| The Global

Hospitality Advisor

-

|

|

|

|

| The Global

Hospitality Advisor

-

|

|

|

December 2002

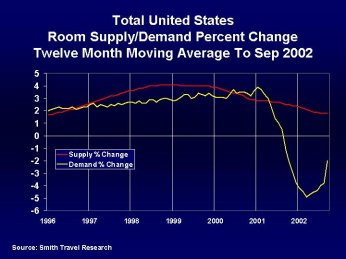

Jim Butler: By year-end 2002, the hospitality industry had suffered through two consecutive years of declining RevPAR with approximately a 10% drop from 2000 through 2002, and the outlook for 2003 is relatively flat. How and when do you see the industry recovering . . . or do you? Steve Rushmore: As 2003 begins, it now appears that the impact of the terrorist attacks on travel and the U.S. lodging industry was relatively mild and short-lived. What did have a profound effect on U.S. hotels was the downturn in the economy and the related cutback on business travel. Throughout the U.S., hotel occupancies declined somewhat and room rates were generally lower. Jack Westergom: Yes, Steve, and

the hospitality industry�s performance closely follows the general economy

and corporate earnings. By definition, the corporate travel market is dependent

on corporate travel, capital expenditures, new product launches and the

training that accompanies it. As long as the economy is sputtering and

corporate earnings are poor with companies slashing expenses, the hotel

industry will suffer. We do not foresee major improvements in the economy

or corporate earnings for at least another 12-18 months and it could be

longer if we have a war with Iraq.

Butler: When will transaction volume increase and who will be the buyers? Alan Reay: 2002 will be recorded as one of the slowest years for hotel transactions in a decade. The slowdown in sales that had begun in the second half of 2001 was further exacerbated by the terrible events of 9/11. The spread between buyer and seller price expectations really widened in 2002, and transactions, especially in the higher end, were almost non-existent. In just the last 30 days, we have seen an important shift in the marketplace by sellers. Some have likened this to the sellers �blinking first.� In any event, sellers have become somewhat more realistic in pricing their hotels for sale. We think that sellers initially believed that the downturn was going to be a short-term phenomenon. They now understand that they cannot sell based on year 2000 numbers. Buyers and their lenders are looking at trailing twelve-month numbers and applying a realistic cap rate ranging between 10%-12%. We expect a tremendous increase in sales activity in 2003. The number of properties that have just come onto the market in the last thirty days alone, with many sellers demanding a fast close, will no doubt set some new, albeit lower, sales values. This in turn will motivate other sellers with their hotels on the market to lower their price expectation. Our own activity is up over 35% at this time verses last year and we are doing more proposals for lenders. Hanson: There are approximately 140 equity funds and major buyers waiting for the spread between bid and asked to narrow. So when sellers realize the �recovery� does not justify 1999 or 2000 values for most assets, and the buyers continue to moderate their expectations given the low returns in public equities and fixed income investments, I believe the equity funds will be the first to execute transactions. The public companies will need to wait until the public equity markets become friendly, and that is likely to be well into 2004 or even 2005. Rushmore: We think today represents

one of the best hotel buying opportunities in the past 10 years. Don�t

expect any great deals on pricing, but you can feel comfortable in the

fact that the risk of new supply entering the market has been virtually

eliminated. And this produces a very favorable hotel buying and ownership

picture. I recommend buying any good quality hotel that is being marketed

at 1999 values�wherever it is located. However, use caution in the tech

areas around Boston and San Francisco, which may show significant pricing

discounts. I also recommend looking at secondary markets that are overlooked

by the large number of opportunity funds.

Butler: How will hotels be valued and priced, and where are values headed? Rushmore: Hotel values in most markets have held up quite well. While they are generally not up to the record 2000 levels, most hotels have been selling for their 1998 to 1999 values. The exceptions are the tech centers in the Boston and San Francisco Bay areas and those gateway cities that depend on overseas travel to the U.S. Values in these cities are down significantly. Although hotel values are down in most markets, there are very few bargains for buyers. Sellers simply do not have to nor want to sell at depressed values so they are holding on until the price is right, which will probably be around 1999 to 2000 value levels. As a result, sales activity was very slow during the first half of 2002 and is now picking up. Reay: There are fewer buyers and lenders for luxury and higher-end, full-service hotels, especially at the current asking prices. In certain locations, we are seeing properties now going for prices as much as 40% below what they went for just four years ago. On the other hand, we see the limited service sector holding up quite well, and in some of the secondary and tertiary locations, we expect to see prices still increasing. In the disproportionately affected markets Steve has mentioned, virtually all product types have been hurt. Butler: New hotel development is off dramatically. What is the outlook for new development? Westergom: Hotel development is dependent on two dynamics: (1) the ability to raise capital for acquisition and construction, and (2) cash flow from property operations. Currently, cash flow performance is on a downward trend and lenders

look unfavorably upon hotel assets as investment opportunities. Until cash

flows improve, asset acquisition prices drop and the economy turns around,

we believe that current conditions will remain static. If lender foreclosures

increase next year, flooding the market with inexpensive product, then

the market may turn around and vulture funds similar to Patriot American

in the 1990s may take over hotel acquisitions. Upscale hotels have the

greatest potential in the next year as lower-end supply outpaces demand.

Lomanno: Hotel development has indeed slowed, and will grow at about 1.7% in 2002 and 1.5% in 2003. This still results in about 70,000 new rooms opened this year. While significantly below 1990s levels, this still represents a lot of rooms being added. In the next two or three years, markets most affected by new supply growth will be San Diego, Orlando, Houston and Miami, each of which will experience supply growth in excess of 5%. When development does return, it is most likely to be in the midscale without F&B category. Hanson: In 2002, there will be approximately 59,600 room starts compared with almost 160,000 in 1998 and the 25 year average of 96,000. PwC forecasts this to remain flat in 2003 with 63,000 starts and begin to increase in 2004 with 93,200 room starts. There has never been a cycle before during which demand and supply have slowed with such similar timing and velocities. Importantly, every period of especially slow levels of construction has been followed by a period of robust RevPAR growth�this portends well for 2004 and 2005. Reay: I can tell you that the surge

of luxury properties that were built in the last three years is not going

to continue, as this segment has suffered the most from the downturn. Lenders

are even more cautious on new hotel development and require developers

to have more equity in the deal. Loans to values are in the 50-60% range,

which will mean that a lot of projects simply will not get built. What

does seem to be getting out of the ground is the higher end, limited service

product, including Marriott�s Residence Inn and Courtyard brands as well

as Hilton�s Garden Inns and Hampton Inn & Suites.

Butler: And how about the outlook for boutique hotels? Whelan: The label �boutique� has been too broadly applied. At the Kimpton Group, a �boutique hotel� is a service orientation more than a building type. Boutique embodies providing the guest with highly personal service and value and allowing the guest to have a choice when selecting their environment, the service they want, and the personal attention that will enrich their experience. Boutique is creative�not rigid. For us, a boutique hotel is a design oriented, architecturally unique, stylish, intimate, full service hotel equipped with the full range of IT features and services our guests demand. The future for boutique hotels in our category is bright. The recovery of the boutique niche, like the industry in general, will rely on the national economic recovery. When that occurs, selective markets will open up. It is a small niche with ample room to grow. The boutique product will be increasingly sought after by guests seeking a better lodging experience. Our boutique hotel creations are guest-driven. The key issue for each individual boutique opportunity is to derive the appropriate combination of product type, design, and service orientation and then deliver on that to perfection. Successful boutique hotel development and operation is very hands-on, and management intensive, not mass-produced. We operate many hotels for unrelated third-party owner/developers who have retained us to help them derive the right product focus and orientation, to provide the right physical plant to support the services and the service level best suited to maximizing the owner�s return and the guest's experience. Once we get beyond this current economic downturn, the underlying fundamentals of demographic growth and shifting demand patterns all support an increased demand for the more legitimate boutique hotels. A successful boutique hotel/restaurant combination will reinforce the emotional contact it has with its guests to create a high degree of guest loyalty. Lomanno: Well Jim, for our analysis, we probably use a broader definition of boutique than Kimpton. And on that broader category, we find that boutiques, a very popular segment until the current downturn, have been very badly affected by the lodging downturn. However, since most of these types of properties are in the 15 markets most affected by the downturn, it is hard to determine how much weight to place on location as opposed to customer preference. It seems like they should rebound when those markets do, but time will tell. Hanson: We too view the boutique segment differently. We view boutiques as consisting of independent properties with ADRs above the upper upscale segment ADR. This segment has experienced the worst decline in lodging demand (-9.0%) among all segments in 2001. Compared to the luxury and upper upscale segments, however, the boutique segment experienced more moderate ADR declines (-2.2%). The trend continued through the first eight months of 2002, with the boutique segment experiencing the worst demand declines (along with the midscale with F&B segment). In 2003, the boutique segment will begin to benefit from the recovery in business travel and experience a 4.4% increase in demand. PwC�s occupancy forecast is for an increase of 1.1 occupancy points to 64.3% while ADR will increase by only 0.8%. The boutique segment nominal RevPAR will be 14.6% below 2000 levels. Westergom: Boutique hotels will always be in demand, but have great difficulty in surviving during slow economic times due to lack of marketing dollars and marketing clout. Some boutique companies like Kimpton and W have brand recognition, and they have a more favorable outlook because of their brand power in driving occupancy, economies of scale, and ability to consolidate marketing dollars. Well-established individual boutique hotels will continue to flourish because of customer loyalty. Butler: Workouts, bankruptcies and receiverships were widely anticipated in early 2002, but largely failed to materialize. Is the threat gone or getting ready to surge? Earnest: Hotel loan delinquencies began to increase with the economic downturn in the first quarter of 2001. However, after September 11th, the hotel industry experienced a significant increase in hotel loan delinquencies. This first phase of the industry downturn over the past 15 to 18 months has consisted of growing defaults in securitized (mainly conduit) hotel loans and a moderate number of restructured hotel loans by many portfolio lenders. Actual defaults and major enforcement actions by lenders have primarily been confined mostly to the CMBS world. As downward pressure has continued on the hotel industry, particularly during the second half of 2002, we believe a second phase of hotel loan defaults and re-structure is just beginning. CMBS hotel loan defaults show no sign of abating. Many more hotel loans are requiring restructure to prevent a new default situation from occurring. Numerous hotel loans that were restructured over the past year are being restructured again in more meaningful and substantial ways. With the projected recovery of the industry off in the distant future, many hotel owners are tiring of feeding properties to protect equity that may not be recoverable after all. Overall, this second phase of hotel loan defaults and restructurings will bring a material, although not alarming, increase in hotel loan problems. Hanson: The �surge� is past. Delinquencies peaked in the late second and early third quarters at only 5.5% compared with 16% in 1990. The industry entered this cycle with a record 3.4 x debt service coverage, the lowest breakeven occupancy ever (only 53%), and record profit levels, so the industry has been structurally able to perform even in the worst conditions in 70 years. Lomanno: Prior to the current downturn, for the most part, the hotel industry was very profitable. Despite the current problems, basic profitability has not changed, nor is it likely to in the immediate future. Debt is at historically low levels, and operations are generally much more efficient. This has enabled most hotels to maintain profitability, despite a reduction in total revenue. Westergom: If the economy remains stagnant, the pace of foreclosures will pick up significantly. Lenders cannot afford to keep non-performing loans on the books for too long, regardless of their financial creativity and their attempts to prolong the inevitable. Many CMBS properties have large bullet loans that will be due within the next 12 months and have no way of paying even if the economy improves significantly. We will not see a repeat of the late 1980s, but we may see a more aggressive stance by lenders on delinquent borrowers. Reay: We see an increase in foreclosures in 2003, especially in the San Francisco and San Jose areas. Properties that are high risk are those hotels that were developed in the last 24 months as well as hotels that were purchased during the same time frame. Many properties are falling behind in either their replacement reserve accounts and/or on property taxes. We are seeing a marked increase in partner litigation, usually a sign of deteriorating conditions. A number of properties are failing on their Quality Inspections, due to the fact that owners are struggling to pay their lenders and have very little margin to fund needed improvements or repairs. Butler: What other trends, problems, opportunities or developments do you see in 2003 and beyond? Westergom: I am biased. My firm specializes in helping owners maximize their profits and protect asset value. We have not seen owners� profits under such pressure for a decade, or at least since the last real estate downturn. There are too many management company executives today who do not think like owners. The easy 1990s bred a whole generation of order takers, instead of order makers. These executives do not know how to compete for business because they never had to do so before. Let me give you an example. We asset manage a midsize upscale asset that lost over a million dollars of NOI last year. That property will make almost $1.25 million in NOI this year or a $2.25 million turnaround. Management would have claimed more in fee income (approximately $1,500,000) than the property generated in NOI. Obviously, management is not sharing the economic hardship with ownership. Very little of this turnaround would have happened, however, if we had not �managed the management company� and required them to redeploy and re-staff their sales team, adjust their marketing focus, aggressively pursue higher rated room rates and re-price our spa, food and beverage offerings throughout the property. We made sure that owner�s and management�s interests were in alignment. The need to aggressively asset manage hotels is greater today than ever before. Lomanno: The major challenges are pricing, pricing and pricing!!! Outside of the threat of war, we see the threat of a deflationary economy as having major repercussions. One only has to look at the complete meltdown in the airline industry to see the effects of an economy in which an industry is hampered by very high fixed costs and unable to raise the price it charges for its service. There are many similarities in the hotel industry�spiraling utility costs, increased wages and benefits as well as astronomical increases in insurance, including liability and workers� compensation. A prolonged deflationary economy could be catastrophic. Hanson: As Jim Butler knows with his experience in management contract negotiations, litigations and arbitrations, management agreements and management relationships are going through more changes than they have since their inception�a response to the agency and fiduciary duty issues, and the additional stress on owner-operator relationships because of the two-year 9.3% industry decline in RevPAR. I doubt any company�s survival will be seriously threatened, mostly because the management companies are too important to the owners. But management agreement litigation and arbitration are likely to accelerate as owners learn about some of the most egregious activities and the very strict principles of agency. The implications of an agency relationship are understood by very few owners. Butler: What are the major changes in debt and equity financing for hotels? Who are the players, what are the terms and what is getting financed? Earnest: The market for hotel loans has become increasingly tiered as to credit quality. Financially strong owners possessing quality hotel properties with in-place cash flow in solid markets have more lending options available than at any time during the past 2 to 3 years. In many situations, we are one of 15 or 20 lenders quoting these top tier transactions. Top tier owners and properties are enjoying hotel loans with full proceeds, competitive spreads and attractive overall terms. However, beyond these top tier situations, capital availability is much more limited and less flexible. Non-stabilized properties or development opportunities are very difficult for all but the strongest developers. Less than premium brands and secondary/tertiary markets also present unusual financing challenges. Flaig: The usual suspects continue to lend on hotels. The few banks with expert teams are likely to remain active now and in the future. Aareal Bank continues to be very active in hotel financing. We typically do not provide construction financing because we focus much of our underwriting on the existing net income of the property. But we are looking for good hotel lending opportunities. For us, that means that the hotel should be well located with high barriers of entry. Solid hotel operations expertise, and a powerful brand name with a global reservation system, are also essential. At present, we see a trend towards floating US LIBOR loans with a 5-year term. Mezz financing is omnipresent but only above 70% LTV. The trend for loan rates is upward. Butler: Have lenders changed underwriting criteria materially since September 11th? Whelan: Lenders are more scarce. Loan underwriting tightened before 9/11. Equity investment requirements are higher. And along the lines that Andreas mentioned, we are seeing lenders requiring independent hotel owners/developers to pair up with legitimate national operators. In fact, several opportunities have come our way for third-party management as a result of the lenders' requests for a national operator to manage the property on completion of development. Lenders seek an operator with a strong regional and national guest base coupled with a sophisticated national sales and distribution system. Our approach with all our boutique hotels is to use our national system to sell the right product to the right customer at the right time for the right price to maximize revenue and profit. It has taken years to develop our system; lenders and investors place high value on that. Hanson: I think Jerry Earnest said it well earlier. There is more talk about changes in underwriting than there are changes. Based on PwC research, there has been less than a five percent change in loan-to-value ratios and no change in debt service coverage ratios, although it is important to note the standards are being applied to current occupancies and rates. That is the real change! Flaig: The underwriting criteria have not materially changed since 9-11. Lower EBITA numbers in most markets directly affect the loan that can be justified by current cash flows. Furthermore, we have seen net income drop more than values. The loan-to-value ratios as such have remained unchanged in my view; however, the denominator (value) has decreased noticeably. The debt coverage ratios for senior debt have increased to about 1.5 on the basis of a 6-7% interest floor. We have seen no changes in value appraisals. Butler: During the past year, mezzanine loans have played an important part in maintaining reasonable leverage levels on a wide range of hotel assets. Do you continue to see a major role for mezzanine lenders in the hotel industry? Earnest: Mezzanine loans have played a major role in sustaining liquidity for hotel financing over the past year. The number of hotel mezzanine lenders and the amount of capital allocated to hotel investments is unprecedented. Over the past year, the lending market has become much more efficient in matching up senior and mezzanine lenders. Increasingly, hotel lenders, including GMAC Commercial Mortgage, are delivering a seamless senior/mezzanine loan product to hotel owners. Previously, hotel owners had to find and match up separate lenders to create this senior/mezzanine loan product. The ready availability of mezzanine capital for hotel loans has shifted the debate more towards pricing and flexibility, and away from loan proceeds. We expect mezzanine capital to play an increasing role in hotel finance in the years ahead. Flaig: I see a very important and continued role for mezzanine lenders in the hotel industry. Even in a low interest environment like today, hotel assets that are coming up for refinancing are more likely than not relying on mezz debt to cover the shortfall in values. With values having fallen more than the amortized loan amount, LTVs being the same, more equity or mezz debt is required to move forward. With interest levels where they are now and likely to be in 2003, we see a continued activity in refinancing hotel assets with a mezz component. Westergom: Mezzanine loans have become more important than ever, as lender requirements have created a large gap between debt and equity capabilities. Mezzanine loans have been a common aspect of new hotel development for most brands, but that has changed, as many brands are no longer in the lending business. Mezzanine loan rates have increased from the 12-20% range to the 18-26% range. With equity availability declining, mezzanine financing is now the only way to get a deal done. The pool of mezzanine players is smaller today than at anytime in the past six years. The Global Hospitality Group® is a registered trademark of Jeffer, Mangels, Butler & Marmaro LLP ©2002 Jeffer, Mangels, Butler & Marmaro LLP |

|

Jeffer, Mangels, Butler & Marmaro LLP web site: http://www.jmbm.com Email Jim Butler at [email protected] Or contact Jim Butler at the Firm Jeffer, Mangels, Butler & Marmaro LLP 1900 Avenue of the Stars Los Angeles, CA 90067 Phone: 310-201-3526 The premier hospitality practice in a full-service law firm |