being the underlying motto. About the Author

Jones Lang LaSalle Hotels is the largest and most qualified specialist hotel investment banking services group in the world. Through our 18 dedicated offices and the global Jones Lang LaSalle network of 6,000 professionals across more than 100 key markets on five continents, we are able to provide clients with value-added investment opportunities and advice. In 2002, our success story includes the sale of 6,474 hotel rooms to the value of US$862 million in 36 cities and advisory expertise on 116,877 rooms to the value of US$17.8 billion across 170 cities. The majority of active investors worldwide have bought or sold hotel and tourism real estate through Jones Lang LaSalle Hotels, taking advantage of our extensive professional relationship and innovative strategies. Our experience and success also extends to the other services, including mergers and acquisitions, valuation and appraisal, asset management, strategic planning, operator assessment and selection, financial advice and capital raising, and industry research. |

|

Anwar R. Elgonemy Jones Lang LaSalle Hotels One Front Street, Suite 300 San Francisco, CA 94111 DIRECT LINE: (415)699-3347 FAX: (415)421-7736 [email protected] www.joneslanglasallehotels.com |

| Also See | The

San Francisco Hotel Investment Climate in the Post-Tech Boom Paradigm

/ Anwar Elgonemy / Oct

2002 |

| Debt Financing Alternatives & Debt Restructuring Strategies in the Lodging Industry / Anwar R. Elgonemy / Sept 2002 | |

| Concrete to Cash: Real Estate Sale-Leasebacks in the Lodging Sector / Jones Lang LaSalle Hotels / March 2002 | |

| The Dynamics of a Hotel Deal in Mexico / Jones Lang LaSalle / July 2002 |

Anwar

Elgonemy is an Associate in the San Francisco office of Jones Lang LaSalle

Hotels who has extensive lodging investment experience throughout the Bay

Area and Northern California. He has been involved with notable area assets

such as the Hilton Hotel & Towers, Renaissance Parc 55, Claremont Resort

& Spa, and the Ritz-Carlton Half Moon Bay. Elgonemy�s Northern California

client base has included Citibank, Clement Chen & Associates, HCV Pacific

Partners, Kimpton Hotels & Restaurant Group, The Pebble Beach Company,

Stanford Hotels Corporation and Tokai Bank, among others. Elgonemy

is both a licensed commercial real estate appraiser and a sales agent.

He is regularly quoted in the San Francisco Business Times and the San

Francisco Chronicle, and has provided industry insight to a number of San

Francisco television channels such as CNN's local edition, KRON and Fox

News.

Anwar

Elgonemy is an Associate in the San Francisco office of Jones Lang LaSalle

Hotels who has extensive lodging investment experience throughout the Bay

Area and Northern California. He has been involved with notable area assets

such as the Hilton Hotel & Towers, Renaissance Parc 55, Claremont Resort

& Spa, and the Ritz-Carlton Half Moon Bay. Elgonemy�s Northern California

client base has included Citibank, Clement Chen & Associates, HCV Pacific

Partners, Kimpton Hotels & Restaurant Group, The Pebble Beach Company,

Stanford Hotels Corporation and Tokai Bank, among others. Elgonemy

is both a licensed commercial real estate appraiser and a sales agent.

He is regularly quoted in the San Francisco Business Times and the San

Francisco Chronicle, and has provided industry insight to a number of San

Francisco television channels such as CNN's local edition, KRON and Fox

News.