advertisement

Tranche Warfare: The Coming Litigation

Among Stakeholders in CMBS Loans

Hotels' Distress Lead CMBS Delinquencies To Record Level

|

News for the Hospitality Executive |

advertisement

Tranche Warfare: The Coming Litigation

Among Stakeholders in CMBS Loans

Hotels' Distress Lead CMBS Delinquencies To Record Level

| By Jim Butler & Jeff Steiner, March 1, 2010

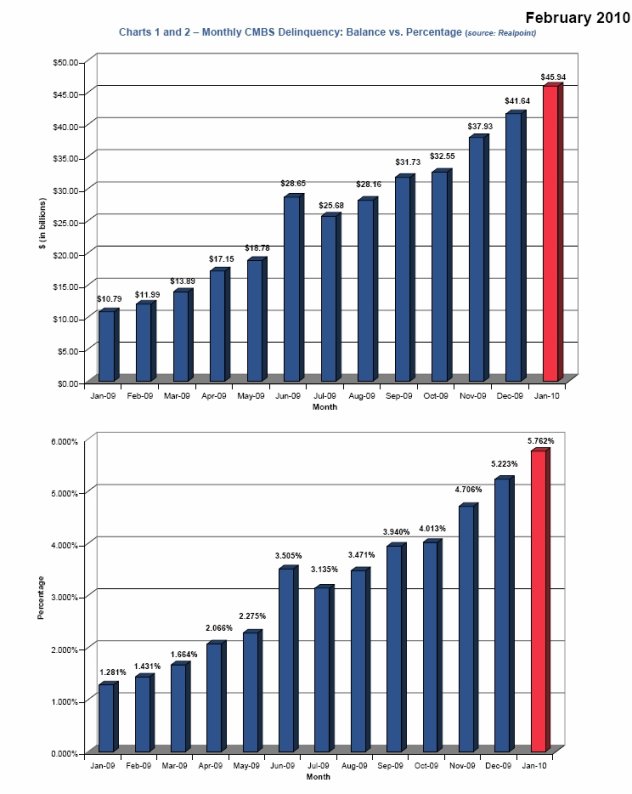

According to the Monthly Delinquency Report issued by Realpoint a few days ago, the total outstanding amount of CMBS (Commercial Mortgage Backed Securities) tracked by that firm is almost $800 billion, of which approximately $46 billion was delinquent in January 2010. The January delinquencies reflect a 326% percent increase from one year earlier when only $10.79 billion was delinquent (for January 2009). Realpoint projects that these CMBS delinquencies will rise to approximately $70 billion by mid 2010, and predicts that the current trend of ballooning loan delinquencies will continue, as reflected in these two charts.  The CMBS structure became dominant because it was so efficient. Prior to the current credit crisis, originators of CMBS loans were able to offer attractive rates and terms to commercial mortgage borrowers in part because of the efficient way in which the CMBS issuers were able to pool the loans in REMICs (Real Estate Mortgage Investment Conduits). CMBS issuers offered purchasers of interests in the loan pool (or individual loans in the pool) certificates representing ownership of pieces (or tranches) of the securitized loans or loan pools with different interest returns and priorities of repayment (the higher the priority of payment, the lower the interest rate that could be earned and vice versa). In larger loans, different return and risk profiles for investors were also created through a so-called A/B note structure, in which the A note has a higher priority of payment and lower interest rate than the B Note. A loan could also be carved up into more notes having different payment priorities and interest rates than just A and B, and ownership of each note could be divided into certificates representing varying payment priorities and interest returns. In some cases, not all the notes may be included in the CMBS loan pool, although pursuant to co-lender agreements among the noteholders, the entire loan will be administered by a single servicer at any given time. CMBS delinquencies and defaults will test conflicts of interest and likely lead to litigation, or "tranche warfare" among the classes of stakeholders Defaults will cause losses to junior positions. Higher delinquency rates and greater borrower difficulties in refinancing CMBS loans have led and will likely in the future lead to more and more conflicts or "tranche warfare" among stakeholders with different interests in the loans or pools -- among the certificate holders with differing priorities and control, the issuers that deposited the loans in the REMICs, those who sold the certificates, and servicers responsible for administering the loans in the REMICs. As delinquencies and subsequent losses mount, those holders of more junior tranches will take the first losses of income and principal. Many will be wiped out, and looking for misdeeds of others that caused their losses. (If only the loan had been liquidated quickly, worked out in a different manner, etc.) PSAs will set the standard of care. When the expected Tranche Warfare develops, the Pooling and Servicing Agreement (PSA), which is a key formative document in the creation of a REMIC, will map much of the battlefield. The PSA is a long agreement, usually 200-300 pages in length, plus exhibits. The parties to the PSA are (a) the sponsor of the REMIC, usually a Wall Street firm that has assembled the pool of loans from various originators, deposits the loans in the REMIC and sells the certificates representing ownership interests in the loan pool, a trustee (most commonly Bank of America, N.A. (as successor to LaSalle Bank National Association) or Wells Fargo Bank, N.A.), and (b) one or more companies acting as servicers of the loans. Typically, each REMIC has a master servicer that administers the loans until they go into default or are reasonably likely to go into default and a special servicer that administers loans in default or reasonably likely to go into default. While there is no single form of PSA in use for all REMICs, there are certain common elements typically found in all PSAs. Typical PSA "Servicing Standard" The servicing standard is the basic guideline that establishes the duties of the servicers with respect to administration of the loans in the REMIC. While the Servicing Standard may be expressed somewhat differently in each PSA, certain elements are commonly found in the statement of the Servicing Standard. Given the number of the elements and considerations incorporated in the Servicing Standard in an effort to balance the interests of the owners of the various tranches and the subjective language used, the Servicing Standard is likely to be subject to many different interpretations. The basic element of the Servicing Standard requires that the loans be administered in the best interests and for the benefit of all of the tranche holders, including those holding pieces of the loans that are not in the CMBS loan pool. However, the servicers are supposed to take into account the relative priority positions of the noteholders. No guidance is provided to the servicers as to how these priorities are to be "taken into account." As part of the Servicing Standard, the servicers are also supposed to administer the loans in accordance with laws, the PSA and any co-lender or intercreditor agreements among the noteholders. To the extent consistent with the foregoing requirements, the servicers are required to use a standard of care and skill consistent with that the servicer uses for administering loans for its own account or for other third parties, whichever is higher. The servicers are supposed to exercise this level of care and skill with the objective of maximizing the net present value of the recovery of the loan. Conflicts of interest by servicers The servicers may have conflicts of interests in servicing the loans based upon the possible ownership by the servicer of a tranche of the loan, compensation arrangements for the servicing, duties to make debt service and protective advances when serviced loans go into default and other business relationships with loan borrowers or other stakeholders. In cases where the originator or sponsor of the CMBS offering is also in the business of being a special servicer, it may hold the most subordinate tranche and also act as the special servicer, so it is not uncommon for such a conflict of interest to exist. Also, the most subordinate class of certificate holders generally has the right to replace the special servicer, subject to rating agency confirmation, creating another potential source of a conflict of interest for the special servicer. In summary, the Servicing Standard is a complex, multi-layered, subjective and ambiguous statement of the duties of the servicers-in other words, fertile ground for each side in the Tranche Warfare to manufacture ammunition for the battle. The final element of the Servicing Standard generally is one requiring the servicers to disregard these conflicts of interest, a worthy objective, but one that is likely to be very difficult for the servicers to do as a practical matter, and one that will undoubtedly be judged with the benefit of perfect hindsight. The bottom line: Why tranche warfare is coming Here is the bullet point executive summary on why tranche warfare is inevitable:

Jim Butler is a founding partner of JMBM and Chairman of its Global Hospitality Group®. Jim is one of the top hospitality attorneys in the world. GOOGLE "hotel lawyer" and you will see why. JMBM's troubled asset team has handled more than 1,000 receiverships and many complex insolvency issues. But Jim and his team are more than "just" great hotel lawyers. They are also hospitality consultants and business advisors. For example, they have developed some unique proprietary approaches to unlock value in underwater hotels that can benefit lenders, borrowers and investors. (GOOGLE "JMBM SAVE program".) Whether it is a troubled investment or new transaction, JMBM's Global Hospitality Group® creates legal and business solutions for hotel owners and lenders. They are deal makers. They can help find the right operator or capital provider. They know who to call and how to reach them. For more information, please contact Jim Butler at [email protected]. or 310.201.3526. |

| Contact:

Jim Butler

|

| Also See: | Insights on the New CMBS Rules - Dawning of a New Era, or Error of a New Dawning? Implications for Troubled Hotel Loans / Jeff Steiner and Jim Butler / September 2009 |