By Daniel J Voellm and Nicholas Hu Runheng

BACKGROUND  High-tech development zones, areas representing the cutting edge of the high-tech industry, have been a driver of the economy and a window to the outside world for many cities in mainland China. Since 1991, the State Council has approved 105 national High-tech Zones in total, most of which cater to the heavy industries. However, with the continual development of China and the appearance of China’s current ‘L’ economy, these High-tech Zones begin a transformation process and seed new industrial clusters, with an increasing share of producer service and financial services. For example, in the Bejing Zhongguancun Science Parkthe added value of the producer service industry in 2015 was doublethat in 2005, accounting for almost 50% of GDP in Beijing Zhongguancun Science Park. Producer services normally includes financial services, information services, technology services, commercial services and distribution services

High-tech development zones, areas representing the cutting edge of the high-tech industry, have been a driver of the economy and a window to the outside world for many cities in mainland China. Since 1991, the State Council has approved 105 national High-tech Zones in total, most of which cater to the heavy industries. However, with the continual development of China and the appearance of China’s current ‘L’ economy, these High-tech Zones begin a transformation process and seed new industrial clusters, with an increasing share of producer service and financial services. For example, in the Bejing Zhongguancun Science Parkthe added value of the producer service industry in 2015 was doublethat in 2005, accounting for almost 50% of GDP in Beijing Zhongguancun Science Park. Producer services normally includes financial services, information services, technology services, commercial services and distribution services

Meanwhile, the rise of these High-tech Zones attracts massive investments from real estate developers driving investment in office, retail, residential and hotel assets, providing essential complementary uses with supporting facilities and amenities to the High-tech Zone. The study of hotel development in the urban fringe of High-tech Zones provides clues as to which factors will have a direct impact on the hotel’s location, grade and classification in the different stages of the High-tech Zone. Therefore, we selected six representative High-tech Zones from domestic tier-1 and tier-2 cities, which include Beijing, Shanghai, Shenzhen, Xi’an, Chengdu and Wuhan. The study focuses on the development of industrial clusters and the different derived real estate types in these six High-tech Zones as well as the ratio of each hotel type in terms of guest rooms. The article reveals prevalent trends in these regional hotel markets and gives recommendations to parties interested in investing in High-tech Zones. Sources of the article are from the official website and annual report of each High-tech Zone, CNTA and HVS research.

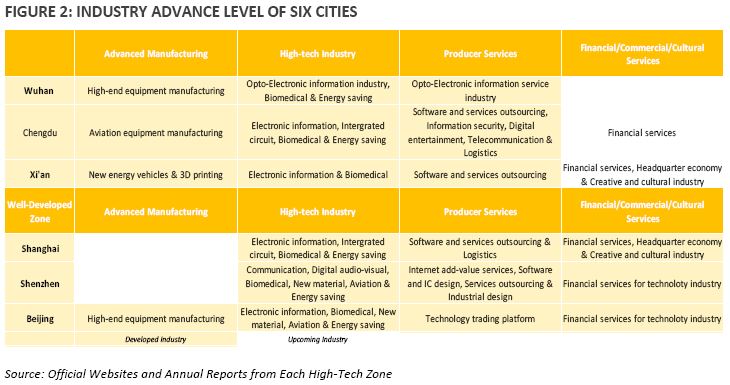

Our research shows that most industries in High-tech Zones can be divided into three major industrial categories: advanced manufacturing, high-tech and producer services, whereas producer services includes financial and commercial services as well. In terms of development stage, Tier-1 cities’ High-tech Zones such as Beijing, Shanghai and Shenzhen have reached an advanced and mature stage, with a more stable and complementary industrial structure. Within the High-tech Zones of Beijing, Shanghai and Shenzhen, producer services account for 48.9%, 47.0% and 53.0% of the total, respectively, while financial services account for 19.1%, 7.0% and 11.0%. However, the High-tech Zones of Xi’an, Chengdu and Wuhan are still mainly dependent on the advanced manufacturing and high-tech industries. Within the High-tech Zones of Chengdu and Wuhan, producer services account for 14.7% and 26.5% of total respectively.

While, within the High-tech Zones of Xi’an, Chengdu and Wuhan, financial services only account for only 3.0% or less, which are much lower than in the three Tier-1 cities. Beijing became the first city in China to develop into a service dominated economy, then followed by Shanghai, Shenzhen and Guangzhou. These Tier 1 cities have upgraded their industries far ahead of Tier-2 cities, while the respective business environments are more mature, more established and more international. In the new millennium, these four Tier-1 cities took the lead in the economic restructuring process from production manufacturing to producer services. In general, Tier-2 cities trail this trend, while Tier-3 cities are exploring their opportunities here.

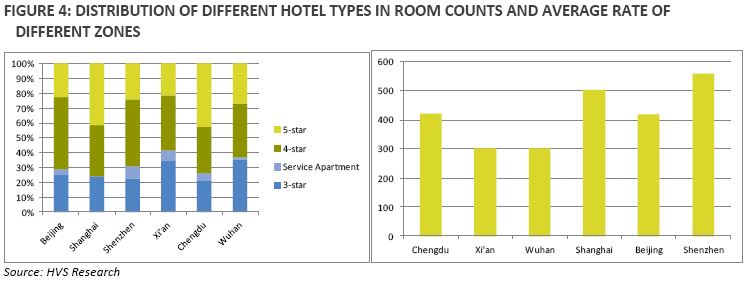

Through comparisons of development among the six High-tech Zones, it is evident that hotel grade and the average rate in the zone are directly under the influence of industry types and show a positive correlation. Among the six High-tech Zones, those of Beijing, Shanghai and Shenzhen are more advanced through more intensive producer and financial services. As well, four-star hotels and five-star hotels in these three Zones represent a larger share, and the average rates in these three zones are relatively higher than the average rates for the zones in Chengdu, Xi’an and Wuhan. The presence of producer and financial services in High-Tech Zones are generally better demand generators to support high-end hotels and drive overall market performance.

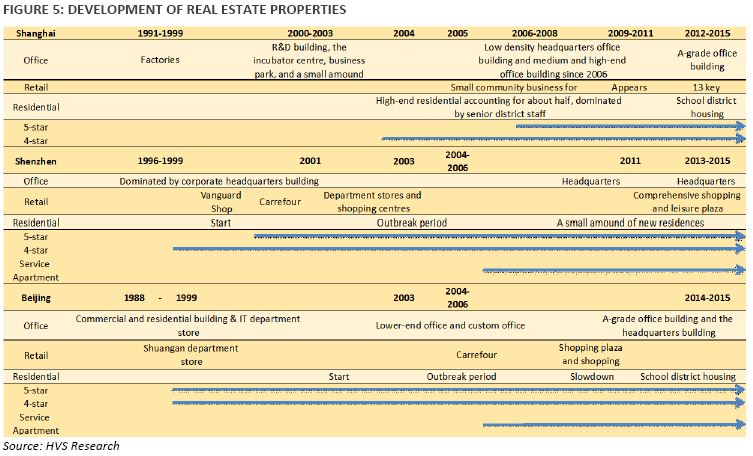

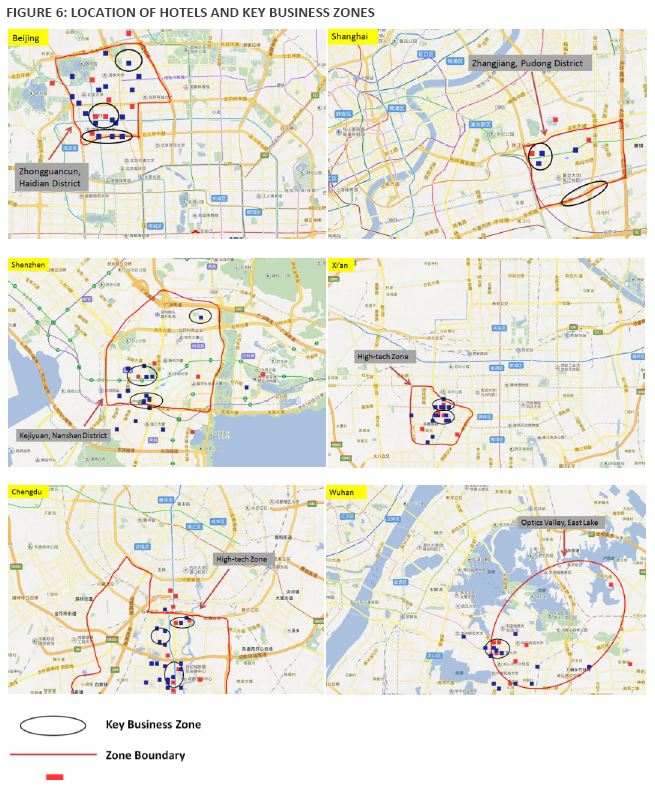

DIFFERENT REAL ESTATE TYPES Through comparison among the High-tech Zones of Beijing, Shanghai and Shenzhen in terms of its development, HVS finds that hotel distribution is closely related to the business environment, in addition to the effect of industry type.

In the early stage, there were mainly industrial plants and commercial office blocks, with lack of supporting commercial facilities, no housing developments and, if at all, budget hotels. Then, following the developments of medium and high-end offices and headquarter buildings, commercial and residential complexes led way to the emergence of four-star and five-star hotels. However, given that many developments were facing pressure from Chinese governments or local authorities, quite a few four-star and five-star hotels were built owing to government requirements. In the further stage, business climate and living atmosphere became much stronger, mirrored in the emergence of high-end office building and complete commercial facilities in the region. Moreover, the supply of five-star hotels increased, meanwhile, service apartment appeared.

Development timing of four-star and five-star hotels will be affected by multiple effects of office development and commercial development. Four-star hotels are usually developed in the early stage to meet basic business traveller needs; after the High-tech Zone matures, five-star hotel gradually appear; service apartments get built in the Zone as a byproduct of large-scale office buildings, forming a complete commercial and residential communities. Service apartment also serve as an alternate commercial use in areas where office demand is soft.

The positioning of hotels in a zone are impacted by factors such as the industry type, company size and the grade of office building. Typically, high value-added industries, medium and large enterprises, foreign-funded enterprises and A-grade offices are essential for supporting high-rated hotels. From the distribution of commercial facilities and high-end hotels in High-tech Zones of Beijing and Shanghai, it is easy to find that site selection of high-rated hotels in High-tech Zones always is associated tightly with the location of commercial facilities. The clustering effect provides the support for high-rated hotels.

DEVELOPMENT OF HOTEL BRANDS With the development of industry and property, the high-tech zone’s hotel market has developed from a budget hotel dominated market to a new market of high-end hotels and service apartments. This trend is reflected in the type of hotel brands present, from local brand to domestic renowned brand then to international renowned brands under international operators, like Starwood, InterContinental, Hilton and Marriott, even to some luxury hotel brands of smaller operators, like Rosewood, Niccolo, Puli and The House Collective in certain high-tech zones. However, robust economic growth has led to inaccurate forecasts, resulting in mismatched positioning of upscale hotels in some markets.

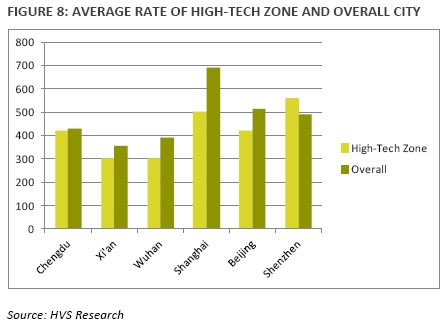

From HVS research, the average rate of High-tech Zone is normally lower than overall average rate of the city, which implies the hotel market of High-tech Zone is relatively less developed compared to other hotel development hubs like CBD. Hence, HVS suggests that hotel developers should look into investing in midscale properties in high-tech zones for lower cost of capital with more attractive returns.

From HVS research, the average rate of High-tech Zone is normally lower than overall average rate of the city, which implies the hotel market of High-tech Zone is relatively less developed compared to other hotel development hubs like CBD. Hence, HVS suggests that hotel developers should look into investing in midscale properties in high-tech zones for lower cost of capital with more attractive returns.