|

|

|

|

|

|

|

,

|

|

|

| 16 December 2002 - Our research examines

the relative performance of the European hotel sector over the last 12

months and highlights strategies that have been adopted to cope with 9/11

and the deteriorating economic conditions. To mitigate the impact

of seasonality we have tracked the performance of a consistent sample of

hotels between January 1999 and September 2002 and analysed the data on

a rolling 12-month basis.

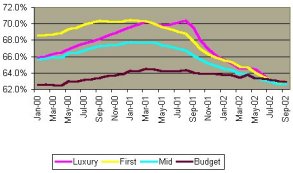

Our analysis looks at hotel performance data for both the UK and continental Europe by segmenting the hotels that contribute to our survey into four different categories � namely luxury, first-class, mid-market and economy/budget. Since there is no official grading system across Europe, Deloitte & Touche have applied a classification to each brand in the survey, which broadly recognizes the positioning of each of the brands. Our research reveals, as illustrated in Chart A, that on a rolling 12-basis the luxury, first-class and mid-market sectors have all experienced significant occupancy declines post 9/11 across continental Europe. In the case of first-class and mid-market hotels this decline actually started at the beginning of 2001, in the main caused by a slowdown in the world economy, which lead to curtailing of travel budgets, although the events of 9/11 exacerbated the decline. Prior to 9/11 luxury hotels managed to maintain occupancy levels but in the wake of changing travel patterns post 9/11, as non-essential travel plans were scaled back, this sector came under the most pressure with occupancy levels falling rapidly from 70 percent to 62 percent. By contrast, the budget sector has proved very resilient with occupancy levels actually increasing, albeit marginally (up one percent) to 63 percent. One reason for this is that budget hotels are generally located in either suburban areas or on motorways, and as consumers have preferred to stay closer to home and travel by car or rail, these properties have been well located to attract this extra demand. Chart A � Continental Europe rolling-12 occupancy

analysis by grade of hotel

Despite this fall in demand, all sectors in continental Europe have managed to improve average room rate when measured in euros between January 2000 and September 2002. First-class, mid-market and budget hotels have all witnessed rate growth of circa 12 percent, whilst the luxury sector, which trades at a 100 percent premium to the market average has experienced a 31 percent increase in average room rates as demonstrated in Table 1. Table 1 - % change in KPI�s between January

2000 and

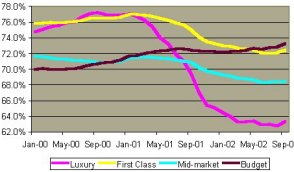

Source: HotelBenchmark Survey by Deloitte & Touche The resilience of the budget sector is further demonstrated by the performance of the UK hotel market where occupancy has moved ahead five percent between January 2000 and September 2002. This sector is the only market sector in the UK to have exhibited an occupancy increase, and its performance contrasts particularly with the luxury sector which has seen occupancy levels plummet 15 percent from 77 percent to 63 percent (see Chart B). Despite an overall fall in UK average room rates of 1.3 percent, the budget sector rates have held up well with room rates improving by 2.5 percent over the same period. Chart B � UK rolling 12 occupancy analysis

by grade of hotel

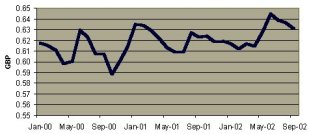

One of the reasons that UK hotels have experienced average room rate declines whilst their continental neighbours have reported significant real average rate growth has been due to the relative strength of the UK pound against the euro. Chart C � GBP-EUR Exchange rate

As a result, the UK has become comparatively more expensive relative to other European destinations. In addition, with the introduction of the euro in January 2002 this has created further transparency in the marketplace, allowing consumers to more readily identify the relative cost of a room in each country. However, despite the falls in occupancy, UK hoteliers have remained relatively robust in keeping price discounting to a minimum, especially in the luxury sector where average room rates are just 0.1 percent below their January 2000 levels, despite the 15 percent fall in occupancy. Commenting on the findings, Julia Felton, director travel, tourism and leisure at Deloitte & Touche says: �The budget sector has proved the most resilient across Europe during the recent tough trading conditions. These properties have been well located to benefit from increased travel by road and rail, as consumers have opted to engage in intra-regional travel rather than fly to destinations further afield. Depressed economic conditions have also encouraged business travellers to seek more reasonably priced accommodation, and so we have witnessed a trading down effect occurring across the spectrum of hotel types. What will be interesting to observe is what proportion of these travellers trade up once economic conditions improve in the future.� The HotelBenchmark Survey contains the largest independent source of hotel performance data outside of North America and tracks the performance of over 6,000 hotels every month. To complete this analysis data for a consistent sample of hotels across Europe was collated between January 1999 and September 2002. To mitigate the impact of 9/11 data was computed on a moving 12 basis so that the real underlying trend in performance could be analysed. Deloitte & Touche is the UK practice of Deloitte Touche Tohmatsu, a global leader in professional services with over 98,000 people in 140 countries. The dedicated Travel, Tourism, and Leisure practice serves owners, investors, operators and developers throughout Europe, the Middle East, India and Africa. Authorised by the Financial Services Authority in respect of regulated activities. The information contained in this article is correct at the time of going to press. |

| Contact:

Laetitia Mowat Media & Public Relations, Deloitte & Touche on +44 (0) 20 7303 4820 www.deloitte.co.uk Lorna Clarke HotelBenchmark Survey Deloitte & Touche 180 Strand, London WC2R 1BL United Kingdom Tel: 44 20 7438 2870, Fax: 44 20 7304 1391 E-mail: [email protected] www.HotelBenchmark.com |

| Also See: | International Occupancy and Rate Report / October 2002 / Deloitte & Touche / Dec 2002 |

| Cardiff's Hotel Industry More Robust than Any Other UK City; London Fared the Worst, with Profits Declining 15 percent / Deloitte & Touche / Nov 2002 | |

| London Hotel Market RevPAR Declines 16 percent in March 2002 / Andersen / April 2002 |