advertisement

The Outlook For Hotel Investments

|

News for the Hospitality Executive |

The Outlook For Hotel Investments

| By Scott Smith, MAI

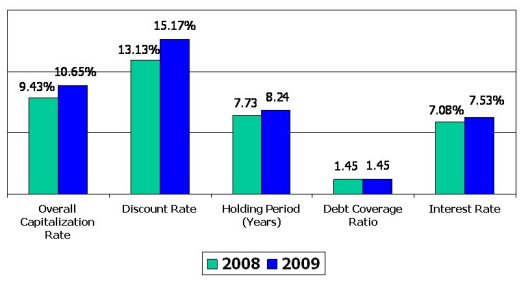

As we now live through the current economic recession and its impact on lodging revenues and expenses, it has become evident that investors anticipate continued declines in operating incomes and resulting loss in property values through the remainder of 2009 and into 2010. That being said, investors also expect the industry to rebound in 2011, and today�s distressed environment will provide exceptional investment opportunities to those buyers with the ability to take advantage. To gain a better understanding of today�s lodging investment environment, let us review the results of the 2009 edition of PKF Consulting�s Hospitality Investment Survey. Investment Criteria

Source: PKF Hospitality Research, 2009 Hospitality Investment Survey Mortgage Criteria

The lack of debt financing and the declining growth in income continues to increase the perceived risk premium for most hotel investors. As a result, the difference between expectations of buyers and sellers continues to be very wide. Investors are fearful of the near-term downside risk and see uncertainly and an unreliable upside. This has already resulted in very few transactions. However, as owners become increasingly compelled to sell (or lenders begin to foreclose), we expect the transaction market to improve in the latter half of 2009. These transactions will be limited to sales of single assets and smaller portfolios, and will include a lower asset class. Funding will be provided by private equity investors that have been anticipating deep discounts in price. Should poor operating profits and lack of debt financing continue to persist for the higher class of assets, we anticipate that buyers will have an unparalleled opportunity to purchase investment grade property at discounts ranging from 20 to 40 percent. As the most recent survey indicates, we have indeed entered into one of the most depressed periods in the lodging investment cycle. Most investors in our survey indicated that the downturn in the lodging sector will be deep and longer than anyone could have imagined. However, this is a cycle and each cycle has its recovery. Although current economic indicators are weak, investors are certain that exceptional opportunities will surface in the coming months as owners are forced to sell or raise additional capital. Our survey respondents expect capitalization rates to moderate and that hotel values in the short term will continue to decline as profits decrease. Only those sellers that have to sell � will, and at a discount. As in past downturns, distressed hotel sales taint the overall health of the lodging investment market. Those well capitalized owners with good quality assets in premium locations will hold for dividend yield and wait for the next cycle. The six-page 2009 Hospitality Investment Survey presents both investment

criteria (cap rates, IRR, equity yield, cash returns) and lending criteria

(LTV ratios, interest rates, loan terms, debt coverage ratios), as well

as three topical articles. To purchase a copy of the report for $250,

please visit www.pkfc.com/buyhis.

Scott Smith, MAI, is Senior Vice President in the Atlanta office of PKF Consulting � www.pkfc.com. This article was published in the June 2009 edition of Lodging. |

| Contact:

Robert Mandelbaum

|

| Also See: | Hotel Foreclosures and Bankruptcies to Rise; PKF-HR Expecting a 25% Increase in Full Service U.S. Hotels Lacking the Cash Flow to Pay their Debt Service in 2009 / January 2009 |

|

|