advertisement

|

News for the Hospitality Executive |

advertisement

|

The Ground Rent

Alternative

By Joseph Pierce December 2011 You have found the site that fits your development needs in a market that complements the improvements you want to develop. Unfortunately, the desired site is either not for sale or is available at a price point outside your development budget. While purchasing the site may not be an option, renting the land may work to the advantage of the developer as well as the land owner. The developer can direct financial resources to the construction of desired improvements without the need to purchase the site. The landlord benefits from a steady income, the security of a long-term tenant, and future appreciation of property value derived from the improvements. A ground lease is an enforceable contract which creates a landlord’s and a tenant’s interest in a defined parcel of land. Usually the ground lease is a long-term lease of land with the tenant permitted to improve or build on the land and enjoy those benefits associated with the improvements for the term of the lease. Improvements made by the ground lessee typically revert to the ground landlord at the end of the lease term. Aside from the financial benefits available to the landowner for entering into a long-term lease, there must be sufficient financial incentive for the prospective tenant/developer to commit time, effort, and capital into undertaking site and building improvements and there must be sufficient length over which the prospective developer can recapture his investment. For an income producing property such as a hotel, the developer’s ground lease obligation generally does not begin until occupancy of the property can commence. During the construction process, the developer will need to acquire a construction loan. After completion of the project the developer will need to transition the construction obligation into a long-term permanent financing. The term of the ground lease must be of sufficient length to allow the developer to obtain third-party mortgage financing and on terms and conditions that make the proposed development financially feasible. Depending on the use of the land and the scale of the development, amortization of major leasehold improvements in most instances will require a minimum of 40 years to permit the lessee to recover his investment and facilitate leasehold mortgage financing, with most long-term leases running 50 to 99 years. In considering a ground rent agreement, we have examined three distinct options:

Fixed Rental A fixed rental is a negotiated ground rent in which the landlord and tenant agree to a fixed fee to be paid for the duration of the lease agreement. Both parties benefit from knowing the precise income stream/lease expense year over year and can budget accordingly. For the landlord, the fixed rental needs to be sufficient to cover the land acquisition costs, any land preparation costs to make the property “site ready,” and the opportunity costs associated with committing the property to the negotiated ground lease versus other potential returns. The landlord runs the risk that the value of the site may well exceed the return of a fixed annual payment over a 50- to 99-year lease term. However, the fixed annual return has a strong appeal in calculating the return of the landlord’s initial investment and the prospect of steady future income. For the tenant, the prospect of a fixed, predetermined rental payment is a reliable budget tool. Additionally, in cases where mortgages are subordinate to the lease rental payment, mortgage lenders prefer the reliability of a fixed lease component that will not unexpectedly change over the term of the mortgage. For the developer, a fixed rental ground lease has two distinct disadvantages. First the rental payment once established is not responsive to current market activity. Thus, should business activity decline, the fixed ground lease becomes a proportionally increased burden to the development. Additionally, new business activities have a start-up period until they reach a stabilized level of business activity. A fixed rental ground lease which provides a reasonable return for both parties in a stabilized year may jeopardize the operation of the new business in its early years and not allow it to stabilize. To overcome shortfalls in the fixed rental ground lease the parties could agree to:

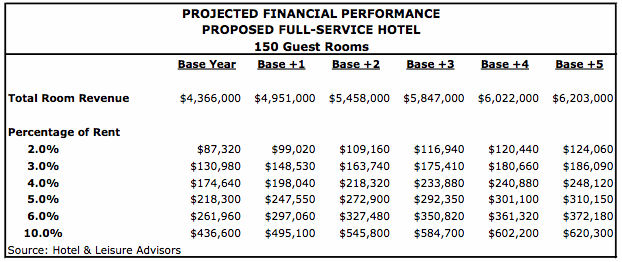

Percentage of Revenue When a ground lease is negotiated with an income producing property, a percentage of revenue lease payment is a possible option. The percentage of revenue can be calculated based on gross revenue or the various revenue components which comprise the gross revenue. The use of the percentage of revenue method allows both the landlord and the tenant to share the risk of a changing market. Once percentages are established, each party to the lease can reasonably budget the ground rent payment for the following year. For the landlord, the percentage of revenue ground lease provides the opportunity to experience income growth in excess of the land acquisition costs, site preparation costs, and the expected rate of return the landlord had anticipated. This method also provides a profit motive to support the tenant via direct usage and with business references. However, there is no guarantee that the income producing property will produce sufficient revenue to cover the landlord’s costs and expected return. Unless negotiated in the ground lease, the tenant will have no obligation to make-up the shortfalls. For the tenant, a percentage of revenue ground lease creates a de facto partner in the landlord. As rental payments are subject to revenue generation, the tenant will be requested to open their books to review by the landlord. Additionally the rental payments are based on the success of the business developed on the site, not necessarily the improved value of the land. A strong business operator will pay a higher rent than an average operator although the site has not changed. However, under this method the tenant acquires a partner who assumes a portion of the business risk associated with a market downturn. The rent will decline with a reduction of revenue. Additionally, this method accounts for the ramp-up period experienced by new businesses. At the beginning when revenues are lower the ground lease is lower, but as the property moves toward stabilization the rental payments will advance accordingly. In the following table the property would

experience increased lease payments year over year based on growth in

room revenue generated by the property. The table is based on a

150-room full-service hotel, entering the market with occupancy of 55%

and average daily rate (ADR) of $145. The property is projected to

stabilize in the fourth year of operation (Base +3) at approximately

65.5% occupancy and ADR of $163. For this example, the property will

experience inflationary growth of 3% in year Base +4 and beyond.

The table shows the impact on rental income with the growth in total room revenue year over year and with an increase in the percentage. For this example, we limited the discussion to room revenue while other full-service hotel revenue components could be incorporated into the calculation. Such revenue components could include restaurant, lounge, meeting space or conference center rental, and retail outlets. Additionally, the percentage of rent calculation could vary based on the revenue component. Thus, a hotel constructed as a tower requiring a proportionally small site footprint may be charged a different percentage rent than that of the adjoining conference center that occupies a large site footprint. Percentage of Appraised Value A ground lease which is based on a percentage of the appraised value of the land is similar to that of a fixed rental lease. However, where a fixed rental lease is negotiated at the beginning of the agreement and generally remains unchanged through the life of the contract, a percentage of appraised value ground lease utilizes rent reset provisions and revalues the lease based on current or updated appraisals at predetermined intervals throughout the contract. With this type of lease arrangement the landlord and tenant agree to lease payments based on the value of the land only. At the beginning of the lease, the subject site is appraised “as is” prior to the income producing improvements being constructed. Based on the appraised value, the parties to the ground lease negotiate a rental payment based on a percentage of the appraised value. This rental payment is fixed for a negotiated period of time, generally 10 years. At the conclusion of the 10 year period, a new appraisal is commissioned. The appraiser is instructed to ignore both the improvements and the lease itself, valuing the land in a fee simple context and as if unencumbered. The resultant appraised value is then multiplied by the contracted percentage rate, resulting in the new ground lease rent for the next 10 years. This process is the only one that is tied exclusively to the land. For the tenant, the risk rests with the expectation that business activity associated with the improvements will grow at least to the level of the growth in land value. Should the land value grow faster than the business activity of the improvements, the new lease rates may be detrimental to the ongoing operation. Additionally, it may be more difficult to finance a development on leased land for which ground rents have not been predetermined. As ground rent payments may take priority over any mortgage payments associated with leasehold improvements, the mortgage lender has no practical way of protecting its financial interest against unanticipated spikes in future ground rent payments. This may overwhelm the earning capacity of the leasehold improvements and cause the lessee to default on the ground lease, putting the leasehold mortgagee at financial risk. For the landlord the sudden spike in lease payments may force the tenant into default, leaving a windfall of improvements that the landlord is neither prepared nor willing to operate. Additionally, the reset lease terms may create an environment in which a viable lessee alternative may not be available and with lease length terms too short to finance. A lease term with less than 20 years is generally considered not suitable for mortgage financing. Depending on the scale of development and major leasehold improvements a minimum of 40 years may be needed to permit the developer to recover his investment and facilitate leasehold mortgage financing, with most long-term leases running 50 to 99 years. Conclusion The development of a ground lease is a negotiated process that reflects the needs and expectations of the participants as well as market conditions. Variations of each of the above ground rent calculations can be incorporated into the final product, creating a contract that works for both tenant and landlord. Many real life examples of ground leases involve a combination of base rent and percentage rent. The use of a combination of base and percentage rent provides the ground lease landlord with the security of a fixed or base rental payment, but disburses some of the risk of performance to both the landlord and tenant. Additionally, the property pays an escalating percentage rent over the duration of the lease providing increased rent to the landlord for improved performance of the income producing property. While the construction of improvements on land not owned by the developer is less than desirable, the execution of a ground lease may be the only way to gain access to valuable real estate in an excellent location. The landlord potentially gains a steady stream of income and increased property value through development that the landlord may otherwise not have the expertise or capital to accomplish on their own. Author Joseph Pierce, Senior Associate is a Senior Associate with Hotel & Leisure Advisors. He received an MBA from Michigan State University’s hospitality program in 1981 and a Bachelor of Science in Accounting from the State University of New York at Brockport in 1978. He has a wide range of experience in operations and accounting in hotels and resorts. Mr. Pierce has been a Controller and Director of Finance and Accounting for Clarion, Renaissance, Marriott, and Westin Hotels. He also managed an independently-owned hotel, The Talbott Hotel in Chicago. Mr. Pierce has performed appraisals, market feasibility studies, consulting assignments, and impact studies nationally. He can be reached at 216-228-7000, ext. 23, or [email protected]. |

| Contact: Hotel & Leisure Advisors, LLC 14805 Detroit Avenue Suite 420 Cleveland, Ohio 44107-3921 Phone: 216-228-7000 Fax: 216-228-7320 |