|

|

|

|

|

|

|

|

| Jones Lang LaSalle Hotels, October 2002

The People�s Republic the world�s most populous nation, also has one of the world�s fastest growing economies. Such characteristics have made it the focal point of Asian investment. There is a definite trend in foreign investment away from South East Asia to China. This fundamental shift in the economic composition of Asia will continue to have implications for the hotel sector, not just within China but across the entire region. Driven by the desire to benefit from an increasingly affluent domestic population as well as the influx of foreign corporate travellers, hotel investors, developers and operators alike are currently scrambling for market presence in China. With China�s recent entry to the World Trade Organisation and Beijing�s successful bid for the 2008 Olympic games providing renewed impetus in the push for market presence, it is timely for all participants to take a step back and consider the fundamentals of hotel operation and investment markets in China, especially in the key centres of Beijing and Shanghai. This edition of FocusOn aims to do just that. ECONOMIC OVERVIEW Since economic liberalisation commenced in 1978, China�s average income has reportedly increased sevenfold and its GDP has quadrupled. During 2001, despite the global economic slowdown and its neighbours � Singapore and Japan being in recession, China posted GDP growth in excess of 7% to become the sixth largest economy in the world. The latest data indicates a continuation of this trend, with growth strengthening to 8% during the year to June 2002. Since 1998, China�s economy has been fuelled by the government�s expansionary fiscal and monetary policies, borrowing heavily to sustain the country�s growth. The economy has recently been boosted by government investment in fixed assets and large-scale construction, but analysts are unsure if this will be enough to offset a possible weakness in exports, which first started softening in Q4 2001. During March 2002, the Chinese government announced plans for another massive bond issue worth USD18.3 billion to fund more government spending in infrastructure and other public works. During 2001, the slowing economy and reduction in cross-border mergers and acquisition activity meant foreign direct investment (FDI) across the globe declined by nearly half. However, foreign investment to China increased by 14.9% to reach USD46.8 billion. Foreign investors, who now account for over half of China�s exports, are attracted to China because of the growing domestic market, cheap land,concessional tax rates, low labour costs, increasing integration in the Greater China region and the stable political and economic environment. FDI inflows have played a key role in job creation, domestic demand and export growth. It is expected that rather than rely on export driven growth in the future, Chinese policies will seek to stimulate domestic demand, encouraging home ownership and spreading economic growth to the western provinces. Mortgage financing has recently become available in China and is considered a stimulant for the housing market. However house and car loans are still in their infancy. In February 2002, policy makers announced rate cuts of 0.25% on deposits and 0.5% on lending. The cuts, the first to be made since June 1999, were made in order to stimulate the economy and improve employment. However, as China�s economy is still progressing from the centrally planned model to a market economy and investment and saving decisions remain relatively inelastic, these cuts are not likely to be as successful in propping up the economy as in the US experience. The stimulation of the domestic economy is hindered by China�s deflating retail prices, which encourage Chinese people to postpone major purchases rather than spend. During 2001, consumer prices increased by 0.7%, but the retail price index fell by 0.8%. Given the government�s housing and education reforms, there is now even more incentive to save for the future rather than spend. Unemployment is also a concern of the Chinese government. Official urban unemployment rate stands at 3.0%, but many believe the true rate is three times this level. LIKELY IMPACT OF WTO ENTRY China joined the World Trade Organisation (WTO) on December 11 2001. As a result, tariff rates on more than 5,300 duties will be reduced, the average of which will reduce from 15.3% to 12% by the end of 2002. In addition to the reduction of tariffs, China must undertake other reforms which will open up many of the country�s markets to foreign interest. Although the precise implications of China�s entrance to the WTO are unknown, most agree that there will be some short term challenges to face before the long term benefits crystallise. While China�s accession to the WTO benefits its reform process and economic development as a whole, less competitive industries, such as small farming operations will suffer as protective tariffs are removed and they are forced to compete with international players. In the first 10 days of initial tariff reductions, the level of car imports rose 37%. Consequently, there is likely to be a shift of resources away from protected industries to those where China has a comparative advantage. Sectors likely to suffer most are agriculture, telecommunications, banking sectors, and capital intensive sectors such as car manufacturers, steel, petrochemical and machinery. The banking system may find it difficult to compete with foreign banks due to the high level of non-performing loans, high cost to income ratios and low capital adequacy. Export oriented industries, such as textiles and electronics are likely to be the winners. Following on from this, there is likely to be a fundamental shift in income distribution and a movement in population away from the rural areas, as ex-farmers move to the cities seeking employment. The exact level of job displacement is debatable. According to the Beijing Morning Post, 11 million jobs will be lost, while 12 million jobs will be created as a result of China�s accession to the WTO. However, the Chinese government was more pessimistic, warning that China could lose 20 million farming jobs over the next several years. The difficulty is that the jobs created are more likely to be those that require educational qualifications, while the unemployed will mostly be unskilled workers. Consequently, there is concern that China will suffer from a bi-polarisation of wealth and widening income disparity between the eastern coastal regions and the hinterland provinces, which may in turn, cause social problems. China�s 12 coastal provinces already account for 90% of the country�s exports and FDI. Most analysts agree that an annual GDP growth in excess of 7-8% is essential to prevent social inequality arising from income disparity. It is believed that at this level, economic development will trickle down to all members of society, including the displaced workers. A recent report by Lehman Brothers predicted China�s economy would grow by 6% pa over the next 20 years provided the necessary reforms were undertaken. These reforms include the provision of a social security framework, restructure of state companies and setting in place methods by which the country can manage the rapidly urbanising population. According to the latest Consensus Economics survey, economic forecasters expect China�s real GDP to grow by 7.3% during 2002 and 7.7% during 2003. Western commentators believe China�s entrance to the WTO will result in an increase in the size of the middle class as the country becomes more wealthy, which in turn may fast track democratic reform. According to the Chinese Academy of Social Sciences, the middle class only comprises 15% of the total population at present. Although this is a long way from US�s 60%, it still represents a staggering 110 million people. There are conflicting forecasts of the growth of the middle class, defined as the people that can afford to buy cars, purchase houses and take leisure vacations. Some say they will reach 200 million by 2005, while others say the urban unemployment, rural underemployment and depressed incomes will constrain it to remain closer to 100 million. As more multinationals set up manufacturing bases in China, FDI is expected to grow up to as much as 16.0% pa for 2002-06, to reach USD100 billion in 2006. This is set to boost domestic competition, raise the skill level of the population, improve the quality of available technology, accelerate structural reform and result in higher efficiency and higher productivity. Nomura Asia predicts foreign trade will double to more than USD1,000 billion by 2006, with exports growing by 15.0% annually during 2002-2006. The World Bank estimates China will account for 6.8% of world exports and 6.6% of imports by 2005, representing growth of 2.0% and 1.3% respectively. However, China must increase the transparency in pricing and subsidies. As far as tourism is concerned, China�s relevant commitments are:

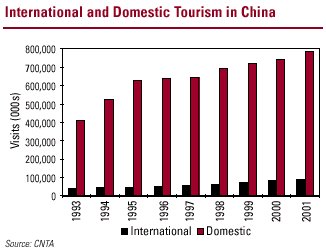

As Premier Mr Zhu Rongji stated, �Whether the gains are larger than the losses will depend on our work�. No one is sure what the net effect will be,but,one thing is certain � the process will be eagerly analysed around the world. INTERNATIONAL AND DOMESTIC TOURISM IN CHINA The growth of China�s inbound tourism market appears to have matched its economic growth and has consistently outstripped the world wide average. Between 1990 and 2000, international visitor arrivals to China increased by an average of 11.8% pa, while global tourism grew by a modest 4.3% pa. During 2001, the disparity was magnified. In the face of a global decline of 1.3%, international visitor arrivals to China increased by 6.7% to reach 89.0 million. This growth continued into the first six months of 2002, with international arrivals increasing by 9.4% over the six months to June 2001. The World Tourist Organisation recently announced that China was set to overtake Italy, US, Spain and France and become the top destination by 2020, attracting 130 million international visitors.

expenditure of 2000. Arrivals from Hong Kong dominate the Chinese market, accounting for 65.8% of total visitors to China. Macau and Taiwan follow with 17.7 % with 3.9% respectively. Japan and Korea dominate the foreign market accounting for 22.7% and 16.0% of total foreign arrivals respectively. Other key source markets include Other Asia, Europe, Russia and the US. China�s domestic tourism has grown at a slower rate than international tourism, increasing by an average of 8.4% pa since 1993. During 2001, domestic visitors grew by 5.3% to reach an all time high of 784.0 million, while domestic tourism receipts increased by 10.5% to reach USD60.2 billion. The China National Tourism Administration expects domestic tourist numbers in China to increase by 3.3% and reach 810.0 million during 2002.

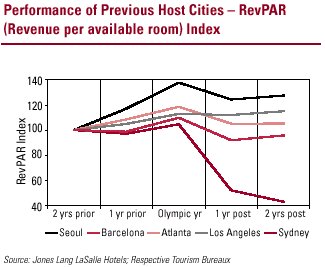

Impact of the Beijing 2008 Olympics Beijing�s role as the host of the 2008 Olympic Games provides the city and China with exceptional opportunities, particularly in relation to marketing. As well as benefiting from the direct impact of visitors, athletes and media generated by the two-week Games period, the city and nation is also likely to benefit from exposure to a worldwide television audience of four billion. The Olympics is also expected to leave a legacy of world class sporting, tourism and general infrastructure, while the convention and events market should profit as the 2008 Olympics demonstrate China�s ability to host major world class events. Looking at the experience of the previous five host cities, the following observations can be made:

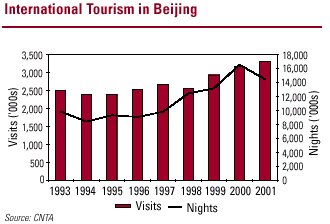

CITY HOTEL MARKET PROFILES Beijing Beijing is China�s political and cultural centre. The city is home to cultural treasures including the Imperial palaces of the Forbidden City, the Great Wall and other historical sites such as the Summer Palace, Temple of Heaven, Ming Tombs and Beihai Park. In recent years, the city has grown tremendously. As increasing numbers of multinational corporations set up representative offices and headquarters in Beijing, the number of new mixed used developments incorporating significant office towers, residential blocks and hotels has also increased. Beijing�s estimated population is 12 million. As China�s political and cultural centre, Beijing attracts a large proportion of foreign and corporate travellers. In complete contrast to China as a whole, foreign visitors (excluding Compatriots) dominate the inbound market of Beijing, accounting for over 85.0% of total international visitor nights and visits. Beijing�s key foreign markets are Japan, the US and Korea. International tourism to Beijing is likely to experience strong growth over the medium to long term in view of the country�s recent accession to the WTO, greater trade liberalisation and its hosting of the Olympics. Many Fortune 500 companies have earmarked China as a key market and Beijing will benefit from this, thereby stimulating demand for upper tier hotel accommodation. Demand is also likely to be sourced from international law firms and other professional consultancies.

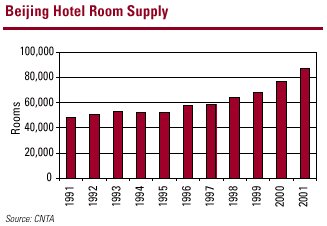

Hotel Supply According to China National Tourism Administration (CNTA), room supply growth in Beijing has accelerated over the the at 506 star rated establishments comprising 86,923 rooms, including 6,289 five star and 17,600 four star rooms. The upper tier market is currently the focus of the development activity in Beijing. Jones Lang LaSalle Hotels has identified three major five star hotels currently under construction and three four and five star hotels comprising 1,254 rooms presently in the planning stages. In addition, we have identified 344,600 square metres of floor area to be dedicated to serviced apartment development by 2005.

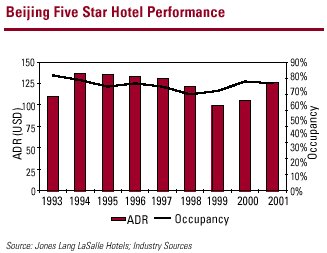

Hotel Performance � Five Star Market Demand for Beijing five star hotels has largely kept pace with supply additions over the past eight years, allowing occupancy to hover between 65-73% over this period. Since 1999, demand has grown at an average of 14.6% pa and has absorbed the new supply. Unlike most other cities in Asia, Beijing�s five star hotel market performance during 2001 remained largely stable despite the global economic slowdown and the events of September 11. Demand remained relatively strong and occupancy improved slightly due to a robust domestic economy and continued interest from multi-national companies looking to establish a presence in China. Beijing benefited from strong growth in demand from Hong Kong and Taiwan in particular, which substituted softer international corporate demand growth. Such a change in business composition to the more price sensitive Hong Kong / Taiwan source markets minimised the ability of hoteliers to increase five star rates. As a consequence, ADR declined by 0.3% to record USD102. Revenue per available room (RevPAR) increased slightly by 0.5% during the course of 2001. Data for the year to date June 2002 indicates five star hotels recorded an average occupancy of 66.2% and an ADR of USD108. In response to competition from new hotels and serviced apartments, several of the existing hotels are currently undergoing or planning for upgrades to rooms and public areas along with the installation of broad-band connectivity.

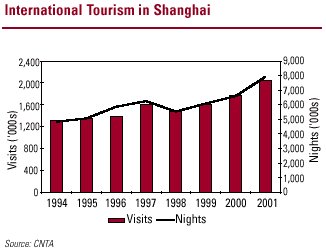

Shanghai The first Chinese port to be opened to Western trade, Shanghai is now one of the world's largest seaports. The city has long enjoyed the stature of being the financial, commercial and industrial centre of China and is today the home of China's first and foremost stock exchange, the Shanghai Stock Exchange. The city has also undergone extensive physical changes including the establishment of industrial suburbs and housing complexes, the improvement of public works, infrastructure development and the provision of parks and other recreational facilities. Shanghai has 11 million urban inhabitants. As China�s financial centre,Shanghai attracts a large proportion of foreign and corporate travellers, although Compatriot visitors still account for a quarter of the city�s international tourism. Increasing flight frequencies and direct flights from long haul destinations are also assisting Shanghai�s reputation as an international tourist destination. The city is increasingly popular as a weekend destination for Hong Kong, Taiwan and Korean residents. As with Beijing, Shanghai�s key foreign markets are Japan, the US and Korea. As Shanghai is at the forefront of China�s rapid business evolution and WTO initiated financial sector reforms, it is expected to attract an increasing percentage of international as well as domestic visitors. Strong demand for upper tier hotel accommodation is likely to come from the international financial and consulting sectors.

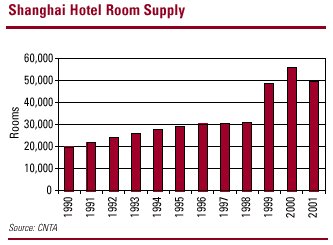

Hotel Supply According to China National Tourism Administration (CNTA), Shanghai�s room stock grew significantly during the 1990s from a base of approximately 20,000 rooms in 1990 to its present stock of 49,831 rooms. During 2001, five star supply was boosted by the opening of the 316 room Marriott Hongqiao and the 318 room St Regis in Pudong. In total, there were 7,306 five star hotel rooms as at December 2001. As with Beijing, the upper tier market is currently the focus of the development activity in Shanghai. However, there are substantially more developments currently under construction or in the planning stages in Shanghai. Jones Lang LaSalle Hotels has identified five major four and five star hotels currently under construction comprising 1,904 rooms and a further six hotels comprising a minimum of 1,971 four and five star rooms presently in the planning stages. If these supply additions come to fruition, total supply in Shanghai will increase by 7.8% by 2005, the five star room stock increasing by a significant 37.0%. This does not include serviced apartment developments which would also compete with hotels.

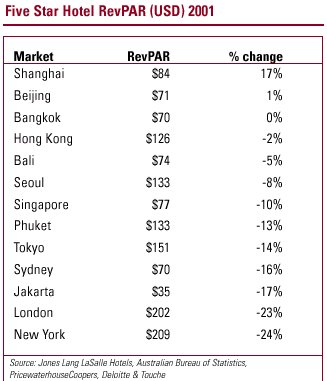

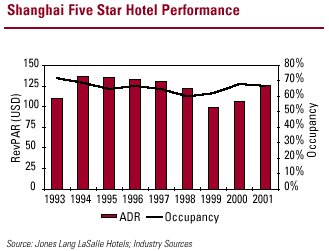

Hotel Performance � Five Star Market During 2001, Shanghai�s five star market was surprisingly resilient. Despite the supply additions, occupancy only fell by 1.8% and ADR surged by 19.1% to reach USD126. The ADR increase was largely due to the strong performance of the previous year and the lag in pricing decisions. Data for the year to date June 2002 was more positive than anticipated, with five star hotels recording an average occupancy of 75.7% and an ADR of USD137. The considerable new supply set to enter the market during 2002/03 should place some pressure on occupancies thereby limiting the operators� ability to push ADRs upwards. This will be particularly evident in the five star segment with an expected 1,904 rooms likely to open during the course of next 12 months. Major hotels currently under construction include:

Regional Operational Performance Comparison When comparing the performance of the five star markets of Beijing and Shanghai to the region, the strength of the performance during 2001 is obvious. During 2001, Beijing and Shanghai were the only two Asian markets to record growth during a year in which hotel operators had to contend with a global economic slowdown and the aftermath of September 11. The growth of the Chinese markets is testament to the strong domestic demand, as well as continuing foreign investment and the resulting international corporate demand for hotels in both markets. Despite this growth, Shanghai and Beijing are still competitively priced compared to other cities around the region particularly when measured against the key centres of Tokyo, Seoul and Hong Kong. When judged against the international gateway markets of London and New York, Shanghai and Beijing both represent low cost destinations with ADRs around 56-66% lower.

INVESTMENT MARKET Approval Process (Authored by Rico Chan and Simon Yim, Baker & McKenzie, Hong Kong SAR) The majority of internationally recognised hotels in China were established via a joint-venture (JV) ownership structure which in the past has required majority representation from local partners. As from China�s accession to the WTO on December 11 2001, foreign investors are permitted to take majority ownership in the construction and operation of hotels (including apartment buildings) and restaurant establishments. Within four years after China�s accession to the WTO, 100% foreign ownership in these projects will be permitted. In general, foreign investment projects in China require various approvals. The newly revised Regulations for Guiding the Direction of Foreign Investment (the �Foreign Investment Regulations�), and the Catalogue for Guiding Foreign Investment in Industry (the �Investment Catalogue�) which are both effective from April 1 2002, divide foreign investment projects into four categories, namely: �encouraged�,�permitted�, �restricted� and �prohibited�. Under the Investment Catalogue, foreign investment in the construction and operation of high-class hotels (four and five star hotels) falls within the �restricted� category. However, foreign invested hotel projects of three star or below are regarded as �permitted� projects. It is interesting to note that the Investment Catalogue currently does not restrict 100% foreign ownership in hotel projects. Based on the Foreign Investment Regulations, foreign-invested high-class hotel projects (as a �restricted� foreign investment project) are to be approved by foreign investment authorities at the provincial level. If the total investment of such high-class hotel projects exceeds USD30 million, approval at the central level will be required. Generally speaking, the tourism bureau and planning commission at the central or local levels will be involved in the approval of foreign-invested hotel projects. In general, foreign invested hotel owners and operators are subject to national and local enterprise income tax (�EIT�) at 33% of net income. Projects in �special economic zones� and �central and western region� of China may qualify for preferential tax treatments, such as a reduced EIT at 15% and waiver of local EIT. Presently, China has two distinct sets of EIT laws: one for foreign-invested enterprises (�FIEs�) and the other for Chinese enterprises. It has been widely reported that in the very near future the Chinese government may introduce a unified EIT rate applicable to all local and foreign businesses. It has been suggested that the unified EIT rate will be about 24-27%. It has also been suggested that the unified EIT rate would be generally applicable to the FIEs established in �special economic zones� and �central and western region�, and preferential tax rates would be granted according to the nature rather than the location of the projects concerned. Investment Environment Most of the local partners of foreign-invested hotel projects have been government related ministries or the PLA (People�s Liberation Army). This being the case, international standard hotels have been tightly held across China with few transactions taking place, mainly because investors are generally reluctant to invest in minority stakes. This is especially the case in an emerging and still largely unknown market such as China. This lack of hotel transactions may however change as the Chinese government implements reforms as part of WTO entry and attempts to reform its state owned enterprises and move the PLA away from such activities. Such reforms may present new investment opportunities as the financial, legal and political pressure on government enterprises and the PLA to divest increases. Transactions that have occurred to date have generally been off market or company level transactions rather than direct and transparent real estate deals. Two notable sales in recent times include the sale of the Sheraton Suzhou in 2001 and the Beijing Grace Hotel in 1997. Throughout the Asian economic crisis and now the global economic slowdown of 2001/02, hotel investors and operators have been prepared to overlook the difficult conditions in other parts of the world and push ahead with their expansion and investment plans in China. Motivated by perceptions of potential upside in the medium term, such a trend contradicts the otherwise cautious attitude that is currently prevailing in many other hotel markets around the world and demonstrates the determination of investors and operators alike to establish a presence in China.

Jones Lang LaSalle Hotel�s most recent Hotel Investor Sentiment Survey (HISS) indicates that both Beijing and Shanghai have some of the highest �buy� sentiment ratings across Asia, while both cities also rate quite high in the �build� sentiment category. Not surprisingly, both markets have low �sell� sentiment ratings. With the Chinese economy now dominating the growth outlook across Asia in particular, many investors from South-east Asia are keen to expand into China given the difficult economic conditions in their home countries. Despite the strong positive sentiment for foreign investment in Chinese hotel markets, few transactions have yet to materialise for the following reasons:

According to our research, Jin Jiang Holdings manages the largest number of hotel rooms across mainland China. Since the last survey in 2001, Accor Asia Pacific Corporation (AAPC) has more than doubled its presence in China, partly due to its April 2002 acquisition of the management of the Zenith Hotels International portfolio which included six hotels in China. AAPC has a further seven hotels comprising 2,694 rooms currently under development, five of which (2,074 rooms) are due for completion during 2002. Four Seasons Hotel Management Group opened its first hotel in China in January 2002. Other operators said to be on the expansion trail are Six Continents Hotels & Resorts, Jin Jiang Holdings and Marriott International who are set to manage another 1,091 rooms by the end of 2002. Other major international hotel operators with a presence in China include Starwood Hotels and Resorts with 11 hotels and 4,302 rooms and Hilton International Asia Pacific with five hotels and 2,205 rooms.

CONCLUSION Given the obvious potential of the Chinese tourism and hotel markets, the motives for gaining a foothold in the market are understandable. The country is home to the largest population in the world and it currently leads the world in terms of economic growth. This economic growth looks set to continue as the benefits of the last five years� foreign investment surge and the country�s accession to the World Trade Organisation crystallise. Furthermore, the liberalisation of the economy is likely to make it become easier for foreign organisations to enter the market, while the Beijing Olympics in 2008 offer an unparalleled marketing opportunity for the city and China as an international tourism destination. �Despite the obvious attractions, the same fundamentals apply across the globe�. However, despite all of these positive factors, there are a number of key issues that somewhat temper investor enthusiasm. These include the potential for chronic room oversupply, lack of market transparency, tenure and concern over earnings repatriation. Despite the obvious attractions, the same fundamentals apply across the globe. The balance of supply and demand determines the profitability of any investment. Before investing, developing or operating in the hotel industry in China, one must always be mindful of these issues. Jones Lang LaSalle Hotels, the world�s leading hotel investment services group, provides clients with value-added investment opportunities and advice. Its recent two-year success story includes the sale of 13,994 hotel rooms to the value of US$1.4 billion in 48 cities and advisory expertise for 173,021 rooms to the value of US$32.6 billion across 343 cities. Jones Lang LaSalle Hotels� services include transactions, mergers and acquisitions, financial advice and capital raising, valuation and appraisal, asset management, strategic planning, operator assessment and selection and industry research. Jones Lang LaSalle (NYSE: JLL) is the world�s leading real estate services and investment management firm, operating across more than 100 key markets on five continents. Disclaimer Copyright - All material in this publications is the property of Jones Lang LaSalle Hotels (NSW) Pty. Ltd. (ABN 65 075 217 462). No part of this publication may be reproduced or copied without written permission. The information in this publication should be regarded solely as a general guide. While care has been taken in it�s preparation, no representation is made nor responsibility accepted for the accuracy of the whole or any part. This publication is not part of any contract and parties seeking further details should contact the author. |

###

|

Jones Lang LaSalle Hotels Fiona Cregan Associate Research and Marketing Jones Lang LaSalle Hotels Level 18, 400 George Street Sydney NSW 2000 Australia tel: +612 9220 8786 fax: +612 9220 8765 [email protected] www.joneslanglasallehotels.com |

| Also See: | Beijing Hotel Market Overview - Jones Lang Lasalle Hotels / Nov 2001 |

| Hotel Development in Southeast Asia and Indo-China / Aug 2000 |