|

|

|

|

|

|

|

|

9.6% in 2002, This After a 19.4% Decline In 2001 PKF Consulting-HRG Annual Hotel Trends Report |

| Atlanta, GA, April 16, 2003 � The average U.S. hotel suffered a second

consecutive year of declining profits in 2002, according to the 2003 edition

of Trends in the Hotel Industry-USA, published by PKF Consulting and the

Hospitality Research Group (HRG). PKF Consulting and HRG announced

the availability of the latest annual Trends report today (www.hrgonline.com).

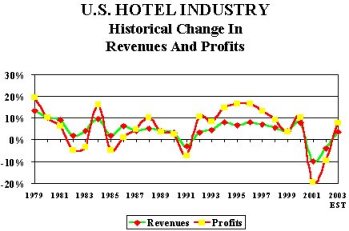

According to the Trends report, the operating profit for the average U.S. hotel dropped 9.6 percent in 2002, this after a 19.4 percent decline in profits in 2001. This marks the first consecutive year decline in hotel profitability since the years 1982 and 1983. On the bright side for hotel owners and operators, HRG projects that U.S. lodging industry performance will improve by year-end. With leading economists forecasting an economic rebound after the Iraq War is settled, current HRG projections call for a 3.6 percent increase in hotel revenues in 2003. This increase in revenue should result in a 7.8 percent increase in profits for the average U.S. hotel for the year. The 2002 results come from the firm's recently completed annual Trends in the Hotel Industry survey, an annual review of U.S. hotel operations conducted since 1935. This year's sample draws upon year-end 2002 financial statements from 4,000 hotels across the country. Profits are defined as income after management fees, property taxes, and insurance, but before capital reserves, debt service, rent, income taxes, depreciation, and amortization. New Expense Cuts Hard To Find �With all the fear over a potential war with Iraq, early into 2002 we were projecting an 11.0 percent decline in hotel profits for the year. Therefore, the 9.6 decline did not come as a surprise,� says R. Mark Woodworth, Executive Managing Director of Atlanta-based HRG. �Expecting profits to be down, hotel operators continued the strict cost control measures implemented in 2001.� After feeling the dramatic negative effects of the September 11 terrorist attacks and recession in 2001, hotel managers cut their costs dramatically. In 2001, total operating expenses declined 5.3 percent, including a 6.6 percent cut in labor costs. �With all the expense cutting done in 2001, there was little fat left in the 2002 operating budgets of U.S. hotels,� notes Woodworth. Because expenses were cut so much in the prior year, hotel managers

were challenged to find additional cost saving measures in 2002.

In response to a 4.0 percent decline in total revenue in 2002, hotel managers

were only able to muster a 1.8 percent cut in expenses.

Ironically, one reason for the difficulty in finding expenses to cut was the moderate decline in occupancy. The average hotel in our 2003 Trends sample suffered a 4.7 percent decline in rooms revenue, the result of a 0.8 percent decline in occupancy and a 3.9 percent decline in average daily rate. �For the most part, the hotels in our survey sample did not lose that many customers. The number of properties that were able to achieve an increase in guest count in 2002 was just slightly less than the number of hotels that accommodated fewer guests,� says Robert Mandelbaum, Director of Research Information Services for HRG. �Given this relative stability in occupancy, hotel managers needed to spend the associated variable expenses required to service their guests.� The most observable example of a variable hotel expense is labor costs. Labor costs constitute 43.7 cents of every dollar spent to operate a hotel. �Historically, hotel managers have made deep cuts payroll in response to declines in revenue,� says Mandelbaum. �However, in 2002, relatively stable occupancy, combined with a desire to preserve guest service, resulted in a decline of only 0.2 percent in hotel labor costs.� Some Expenses Go Up Further evidence of hotel managers� efforts to attract new customers,

while satisfying their existing guests, are the increases in both maintenance

and marketing expenditures.

In 2002, hotel managers spent an average of 1.2 percent more to market their hotels than they did in 2001. This figures includes all on-site marketing efforts, but does not include any fees paid to franchise organizations or referral services. �If you examine the details of the marketing expenditures in 2002, you find that sales and marketing payroll was flat compared to 2001,� says Woodworth. �Therefore, the entire 1.2 percent increase in marketing expenses went towards advertising, merchandising, and other direct promotional efforts.� Despite declining revenues, U.S. hotels did increase the amount they spent to maintain the hotel building, furniture, fixtures, and equipment. Property operations and maintenance expenditures increased 1.7 percent in 2002. �Even in difficult market conditions, hotel owners and operators know that they need to maintain the physical product in order to retain market share and preserve asset value,� notes Mandelbaum. Insurance Takes A Big Bite The single largest increase in hotel operating costs during 2002 was insurance. The average U.S. hotel had to spend 33.1 percent more in 2002 in order to insure the contents and structure of their building, as well as business liability. This comes on the heels of an 18.9 percent increase in 2001. �Ever since September 11, 2001, our clients have been telling us about the staggering increases in premiums they�ve had to pay,� says Woodworth. �This is one of the biggest increases in any one individual expense item that we�ve seen in the 67 years our firm has been tracking U.S. hotel operating performance. From what we�ve heard, this trend of increasing insurance premiums appears to have carried forward into 2003.� Energy Relief After much concern regarding the rise in energy costs in 2001, U.S. hotels saw some relief in 2002. The average U.S. hotel spent 5.5 percent less in 2002 than they did in 2001 to provide electricity, gas, steam, fuel and/or water for their property. �We attribute the decline in utility costs to a combination of a drop in energy prices, as well as improved conservation measures by hotel managers,� says Mandelbaum. �However, we have heard from some hotel managers that their utility bills have begun to creep up during the first quarter of 2003.� Reversal Of Fortune While all hotel categories suffered drops in both revenue and profits in 2002, the magnitude of decline in performance did vary by property type. Of all the different hotel categories, convention hotels experienced the smallest declines in revenues (2.6 percent) and profits (5.4 percent). Limited-Service hotels, on the other hand, endured the greatest fall-off in revenues (5.7 percent) and profits (12.7 percent).

Source: The Hospitality Research Group of PKF Consulting -- �The relative insulation enjoyed by limited-service hotels in 2001, as well as the hard hits experienced by convention hotels, were short lived,� says Woodworth. �In 2001, tight personal and corporate budgets forced travelers to trade down from high-priced full-service properties to more moderate priced limited-service hotels. In 2002, discounting appears to have enabled rate sensitive travelers to think about trading back up. In turn, managers at the higher priced properties were able squeeze as much profit from their stabilized top-line situation and minimize their decline in profitability.� �While profits have fallen for all property types, the average profit

margin for the properties in our sample was 27.5 percent,� says Woodworth.

�This is nearly two full percentage points greater than the 25.6 percent

average margin achieved by U.S. hotels from 1960 through 2001. Hotel

owners and operators certainly don�t like to lose ground, but they are

not losing money.�

The Importance of Benchmarking While HRG is projecting growth in revenues and profits for the average hotel in 2003, these increases will not come automatically for each and every property. �Changes in travel patterns, budgets, insurance and utility expenses, and distribution channels will provide significant challenges in 2003,� says Woodworth. �Throughout the year, hotel owners and operators will want to know why their hotel is, or is not, benefiting from the rise in market performance. Proper top- and bottom-line benchmarking is required to answer this question.� In response to this increased demand for revenue, expense, and profit information, HRG offers its clients Benchmarker, a service that allows hotel owners and operators to compare the financial performance of their properties against a select group of comparable properties. Hotel owners and operators interested in HRG�s Benchmarking products can contact Claude Vargo at (404) 842-1150, ext 237. To order a copy of the 2003 edition of Trends in the Hotel Industry,

call (404) 842-1150, ext 237, or visit the HRG website at www.hrgonline.com

(see Publications and Data).

|

###

|

Gary Carr Director of Communications PKF Consulting c/o Rising Moon P.O. Box 683 Clayton, CA 94517 (925) 672-8717 [email protected] Mark Woodworth

|