advertisement

Executive Summary of the 2nd Qtr U.S.

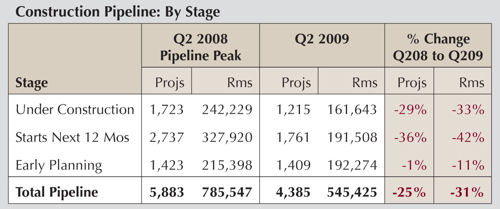

Hotel Construction Pipeline

Cancellations and Postponements at Record High of 507 Hotels/76,726 Rooms

.

|

News for the Hospitality Executive |

.

Forecast for

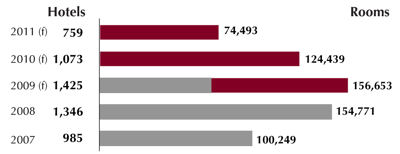

New Hotel Openings  For the first time, Lodging Econometrics (LE)

has compiled and announced its forecast for New Hotel Openings for

2011. New

hotel openings are projected at 759 hotels/74,493 rooms. LE has also

adjusted

its forecasts for 2009 and 2010. The 2009 forecast has been reduced to

1,425

new hotels/156,653 rooms, down by 5,036 rooms, a decrease of 3%. The

2010

forecast has been adjusted to 1,073 projects/124,439 rooms, down 21,277

rooms

or 15%. For the first time, Lodging Econometrics (LE)

has compiled and announced its forecast for New Hotel Openings for

2011. New

hotel openings are projected at 759 hotels/74,493 rooms. LE has also

adjusted

its forecasts for 2009 and 2010. The 2009 forecast has been reduced to

1,425

new hotels/156,653 rooms, down by 5,036 rooms, a decrease of 3%. The

2010

forecast has been adjusted to 1,073 projects/124,439 rooms, down 21,277

rooms

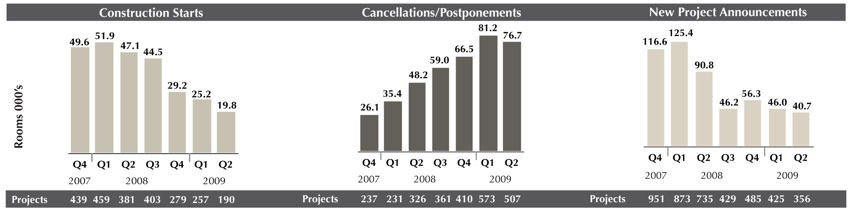

or 15%. These forecasts are lower than what might be first thought based on the size of today’s pipeline. For larger projects, there is no new lending available for “take-out” mortgage loans. Presently, neither loan syndication or loan securitization systems are functioning. Government programs to remove toxic mortgages from bank balance sheets are slow in coming. Investment incentives to restart securitized lending are just beginning to surface. It’s a very slow process and is not expected to change the lending landscape for lodging any time soon. The priority for banks is to continue to reserve against future balance sheet problems, leaving little room for originating new loans. Only selected, smaller projects are still able to obtain new financing at the community level. Meanwhile, lodging operating statistics have continued to show declines through June. The rate of decline is hoped to moderate starting late 2009. However, future growth will likely remain flat for a prolonged period as the pace of economic recovery for consumer and business spending is anticipated to be slow. Key Pipeline Metrics  Developer sentiment, which is changing rapidly, is best expressed in the Key Pipeline Metrics. Construction Starts, almost a pure reflection of the lending environment, stand at a cyclical low of 190 projects/19,820 rooms in Q2. Only a relatively small number of projects have migrated up the Pipeline toward construction, while many others remain stalled. As these trends continue, LE expects more developers with stalled projects to cancel or to postpone until lending and operating trends improve. In Q2, Cancellations and Postponements reached a record high of 507 projects/76,726 rooms, making this the second consecutive quarter with cancellations at 500 or more projects. While Cancellations and Postponements always take place on a one by one basis, a new trend has recently emerged. Some developers have put their entire development portfolio on hold until another point in time as they move to preserve their capacity to deal with other issues in their operating portfolio. Finally, New Project Announcements (NPA’s) into the Pipeline, directly impacted by the precipitous operating declines, are at their lowest level in 18 quarters. At 356 projects/40,682 rooms, NPA’s are down 68% by rooms from Q1 2008’s cyclical peak. This trend will continue in a low channel until early next decade.

ABOUT LODGING ECONOMETRICS With over 30 years of experience, Lodging Econometrics (LE) is the foremost source of global business development intelligence for hotel franchise companies. LE serves as your strategic planning partner. We identify every opportunity available to your company worldwide, based on your particular market share goals, sales objectives and brand specifications. For more information about LE’s complete report on the United States Lodging Construction Pipeline or to inquire about any of LE’s other lodging real estate reports, please contact us at 603-431-8740 x19 or [email protected]. |

Contact: Lodging Econometrics |