|

advertisement |

|

|

|

advertisement |

|

|

| San Diego State University - Center for Hospitality

Research

December 2002 This forecast marks the first report issued by the new Center for Hospitality and Tourism Research (CHTR) at San Diego State University (SDSU). The report provides public and private sector travel industry decision-makers with a composite resource on data and trends in the San Diego lodging industry. The data used for the 2003 San Diego County Lodging Industry Forecast was compiled by Smith Travel Research (STR), the nationally-recognized leader in tourism industry research, and analyzed by the CHTR. Statistics also were gathered from the San Diego Convention & Visitors Bureau, CIC Research, and other credible sources. U.S. Economy

Blue Chip Consensus forecasts indicate a 3 percent growth rate for real GDP during 2003 versus 2.6% for 2002. Typically, the tourism industry recovery lags general economic growth by six months. Based on this information, revenue per available room (RevPar) growth should resume at historical levels by 2004. During the current period of economic instability, the hotel sector has performed relatively well. Much of the difference is the lack of new hotel supply; however, additional significant differences include low loan leverage, a strong banking system and much lower interest rates. The sluggish economy, the prospects of war with Iraq, and �long lasting imprints of the September 11 events on the big family vacation plans typically taking place in July and August, have prevented the market from clearly turning around,� according to Torto Wheaton Research. The U.S. economy appears likely to sputter throughout the first half of 2003, with more layoffs and fewer new jobs in store, according to The Anderson Forecast released December 5, 2002, by the University of California Los Angeles. The forecast predicts the national economy will experience sluggishness and a disappointing labor market until mid-2003, when business spending will finally begin to pick up. U.S. Lodging Market

Nationally, the occupancy for 2002 should finish the year at just under 60 percent at an average room rate of $83. The occupancy is down two percent from 2001 while the rate is down three percent from last year. Through the first 10 months of the year, only New York, Oahu and San Diego are over 70 percent occupancy. New York lost nine percent in average rate while Oahu lost six percent. San Diego is down less than one percent in average rate this year. UBS Warburg expects total U.S. lodging room revenues (the change in demand and room rates) to increase 2.0 percent in 2003. Subtracting their U.S. room supply growth estimate of 1.2 percent from this estimate, results in a 2003 U.S. RevPAR growth forecast of just under one percent. To add some international perspective, the highest major city occupancy through October of this year is Tokyo at 79.5 percent while the lowest is Jerusalem at 32.4 percent, according to the HotelBenchmark Survey by Deloitte & Touche. Generally, Asia and Europe are strong while Latin America is weak. According to the Travel Industry Association of America (TIA), �international travel, business travel and air travel will continue to be down during the holiday season and into early �03; Internet bookings, leisure travel, auto travel, RV and cruise travel will be up. Travel closer to home as well as last minute bookings will be up.� The Internet will be the primary growth market representing a jump from $24 billion in 2001 to $64 billion in �07 according to Jupiter Media Matrix. The growth will not come from new Internet users, rather more �bookers� than lookers. Prices are now transparent to all travelers, reducing growth in average rates until room demand rebounds more fully. Holiday season travel will be up this winter due to pent up demand for close to home, family travel. Some financial trends have emerged in our industry. Mezzanine finance, particularly with lenders asking for as much as 50 percent equity, has become commonplace. Firms to ensure that management is optimized are also utilizing asset management. Lodging stocks will likely be flat in the short-term but are positioned for growth in the near future. A good trend is the reduction in new supply; however, lenders are beginning to consider opening the spigot for selected hotel development projects. Regional Economy

San Diego Lodging Forecast 2002

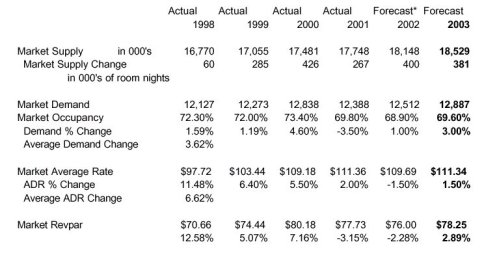

When compared to the leading cities in the United States, San Diego is one of the strongest in both hotel industry performance and desirable destinations. The region is capable of absorbing several thousand new rooms over the next three years, most of which should be targeted for the convention center expansion. Specific markets where new hotel supply is capable of being absorbed include the downtown market area and coastal strip areas of La Jolla and Del Mar. These markets have a strong mix of corporate and leisure demand, both of which should begin to pick up in 2003. San Diego benefits by having a �drive-to� market with travel market segments that do not require the return of the business traveler. These include convention, government and leisure travel. Based on that, the forecast is for occupancy levels to improve to 70 percent in 2003 with average rates up to $111. Provided at the end of this forecast is a graphic depiction of supply, demand, occupancy, and rates based on a 10-year history in San Diego County. New development of hotel properties is limited in the immediate future.

This is based in part on the difficult financing market today. San Diego�s

lodging market should look forward to tremendous success in the future.

On the attached graphic, it is easy to see what has occurred in San Diego�s

lodging market over the past 10 years. When demand increases, occupancy

levels move up, particularly when new supply is limited. In the early �90s,

demand could not keep pace with supply. When it did catch up, rates firmed

up and grew beyond the consumer price index. Today, with less than three

percent per year supply growth, occupancy levels will begin to increase

above 70 percent. That appears to be the magic number that drives average

rate increases. There are always caveats to a forecast of economic

activity. These include but are not limited to further budget and trade

deficits, changes in Fed policy on interest rates, corporate earnings,

holiday spending, retail sales, continued terrorist attacks, war and general

traveler sentiment. In addition, housing prices have in many ways held

consumer spending up. Without this buoyancy, we would be struggling in

a deep recession.

* - includes actual data through October, 2002

Commercial Traveler Demand

As an example, according to Marcus & Millichap, San Diego�s biotech demand has kept the office market alive as technology companies cut back spending, employment and office absorption. These same companies will fuel some job growth as well as extended-stay and corporate lodging demand. Group Meeting Attendee Demand

Meetings at individual properties represent as much as 50 percent of room revenue at certain San Diego resorts and hotels. While this segment will not grow markedly in 2003, it should resume strong, steady growth in 2004. Thanks to the addition of the Lodge at Torrey Pines, renovation of La Costa Resort, addition of the Del Mar Marriott and W Hotel as well as the addition of several great golf courses, San Diego is now perceived as a more comprehensive resort destination. Leisure Traveler Demand

|

Contact:

###

|

Robert A. Rauch, CHA Director, Center for Hospitality and Tourism Research San Diego State University San Diego Tel: 858.792.3530 [email protected] http://www.sdsu.edu/ |