By Cristiano Vasques , Pedro Cypriano , Fernanda L'Hopital

Introduction

It is our great pleasure to present the third edition of the Trends and Opportunities South America, an annual publication by HVS/Hotel Invest (in partnership with STR) that illustrates and analyzes the sector’s performance in some of the major markets in the region.

Every year we provide recent and reliable information in addition to telling you about the challenges and opportunities in South America’s main hotel markets. We are convinced that an informed and transparent market is more solid and professional. Having said this, we believe that this publication will increasingly become a key tool for hoteliers, developers, and investors by supporting them to properly formulate their business and investment strategies.

If you wish to receive this publication and other news from HVS/Hotel Invest, please visit our websites (www.hvs.com and www.hotelinvest.com.br) and follow us on LinkedIn (HVS| HotelInvest). For further information, questions, comments or suggestions, please contact Cristiano Vasques – São Paulo, (55 11) 3093-2743, [email protected] – or Fernanda L’Hopital – Buenos Aires, (54 11) 5263-0402, [email protected].

Our Sample

The Report’s broad database mostly comprises data from STR, supplemented by HVS/HotelInvest own records and data provided by third parties. We thank all those who have contributed to this publication and we invite new hotels, operators, and associations to share their data through STR for future editions, contacting Patricia Zulato: (55 47) 99201-7002, [email protected].

The information contained herein is based on the performance of 80,665 rooms using data on average daily rates in nominal value and national currencies, and includes the main hotels in each segment of each city. We are therefore certain that the trend indicators truly reflect what is happening in each market universe.

Our annual comparisons use the same sample base throughout the historical series, except when there are openings or significant segmentation changes. Our wide sample plane is statistically significant and is shortlisted below:

- Buenos Aires: 7,828 rooms (38% of the analyzed universe);

- Santiago: 8,186 rooms (57% of the analyzed universe);

- Bogota: 7,525 rooms (65% of the analyzed universe);

- Lima: 4,267 rooms (48% of the analyzed universe);

- Rio de Janeiro: 18,794 rooms (62% of the analyzed universe);

- São Paulo: 21,822 rooms (59% of the analyzed universe);

- Salvador: 2,434 rooms (27% of the analyzed universe);

- Curitiba: 3,088 rooms (32% of the analyzed universe);

- Porto Alegre: 2,234 rooms (32% of the analyzed universe);

- Belo Horizonte: 4,487 rooms (39% of the analyzed universe).

2016 Retrospective and 2017 Outlook

Change of tack, good prospects for South America

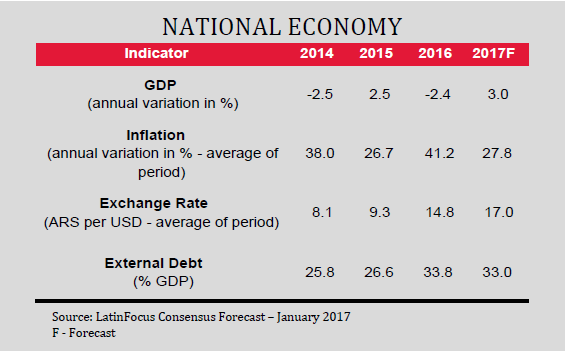

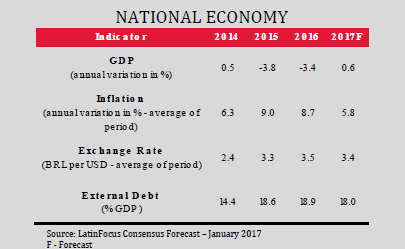

2015 and 2016 were marked by low economic growth in South America. The international backdrop for this poor regional performance included the global economic slowdown and the drop in the price of commodities, which affected the raw-material exporting countries. In addition to these external events, there were some regional factors such as new presidents taking office, plus bad administrations, in some cases, and the inability to strengthen the institutional framework and fight against corruption. Although all the countries in the region, except for Peru and Paraguay, evidenced a slowdown, the regional recession is accounted for by the internal crises of Argentina, Brazil, and Venezuela. The good news is that a change of trend is expected in 2017. On the one hand, most of South American governments are shifting from the left to the right, with the implementation of reforms aimed at balancing the economy and improving the business climate, which should lead to greater economic growth. On the other hand, brighter prospects for the regional and global scenarios, higher raw material prices, and government investment plans should favor the South American economies. The United States withdrawing from the Pacific Alliance might encourage the creation and strengthening of regional blocs, with a positive impact on its members.

In Argentina, the first year of Macri’s administration set a change in the country’s economic direction. In 2016, despite the drop in GDP, major economic adjustments were implemented to start balancing the economy. Although there are pending reforms and challenges to be solved, positive signs have already appeared as well as an improvement in confidence levels and in the institutional and business climate. This together with a more favorable global and regional scenario will reset the country on the growth path in 2017.

In Chile, despite the drop in copper prices, Brazil’s recession (a major business partner), and business discontent due to government reforms, the GDP went up by 1.7% in 2016, which shows the country’s economic soundness. Economic activity is forecast to accelerate in 2017, encouraged by higher copper prices and more favorable prospects for China, the United States, and Brazil.

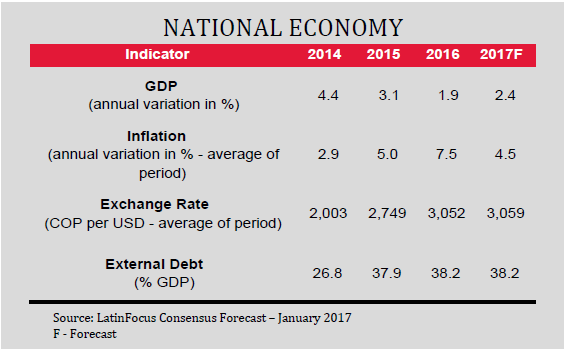

Colombia suffered from increased economic slowdown in 2016, mostly as a result of lower crude oil prices, accompanied by concerns about the country’s fiscal deficit and a rise in inflation. However, toward the end of the year, Congress passed a tax reform bill aimed at increasing tax revenue and helping the country keep its credit rating amid a slump in oil revenue. This, in addition to progress over the peace agreement with FARC, prospects of crude oil and farm product exports picking up, an increase in industrial production, plus more investments in infrastructure, account for greater growth projections in 2017.

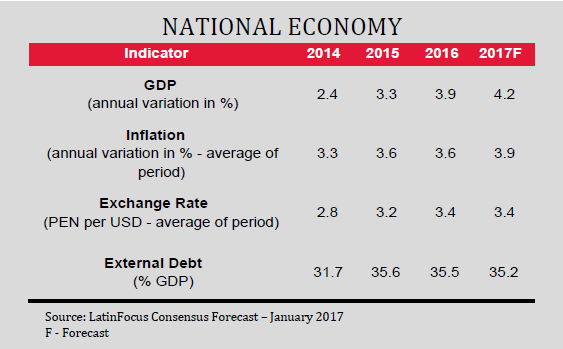

Peru was the star of the region. Although the country’s presidential elections, whose winner was the pro-market candidate Pedro Pablo Kuczynski, prevented greater growth, Peru’s economy showed an attractive 3.9% expansion in 2016. This was possible thanks to an increment in traditional exports and to the recovery of the manufacturing sector. The local economy is expected to expand even more in 2017.

In Brazil, high unemployment, credit restrictions, political unrest, and weak external demand caused the economy to drop again in 2016. The new government has implemented a series of reforms that are showing the first signs of economic stabilization. There are moderate growth prospects for 2017, and the economy is expected to accelerate in 2018.

Opportunities and challenges for the hotel industry

Economic upturn brings opportunities for the region

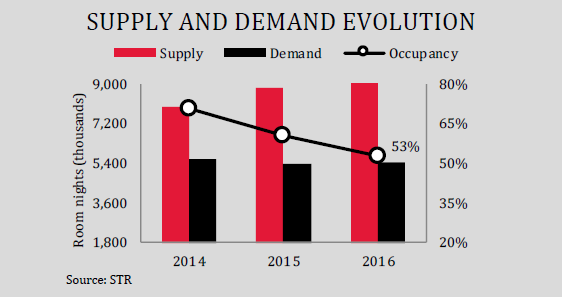

Even if the regional outlook was not too encouraging in 2016, the countries in question attained marked increases in the number of foreign tourist arrivals, with the exception of Argentina and Brazil that had a slight decrease due to their recession. In terms of hotel demand, all the cities analyzed here, except for the Brazilian ones, showed an uptrend, especially Bogota. Some markets were affected by hotel openings, particularly Rio de Janeiro, in addition to Curitiba and Belo Horizonte, which caused a drop in occupancy and, in most cases, in rates as well.

Although hotel supply will increase in some cities in 2017, the uptrend is expected to continue in line with the projected economic acceleration and the consolidation of destinations. This will contribute to a rapid reabsorption of supply and help several cities and segments keep attractive occupancy and average daily rate levels.

Having overcome uncertain times and with significantly lower risk, South America will grow again in 2017. This, in addition to the historical performance of the past 10 years, indicates good possibilities for the hotel industry in the region. Some of the current opportunities (many of which have been in place since the last edition of Outlook) are:

- Attracting foreign investors. On account of the dollar appreciation and a bet on regional economic fundamentals;

- New developments in cities with attractive RevPAR levels and increasing demand. The development of hotels in the economy and midscale segments is still at a budding stage in the region. Some markets also show opportunities in the upscale and luxury segments. In addition, leisure projects are stealing the limelight, especially for destinations with an expanding domestic market.

- Popularization of timeshare and fractional ownership, especially in Brazil. While the business hotel segment shows a new drop in performance, the leisure market growth continues to be significant. New developments have become feasible in the country;

- Improvement of operating efficiency in hotels in operation. In an increasingly competitive market and with better quality of supply, expanding revenue has become a challenge, especially in more economically vulnerable countries. In this context, seeking greater operating efficiency is critical to increasing profitability margins. Reviewing operating processes and recruiting the assistance of asset managers will help achieve better results;

- Structuring new funding options. In Brazil, for instance, structuring a condo hotel is no longer an easy option. On the other hand, one of the greatest risks in the sector has considerably decreased – oversupply. Better qualified investors are more likely to arrive in Brazil;

- Chains have increased conversion efforts. The participation of independent hotels predominates in the region. The challenge lies in finding properties meeting the brands’ requirements.

Market Overview

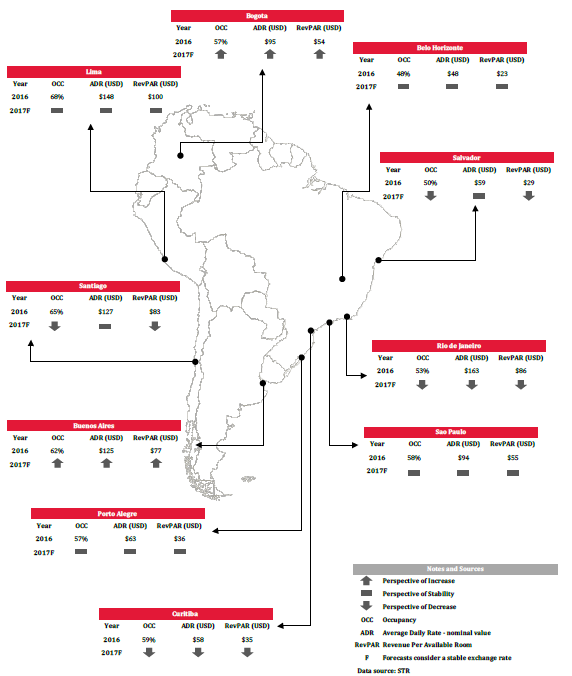

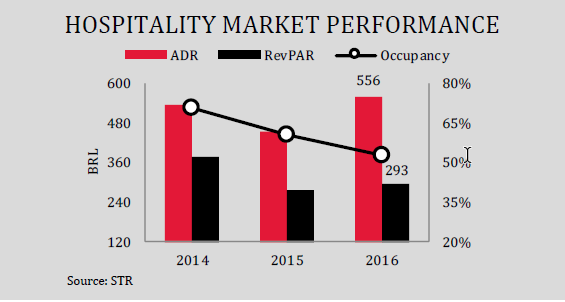

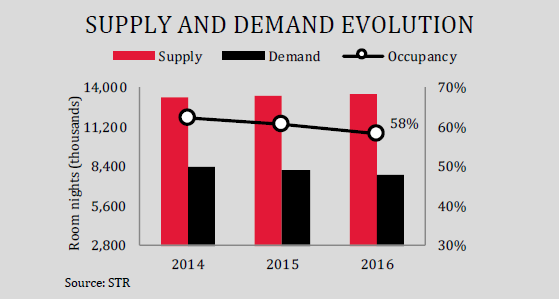

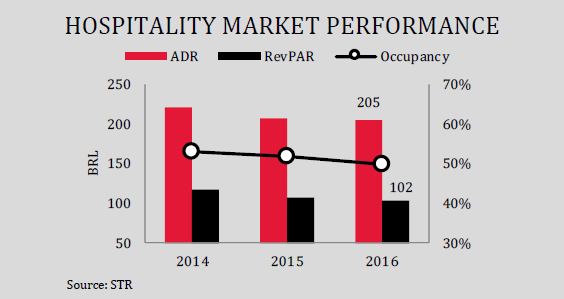

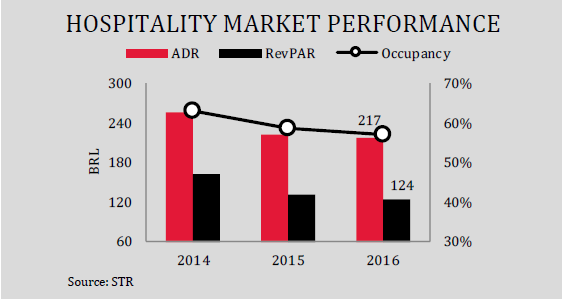

Argentina – Buenos Aires

Change of trend. The first recovery signs already evident

- 2016: A year of transition and of economic redirection. During his first year in office, Macri’s government implemented a series of adjustments and reforms aimed at reducing macroeconomic imbalances. Although, as expected, this had a negative impact on employment, inflation, and real wages, affecting consumption and investment, the foundations for Argentina's growth in 2017 were laid in 2016.

- Change of trend and positive prospects for 2017. Although the economy is undergoing a process of recovery and there are still some adjustments pending, it is possible to see positive signs. The combination of higher real wages, an improvement in business confidence, and increased regional growth is expected to contribute to set the country on the growth path in the short term.

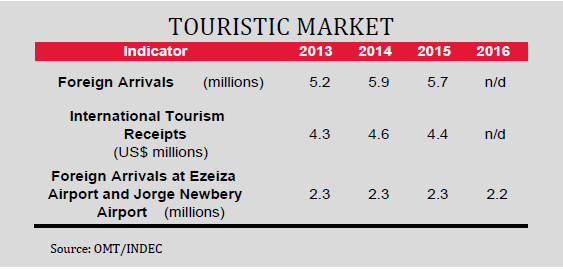

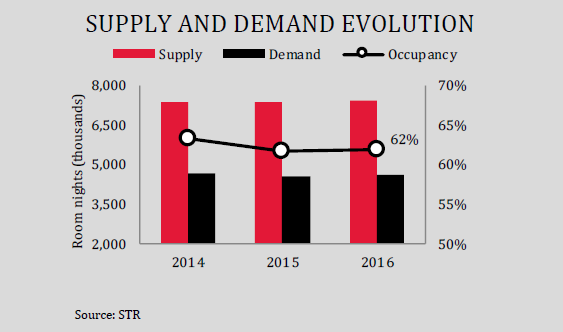

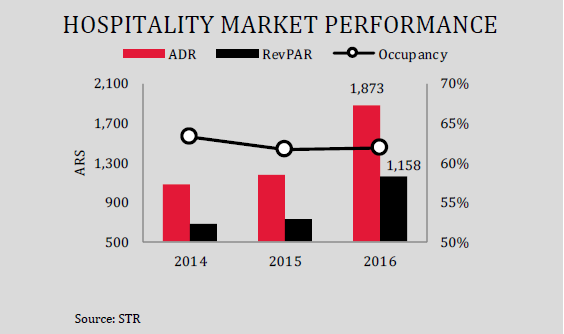

- Currency devaluation helped increase RevPAR and profitability in 2016. Despite the recession and the fall in tourist arrivals in the first months of the year, demand rose at a moderate pace above supply, thus increasing occupancy. As a result of this change in occupancy trends and of a highly dollarized market, rates in US dollars remained nearly unchanged, which led to an increment in RevPAR of 58.5% in local currency. This had a favorable impact on hotel profitability, albeit lessened by an increment in operating costs due to inflation and the elimination of utility subsidies.

- Stable supply and an improved economy bring opportunities for new developments. With fewer hotels to be inaugurated, an improvement of economic prospects, and the actions implemented by the government to foster tourism (such as the refund of 21% VAT to foreigners), Buenos Aires should increase its occupancy and rate levels in 2017. There are new projects under analysis.

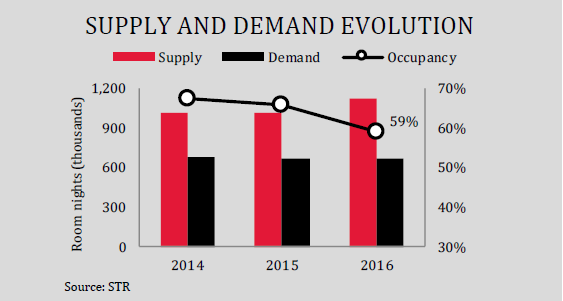

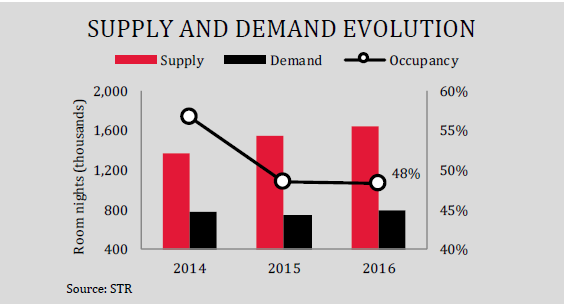

Chile – Santiago Market absorbing new supply. Good demand prospects

- Economic cooling-off in 2016. In addition to a drop in copper prices, the labor and tax reforms implemented by the government and the business discontent with the administration have had an impact on the business climate and have slowed down investment in the country.

- 2017: Election year, slight growth acceleration. Despite some uncertainty about the results of the forthcoming presidential elections in November, a slight upturn in the economy is expected in 2017, fueled by a moderate rise in copper prices and a more positive outlook both for Chile and the other countries in the region.

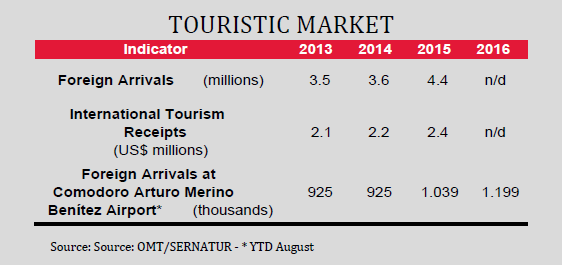

- Strong increase in tourist arrivals in 2016. Tourist arrivals in Chile increased by nearly 26% in 2016, especially on account of the marked growth of Argentine visitors living in neighboring provinces and traveling mostly on a shopping spree.

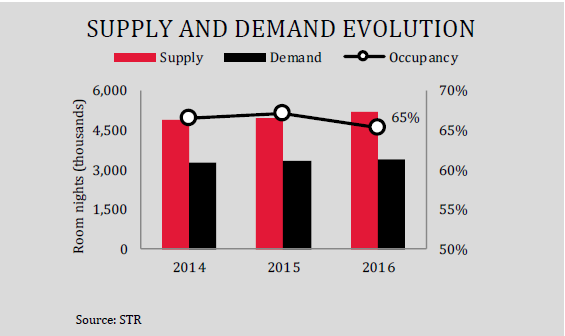

- Supply growth exceeds demand growth in 2016. Despite an increment in visitors and hotel demand in Santiago, the growth in supply led to a drop in occupancy.

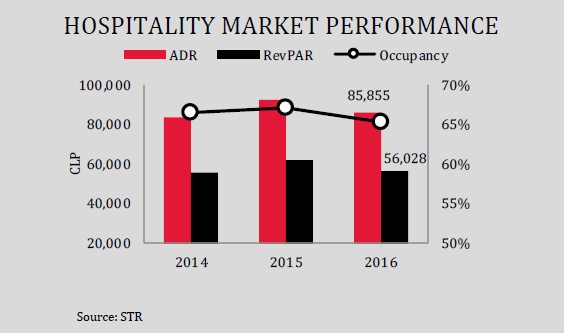

- 7.1% drop in average rate in 2016. The drop in the average rate in 2016 is accounted for by two main reasons; the 2015 Copa América that allowed for high rates during the year, and a drop in occupancy in 2016, which made the market more competitive thus hindering rate increases.

- Positive demand prospects. Foreign visitor arrivals are expected to grow at a higher rate than the economy. Although occupancy in Santiago will be affected by new openings in 2017, the city has showed a fast capacity to absorb supply, which will help keep attractive occupancy and average rate levels.

Colombia – Bogota High demand growth indicates rapid supply absorption

- Economic slowdown in 2016. The cooling-off in economic activity in 2015 extended to 2016 as a result of a rise in inflation and currency devaluation. In December, Congress passed a tax reform bill aimed at increasing tax revenue and helping the country keep its credit rating amid a slump in oil revenue, thus guaranteeing macroeconomic stability and long-term growth.

- Change of trend in 2017. The increase in commodity prices, infrastructure investment, and industrial production will accelerate economic growth in 2017.

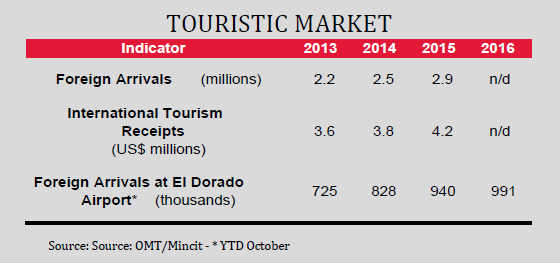

- Strong growth of international tourism. The continuous improvement of Colombia’s international image, the signature of the peace agreement, the actions promoting the country as a travel destination, and a competitive exchange rate have contributed to a double-digit growth of international tourism.

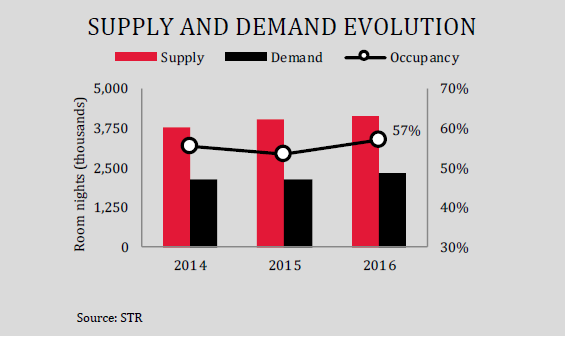

- Occupancy grew by 6.2% in 2016. Just like international demand, domestic demand showed a very positive trend in 2016, so that the supply inaugurated during the year was rapidly absorbed, leading to a strong increment in occupancy.

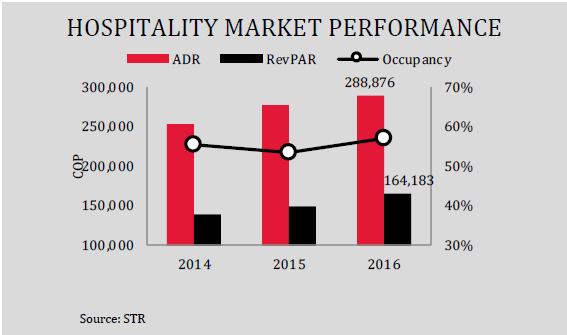

- Moderate rise in average rate. In 2016, the average rate went up, albeit below inflation. Considering an average market occupancy under 60% and a slowdown in economic activity, hoteliers were left with little room to adjust rates.

- A rosy horizon. Although new openings are scheduled for the next months, the growth of demand is expected to exceed that of supply. The end of tax benefits for the construction of new hotels will slow down the pace for the development of new projects. In this scenario, performance prospects for the sector are positive.

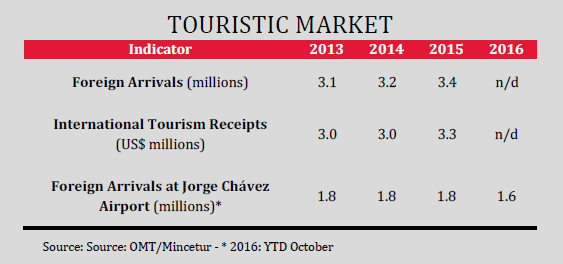

Peru – Lima Solid economic indicators and outstanding hotel performance

- The region’s greatest economic growth. Although presidential elections put the economy on hold during the first half of 2016, Peru showed an acceleration and attractive growth in economic activity during that year, thus becoming the star of the region. The expansion of its iron and copper production capacity as a result of the commissioning of new mines, together with the recovery of the manufacturing sector and traditional exports were the major factors that accounted for such performance.

- Expectations of economic acceleration in 2017. The favorable image of the newly sworn-in president and the actions to be implemented, the improvement of foreign demand and the return to growing fixed investments indicate that the economy will expand in 2017.

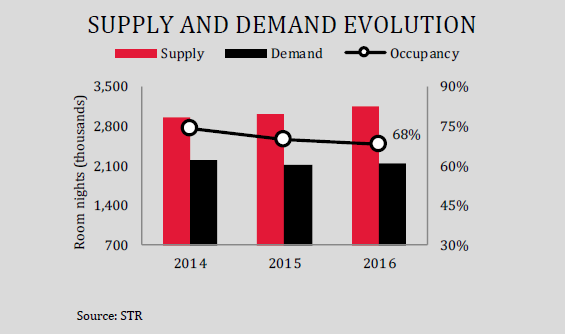

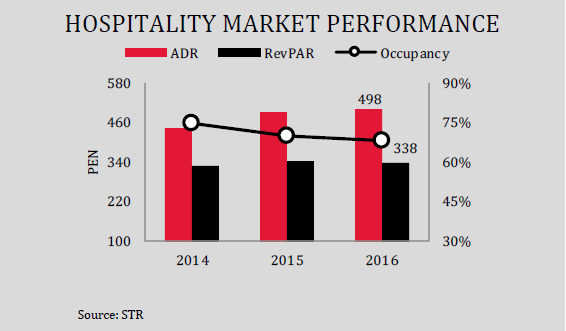

- The new influx of supply led to decreased occupancy. Despite an increase in demand in 2016, growth was moderate as the first months were slack for hotels in Lima due to the presidential elections. The impact of the new supply inaugurated in 2016 and at the end of 2015 exceeded demand growth, which caused a drop in occupancy, still in attractive levels at 68%.

- 1.2% drop in RevPAR. The fall in occupancy led to a more competitive market, with a 2% increment of the average rate in local currency and therefore a lower RevPAR below inflation.

- Attractive performance and good economic prospects. Despite the expected increase in supply until 2020/21, which could affect hotel performance in the short run, Lima has excellent growth prospects for the economy and tourism. Therefore, the new influx of supply is expected to be absorbed in the short run and the city should keep high occupancy and average rate levels.

Brazil After adjustment period, expectations of growth resuming

- Expectations of better macroeconomic indicators already in 2017. Focus Bulletin forecasts a slight GDP growth, inflation at the center of the target, and interest rates around 9% YOY. Consumer and business confidence indexes have improved and a new cycle of economic growth is expected to begin.

- Proposals under study might benefit domestic and international tourism. Some of the main proposals include Visa exemption for some foreign nationals (from USA, Japan, Australia and Canada) and gambling legalization. The impact on tourism will not be right away; however, if approved, such actions can encourage new businesses in the country's tourism sector.

- Olympic Games: A positive showcase for the country. In the opinion of the media and the general public, the event was a success and created a positive image for Brazil. In a survey conducted during the Games, 90% of respondents answered they were willing to return to the country.

- Regulating condo hotels will help improve hotel performance in the country. The actions of the CVM (The Securities and Exchange Commission of Brazil) in the condo hotel market, together with the sector’s lack of financing, will limit the arrival of new developments in the country. On the other hand, this situation will benefit projects with good financial prospects as, with more restrictions for the development of new projects, one of the major risks of the hotel business, i.e. oversupply, decreases in the hotel business, and the performance of hotels already in operation improves in the medium term.

- Fractional and timeshare: In spite of the crisis, the leisure segment keeps growing. As already happened in mature markets, timeshare and fractional ownership options are stealing the limelight in the country. Several opportunities for new developments are under study in Brazil.

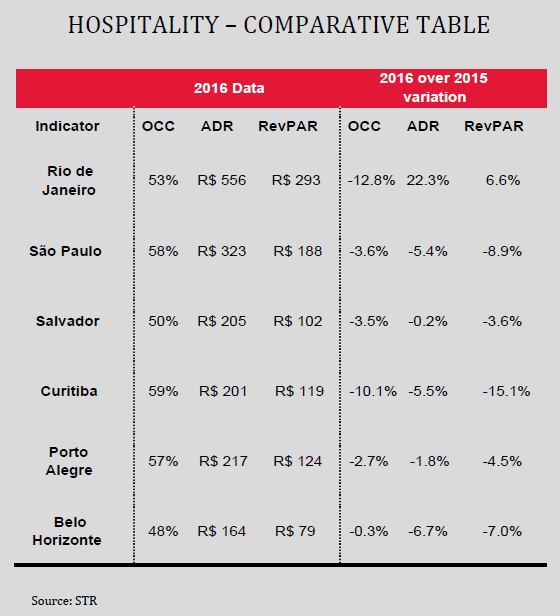

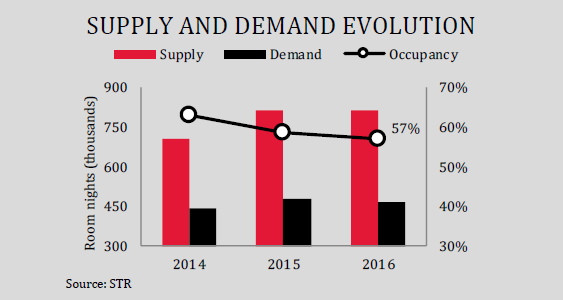

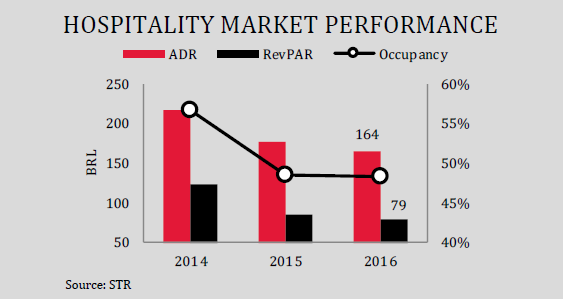

Rio de Janeiro After the Olympic Games, Rio’s hotel market faces challenging scenario

- Olympic Games: A positive impact on average rate. Apart from Brazil’s positive image to the world, local hoteliers were able to charge high rates during the event, so that the average rate went up by 22% in the year.

- Steep hikes in supply. As a host city of the Olympic Games, hotel supply increased with over 10,000 rooms in 2016. Once the Games were over and with the country’s crisis, performance levels dropped, with no indication of reaching its historic high before 2020.

- Events and leisure, performance recovery options. With new hotels and event infrastructure, the induction of demand in the leisure and event segments may be an option to improve performance in the medium term. To this end, it is critical to develop public-private initiatives and focus on public security.

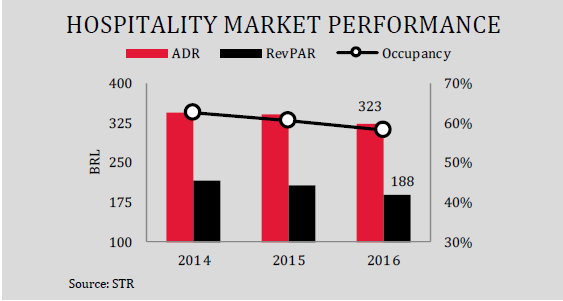

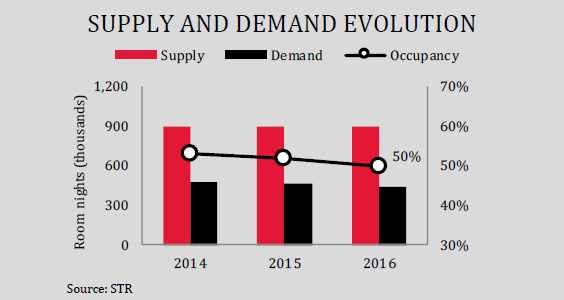

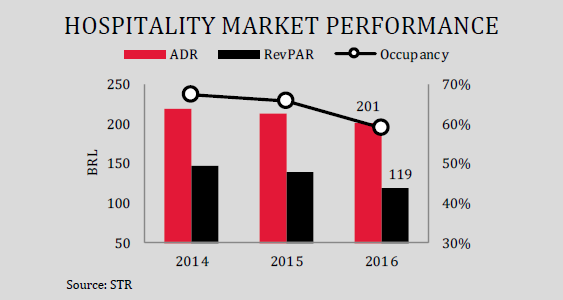

São Paulo Without new supply, recovery will be faster than in other markets

- Asset valuation trend in the medium term. Despite a drop in RevPAR in 2016, the return to a growth path and the restrictions to consolidate new projects will help recover asset value in the medium term.

- Larger leisure market share. The greater number of shows and leisure activities in the city, together with the implementation of more attractive rates over weekends, has encouraged hotel occupancy, especially in the midscale market.

- Sao Paulo boasts the best opportunities for new hotels in Brazil. In the medium term, it is the destination with the fastest recovery potential, as there have been no new projects developed in recent years. Modern and well located projects with a strong brand may have good results.

Salvador Another year of demand drop in the city

- Convention Center collapse and closure of Pestana Bahía. The city lost two major spaces for holding events. The Convention Center that was being refurbished collapsed and there is no information about its reconstruction. The Pestana Bahía hotel, featuring a convention Center, closed in February.

- Improved city image thanks to investments in urban regeneration. The public investments made in the Historic Center, the Rio Vermelho quarter, and along the entire seafront promenade in Salvador have turned the city into a more attractive place for its inhabitants and visitors.

- New hotels. Despite the recent economic shrinkage, the city will incorporate two new hotels in 2017 – Adagio Salvador (February) and Fera Palace Hotel (March), thus increasing competition in the sector.

Curitiba In a year of crisis, hotels felt the opening of new projects

- The crisis and the expansion of supply had an impact on the local hotel market. After a few years of stable performance, the sample analyzed in Curitiba showed the sharpest fall in RevPAR compared to the other markets under study. This was mostly due to the economic crisis and a rise in supply in 2016.

- Prospects of decreased performance in the short run. With more inaugurations scheduled for 2017 and with demand growth dependent upon an improvement of the national economy, hotel competition will be fiercer. In order to mitigate these effects, local hoteliers should focus on rate strategies and cost control.

Porto Alegre With low new supply expectations, hotels depend on economic upturn

- A new oversupply crisis is not an imminent risk for the city. After the inauguration of new hotels in 2014 and 2015, there are no plans for a large number of new developments in Porto Alegre, at least in the short term. In 2017, only one hotel of the Intercity chain is scheduled to open.

- The regional crisis increases the effects of the national economic recession. The regional scenario is an additional problem in terms of demand. The Rio Grande do Sul state is undergoing a crisis, with problems in public utilities and fewer local investments. The lower capacity to attract local businesses may extend the performance recovery period for hotels in the gaúcha capital city.

Belo Horizonte Supply stability horizon, with gradual recovery in upcoming years

Onset of supply stability. After several years of significant increase in hotel supply, 2016 had fewer hotel rooms entering the market. The scenario indicates the beginning of stability given that there are few projects scheduled to open in the short term. Occupancy levels remained stable. However, with rates dropping due to strong competition, the RevPAR kept falling. Belo Horizonte is not ranked among the country’s major leisure travel destinations. With the country’s economy picking up and stable hotel supply, the sector’s performance indexes tend to recover. However, there is a need for local investment in leisure and event venues to increase the city’s attractiveness as a travel destination and thus accelerate the hotel segment recovery.