|

|

|

|

|

|

.

|

and Average Rates Through the First Half of 2002 |

| by Rod Clough

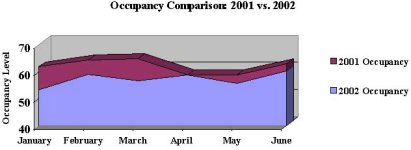

September 6, 2002 Dallas has been the site of declining hotel occupancy and average rate levels through the first half of 2002, influenced primarily by the downturn in the tech and telecommunications sectors as well as other secondary factors. According to Smith Travel Research, occupancy for the six months ending June 2002 dropped to 57.0% for the MSA, off from almost 62.0% a year earlier. After virtually closing the occupancy gap in April, May and June occupancy declines have been modestly lower than declines experienced in the first quarter.

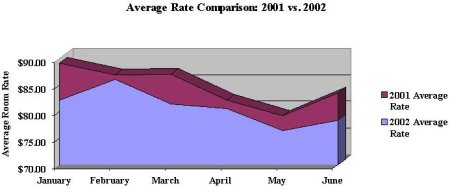

Also according to Smith Travel Research, average rate has dropped by 4.0% thus far in 2002, to just over $80.00 from $83.75 in 2001. Declines in rate were less significant in February and April, while the greatest declines have been experienced in January, March, and June.

Various Dallas sub-markets became over-heated during the tech boom of the late 1990s and into 2000, as unprecedented business levels were seen at major telecom and tech powerhouses throughout the city. Dallas MSA unemployment hit its low in December of 2000 at 2.6%. Key players, such as Texas Instruments, Nokia, Nortel, and Alcatel, to name a few, drove hotel demand to never before seen levels. Following the tech bubble burst, demand from these sources declined during the last three quarters of 2001 and has remained at standstill levels for much of 2002. By June 2002, unemployment reached its highest level for the year, at 7.5% (unemployment last topped 7.5% in June of 1992). While many of these companies are now touting leaner, meaner operations and business models that are poised for recovery over the next three to five years, others are still retooling and reorganizing, announcing occasional layoffs and reorganizations. Hotels able to draw from a diversified base of demand have fared better, but, few hotels have been completely spared from the city�s business slow down. Downtown hotels are looking forward to the unveiling of the expanded and renovated convention center, which should help support a recovery in the coming years. The city is touting the new 203,000-square-foot hall as the world�s largest column-free exhibit space, and altogether the center will offer over 900,000 square feet of exhibit space - the most in the state. The project is scheduled for completion in September, and a grand opening celebration is planned for December. The city�s normally bustling Dallas Market Center (DMC) experienced a downturn in hotel room night generation during the first half of 2002, continuing its slide from the peaks experienced in January and October of 2000. The first quarter and the fall months of September and October are normally the brightest spots for this sub-market, providing demand which overflows into the Brookhollow and CBD sub-markets. Market Center hotels typically see occupancy levels above the 70-percent mark, and rates at or above $100 overall; January and October are particularly strong, normally spiking the market average rates over $120. On the heels of an expected brighter September and October ahead, we expect some strengthening in this sub-market during the first quarter of 2003. January 2003, in particular, is poised to be a strong month for the Markets, with roughly 10 events scheduled, including the highly attended gift, apparel, and furniture markets. Hotel demand associated with DFW International Airport has declined concurrent with its lower activity levels. For the first half of the year, passenger activity at D/FW International was off just under 11.0%, mirroring the decline in American Airlines traffic, which represents roughly 70% of the airport�s activity. American Airlines is working hard to streamline its operations in order to remain in business. On August 22, the company, which is headquartered at the airport, announced plans to consolidate its operations into two buildings from its current 11-building campus. Delta, which represents the next greatest share at roughly 17%, was down a lesser roundly 5.0% in activity for the first half of the year. Fortunately, the passenger gaps are shortening somewhat, with declines in May and June less significant than declines in earlier months. Construction on the airport�s new international concourse is also continuing and is on schedule. Despite the recent declines in activity, D/FW remains a leader in nationwide airport operations, with almost 26 million total passengers passing through the facility during the first half of 2002. Growth continues to push northward, with Grapevine, Frisco, Southlake, and Flower Mound, among other outlying communities, seeing expansion. Relocations are also occurring within the Dallas area, as some companies move northward to newer office spaces (now available at attractive prices) or otherwise consolidate operations in order to cut costs. The next five months should continue to show stabilizing trends, as the convention center comes on-line, companies continue to streamline and re-organize operations, passenger activity at the area airports stabilize, and activity at other market drivers, such as the Dallas Market Center, improve from fall 2001 levels. A positive turn towards recovery is expected for 2003. |

Contact:

| Rod Clough

Managing Director HVS International Suite 101 2601 Sagebrush Drive Flower Mound, TX 75028 972-410-2002 [email protected] |

| Also See | Hotel Business in Dallas Area Looks `Mediocre' for Fall / September 2002 |

| Hotel Occupancy Rates, Revenues in Fort Worth and Arlington, Texas, Area Continue to Slide / May 2002 | |

| Dallas Report / 2002 National Lodging Forecast / Ernst & Young LLP / Feb 2002 |